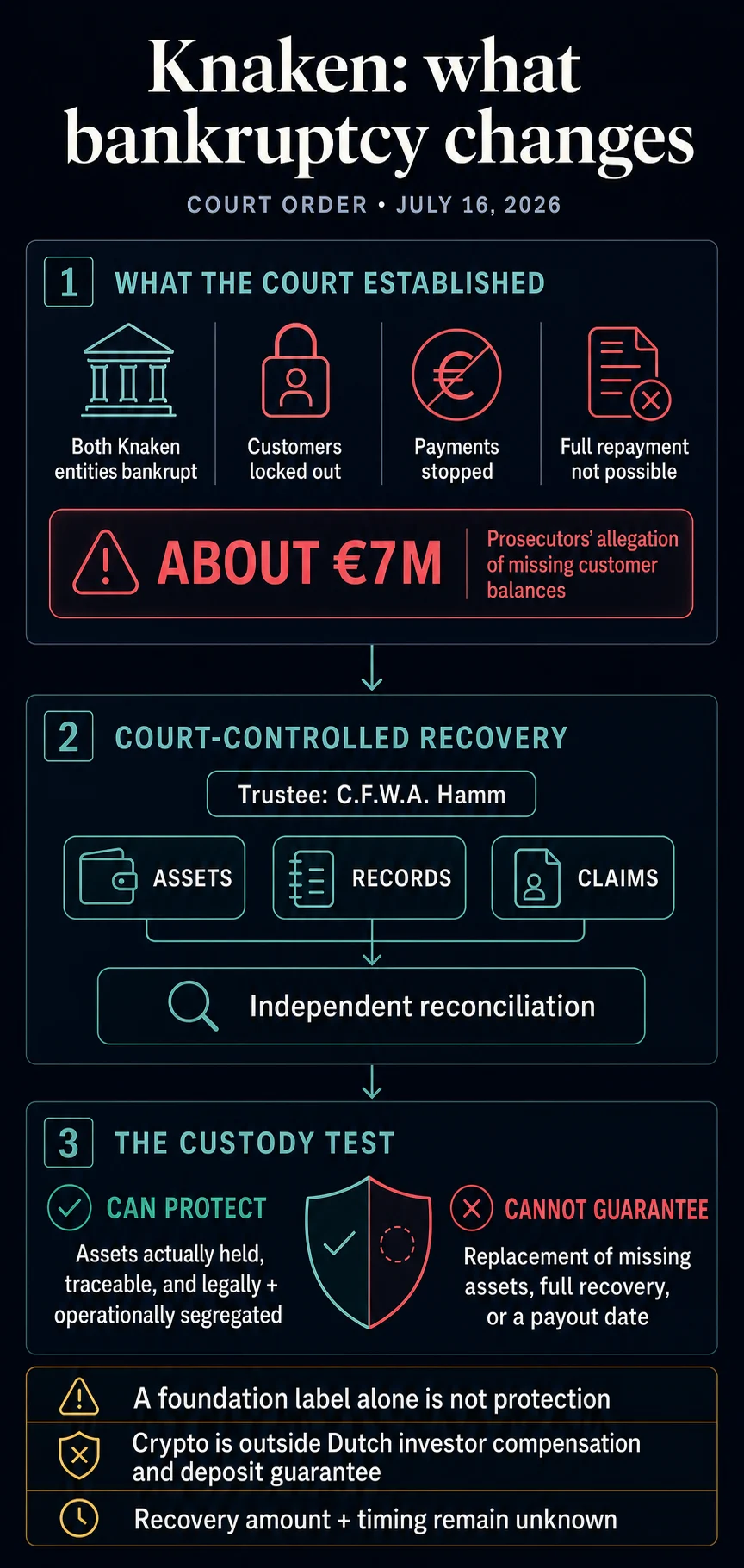

The Dutch cryptocurrency exchange Knaken, operating through its holding company Knaken Cryptohandel B.V. and the affiliated payments foundation Stichting Knaken Payments, has been placed under court-controlled bankruptcy as of July 16. The decisive ruling by the Rotterdam District Court followed findings that the exchange was demonstrably unable to fulfill its obligations to its customers, citing significant financial shortfalls and a lack of transparency regarding the extent of the deficit.

