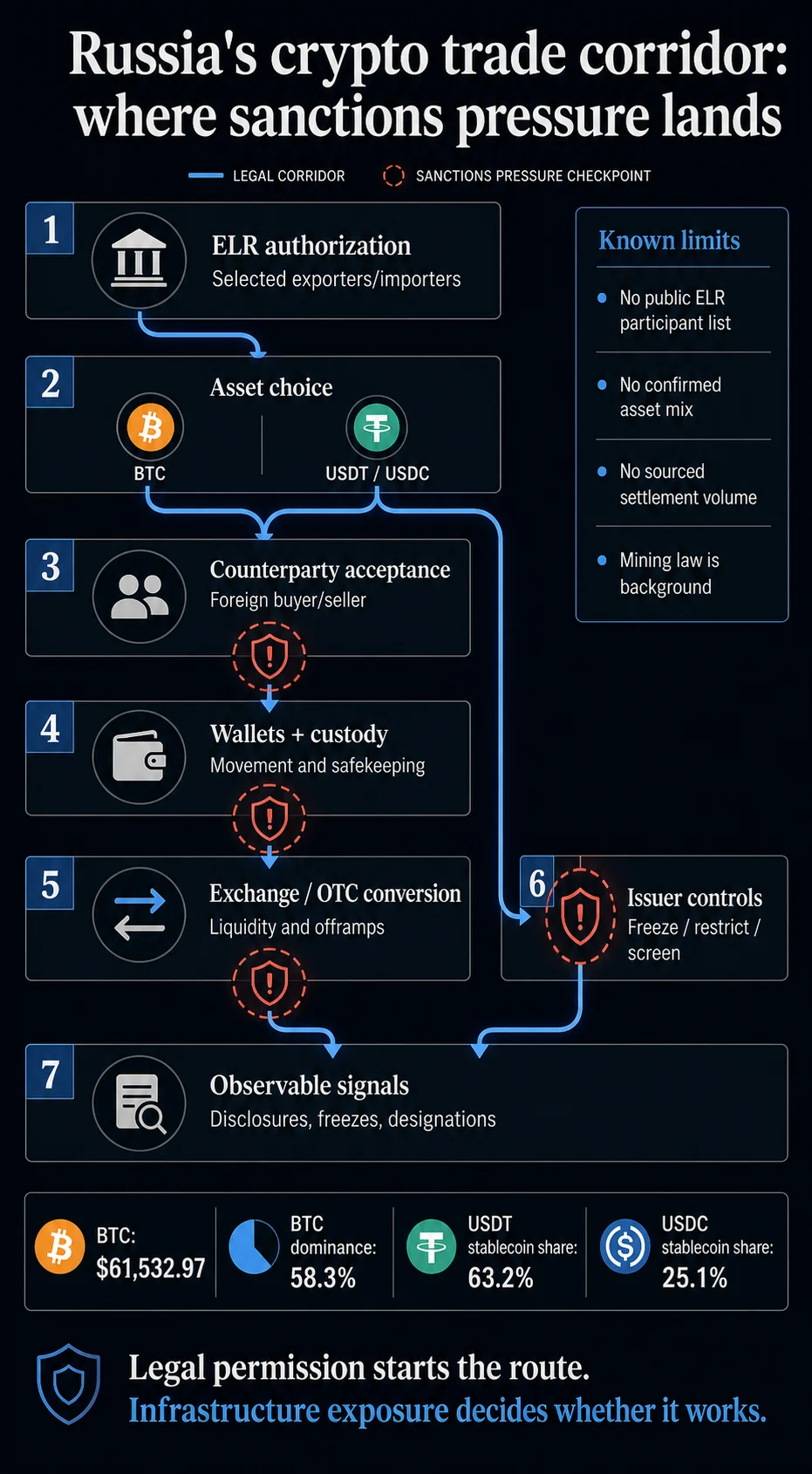

The Russian Federation has officially initiated a live-environment test of cryptocurrency-based foreign trade settlements, marking a significant escalation in the Kremlin’s efforts to circumvent the tightening net of international financial sanctions. This move, sanctioned by the Bank of Russia, allows a select group of exporters and importers to utilize digital assets for cross-border transactions under a highly regulated "Experimental Legal Regime" (ELR). By shifting digital currency usage from the shadows of unofficial workarounds into a state-supervised framework, Moscow is attempting to build a sovereign financial corridor that operates outside the traditional SWIFT-dependent banking system. However, the success of this initiative remains tethered to a complex web of global infrastructure—including exchanges, liquidity providers, and stablecoin issuers—that remains highly susceptible to Western regulatory pressure.

The Genesis of the Experimental Legal Regime

The transition toward legalized cryptocurrency settlements follows years of internal debate within the Russian government. For much of the last decade, the Bank of Russia maintained a hardline stance against digital currencies, citing risks to monetary stability and the potential for money laundering. However, the geopolitical shifts following February 2022 and the subsequent disconnection of major Russian financial institutions from the SWIFT global messaging system necessitated a radical rethink of national policy.

The current framework is anchored by two pivotal pieces of legislation. Federal Law No. 223-FZ provides the legal basis for digital currency payments under foreign-trade contracts, specifically within the boundaries of the ELR. Complementing this is Federal Law No. 221-FZ, which establishes a comprehensive framework for digital currency mining. Together, these laws aim to create a self-sustaining ecosystem where domestic mining provides the "liquidity" (digital assets) that can then be funneled through the ELR to pay for critical imports or receive proceeds from exports.