The court’s decision was precipitated by a petition from the Dutch Public Prosecution Service, which alerted the judiciary to a substantial monetary gap within customer balances. Official statements indicate that approximately €7 million is unaccounted for, leaving customers locked out of their accounts and unable to access their funds. This inability to process payments and the undisclosed "substantial coverage deficit" were key factors leading the court to override Knaken’s proposed alternative solutions and impose external oversight. Consequently, the management of Knaken has relinquished control over the wind-down process, with Trustee C.F.W.A. Hamm now holding the legal authority over both Knaken Cryptohandel B.V. and Stichting Knaken Payments.

From Internal Resolution to Court-Mandated Bankruptcy

Knaken had initially argued against bankruptcy, proposing an independent verification process followed by its own distribution protocol as a means to protect customer assets. The exchange’s defense hinged on the assertion that existing measures, including criminal asset seizures, the service shutdown, and its custody structure, were already sufficient safeguards. However, the Rotterdam District Court found these arguments insufficient, opting instead for a court-appointed trustee to manage the liquidation and asset recovery.

The intervention by the Dutch Public Prosecution Service marked an unusual pathway to bankruptcy proceedings. Prosecutors stepped in because customer accounts were blocked, and the lack of clear disclosure prevented individuals from assessing their financial standing or initiating meaningful bankruptcy petitions independently. The court-controlled process, therefore, provides customers with a mechanism for resolution that operates independently of Knaken’s internal accounting and proposed payout systems.

Under Dutch law, a court-appointed bankruptcy trustee operates as a fiduciary for the collective body of creditors, overseen by a supervising judge. The trustee’s mandate is extensive, encompassing the inventory of all assets and claims, thorough examination of financial records for irregularities, protection and liquidation of the bankrupt estate, and the subsequent proposal of distributions based on established claim priorities, as outlined in the Dutch judiciary’s guidance and the Bankruptcy Act.

For Knaken, this means the trustee is tasked with reconciling the exchange’s platform ledgers with its digital wallets, access controls, bank accounts, and any other property held by both the operating company and the payments foundation. A crucial aspect of this process will be to definitively establish which entity is liable to each customer and whether assets identified as customer property were indeed held separately from the exchange’s own operational estate. While this independent verification is vital, it does not inherently resolve the financial deficit or predetermine the recovery percentage for customers.

Investigation into Potential Criminal Conduct

In parallel with the civil bankruptcy proceedings, the Fiscal Intelligence and Investigation Service (FIOD) has been conducting an investigation into potential criminal conduct associated with Knaken. Searches were carried out on June 29, according to prosecutors, during which digital data carriers and company assets were seized. As of June 30, no arrests had been announced. It is important to note that these investigations and seizures do not constitute a finding of guilt, and the legal disposition of seized property, along with its coordination with the bankruptcy estates, will be determined through the ongoing legal processes. The distinct teams handling the civil petition and the criminal investigation highlight the multi-faceted nature of the case.

The Crucial Role of Custody in Customer Recovery

The bankruptcy of Stichting Knaken Payments places a significant emphasis on the exchange’s custody structure as a critical determinant of customer recovery. While the establishment of a separate foundation is typically intended to create legal separation between an operating company and client property, its effectiveness hinges on the actual presence of sufficient assets, accurate record-keeping, and the availability of these assets for repatriation when the platform fails.

The Dutch Authority for the Financial Markets (AFM) has previously stated that Dutch law lacks a statutory segregation regime for custodied crypto assets that is as robust as those governing securities held by banks and investment firms. Consequently, crypto providers in the Netherlands often utilize separate entities, such as foundations, to establish legal separation. However, for this separation to provide effective protection, the provider must demonstrably hold client crypto and funds, maintain meticulous position records, utilize distinct client and proprietary wallets, implement secure recovery-key controls, confine the foundation’s activities strictly to client custody interests, and possess a functional procedure for asset repatriation.

Crucially, neither the court nor the prosecution has publicly disclosed the specific Knaken assets that remain, their locations, whether the platform’s ledgers align with the foundation’s records, or if customer balances were legally and operationally segregated. With both entities now in bankruptcy, the trustee’s immediate priority is to ascertain these facts. Only then can an account entry be meaningfully linked to identifiable property or an accepted claim for recovery.

Adding to the complexities, prosecutors have indicated that Knaken had not secured the required authorization from the AFM. The Markets in Crypto-Assets Regulation (MiCA), which has recently come into effect, sets a new benchmark for the safeguards expected from authorized crypto custody providers.

MiCA’s Framework and Implications for Crypto Custody

MiCA Article 70 mandates that authorized providers holding client crypto or access means must safeguard client ownership rights, particularly in instances of insolvency. Subject to specific institutional exceptions, eligible client funds are generally required to be deposited in a separately identifiable account at a credit institution or central bank by the next business day.

Furthermore, MiCA Article 75 imposes obligations on custody providers to maintain per-client position records, establish a clear custody policy, and implement effective return procedures. Client holdings must be legally and operationally distinct from the provider’s own assets to ensure that properly custodied crypto remains beyond the reach of the provider’s creditors in the event of insolvency. The regulation’s official text emphasizes preventive custody controls rather than providing a mechanism to replace assets that are no longer present.

In anticipation of MiCA’s full implementation, the European Securities and Markets Authority (ESMA) had, in June, advised unauthorized providers to cease onboarding new clients, restrict existing activities to an orderly exit, safeguard client interests, and clearly communicate their asset handling strategies. This directive underscores the regulatory push for greater transparency and consumer protection within the crypto sector.

The operational risks associated with MiCA compliance have already manifested in other market exits. Recent reports indicated that AscendEX warned some withdrawals might not be processed following its own operational challenges. Knaken’s situation, however, is distinct and has progressed to a more advanced legal stage, with a court having officially recognized a coverage deficit and imposed bankruptcy control.

Investor Protection Landscape in the Netherlands

The Dutch regulatory framework offers limited recourse for crypto investors in such scenarios. De Nederlandsche Bank (DNB) clarifies that crypto-assets and crypto service providers fall outside the scope of the Dutch investor compensation scheme. Similarly, DNB’s deposit-guarantee guidance explicitly excludes crypto assets like Bitcoin. Any potential recovery of cash held at a bank would be contingent on the established ownership and structure of those accounts, which, in Knaken’s case, remain unclarified.

Navigating the Path Forward for Knaken Customers

For locked-out users of Knaken, the court-controlled bankruptcy signifies a shift from the exchange’s internal promises to an independent, legally supervised process. The initial critical development will be the trustee’s presentation of a reconciled inventory. This inventory must detail all controllable or recoverable assets, including crypto, cash, and other property, and cross-reference them with the entities’ records. While a displayed customer balance serves as evidence of the platform’s declared liabilities, actual recovery will depend on the ability to locate and legally link corresponding assets to customer claims.

It is possible that the foundation held certain assets for customers, while the operating company may owe other liabilities. The bankruptcy proceedings are tasked with determining whether identifiable client property exists outside the general creditor pool, whether shortfalls translate into claims against either of the bankrupt estates, and how these accepted claims will be ranked according to Dutch insolvency law.

The ongoing criminal investigation, while separate, could yield property or information crucial to the bankruptcy estate. However, the court announcement does not specify the nature or ownership of seized assets, nor does it predetermine their legal treatment. Effective coordination between the trustee and criminal authorities will be paramount in shaping the evidence and assets available for the bankruptcy process, without conflating the insolvency case with a judgment on criminal liability.

Only after these fundamental questions regarding asset availability, ownership, and legal standing are thoroughly addressed can the trustee provide a credible estimate of potential customer recovery and the timeline for distributions. The court’s intervention replaces Knaken’s self-proposed payout process with a structured accounting and collective claims procedure, offering a more transparent, albeit potentially protracted, route towards resolution for affected customers. The overarching implication is a stark reminder of the inherent risks in the digital asset space and the critical importance of robust regulatory oversight and transparent operational practices.