Under the ELR, the Bank of Russia acts as the ultimate gatekeeper. It determines which firms are permitted to participate, sets transaction limits, and monitors the flow of assets to ensure they do not destabilize the ruble. This controlled environment is designed to shield the broader Russian economy from the volatility of the crypto market while providing a "pressure valve" for industrial sectors struggling with traditional payment delays.

A Chronology of Financial Isolation and Innovation

The path to the ELR has been defined by a series of escalations in the financial war between Moscow and the West:

- February–March 2022: The United States, European Union, and their allies freeze roughly $300 billion in Russian central bank reserves and expel major Russian banks from SWIFT.

- Late 2022: The U.S. Treasury’s Office of Foreign Assets Control (OFAC) begins targeting Russian crypto-linked entities, most notably the exchange Garantex, which was accused of processing over $100 million in illicit funds.

- 2023: "Friendly" nations, including Turkey, China, and the UAE, begin facing "secondary sanctions" pressure from the U.S. Treasury. This leads to a significant increase in rejected payments and account closures for Russian businesses operating in these jurisdictions.

- August–September 2024: President Vladimir Putin signs the laws enabling the crypto pilot. The Bank of Russia begins selecting participants for the first wave of experimental settlements.

This timeline illustrates that the ELR is not a proactive choice of innovation but a reactive measure to the systemic failure of traditional banking corridors.

The Strategic Choice: Bitcoin vs. Stablecoins

One of the most critical aspects of the ELR is the choice of the settlement asset. The Russian framework must balance the need for decentralization with the requirement for price stability and accounting ease.

1. Bitcoin (BTC): The Issuer-Free Alternative

As of late 2024, Bitcoin maintains a market dominance of approximately 58.3%, with prices hovering near the $59,300 mark. From Moscow’s perspective, Bitcoin’s primary advantage is that it has no central issuer. Unlike a bank account or a stablecoin, no single entity can "freeze" a Bitcoin address at the protocol level. This makes it a formidable tool for resisting direct censorship. However, the inherent volatility of BTC makes it difficult for Russian firms to use for long-term invoicing. Furthermore, while the asset itself cannot be frozen, the "on-ramps" and "off-ramps"—the exchanges where BTC is converted into usable fiat currency—remain primary targets for Western enforcement.

2. Stablecoins: The Accounting Solution

Stablecoins, particularly USDT (Tether) and USDC (Circle), dominate the settlement discussion due to their 1:1 peg to the U.S. dollar. Together, they command nearly 90% of the stablecoin market. For a Russian importer, paying in USDT is functionally identical to paying in dollars, simplifying tax and accounting procedures. However, stablecoins are "centralized" assets. Circle, the issuer of USDC, explicitly states in its terms of service that it complies with U.S. sanctions and can freeze tokens in specific wallets. Tether has also shown an increasing willingness to cooperate with international law enforcement to block addresses associated with sanctioned entities. This creates a "chokepoint" where a Russian transaction could be neutralized mid-stream by a private company.

Mapping the External Chokepoints

The ELR creates domestic legality, but it cannot mandate international acceptance. A trade payment requires a willing counterparty and a functioning infrastructure. The following table highlights where the Russian "corridor" faces the most significant external risks:

| Settlement Phase | ELR Function | Sanctions Pressure Point |

|---|---|---|

| Authorization | Grants Russian firms legal right to use crypto. | Limited to domestic jurisdiction; no impact on foreign banks. |

| Liquidity Sourcing | Domestic miners or OTC desks provide assets. | Tracing of "tainted" coins by blockchain analytics firms. |

| Counterparty Acceptance | Foreign seller agrees to receive digital assets. | Fear of secondary sanctions and loss of access to Western markets. |

| Custody & Transfer | Movement of assets via digital wallets. | Wallet screening by major service providers and blacklisting of addresses. |

| Conversion (Off-ramp) | Converting crypto back into local fiat currency. | Centralized exchanges and banks refusing to process "Russian-origin" funds. |

Official Responses and Global Compliance Measures

Western regulators have not remained idle as Russia builds this alternative framework. The U.S. Treasury’s virtual-currency sanctions guidance has become the gold standard for global compliance. Digital asset firms—including those based in non-sanctioning jurisdictions—are increasingly adopting sophisticated blockchain analytics tools (such as Chainalysis or Elliptic) to identify and block transactions originating from Russian-linked wallets.

While the Russian government has not published a list of approved ELR participants to protect them from immediate designation, the Bank of Russia has signaled that the pilot will be "limited and cautious." Inferred reactions from the Russian business community suggest a mix of optimism and trepidation. Large industrial exporters see it as a necessary evil to keep trade flowing, while smaller firms fear that the high cost of compliance and the risk of having assets frozen by issuers like Circle or Tether may outweigh the benefits.

Broader Implications for Global Finance

The Russian crypto experiment is a "canary in the coal mine" for the future of the global financial system. If Moscow successfully facilitates large-scale trade via this corridor, it could provide a blueprint for other sanctioned nations, such as Iran or North Korea, to further decouple from the dollar-based order.

However, the experiment also reinforces the reality of "financial transparency" in the digital age. Unlike physical cash or gold, blockchain transactions leave a permanent, public trail. This "observable behavior" allows Western authorities to map out the networks of intermediaries—the brokers, OTC desks, and small-tier exchanges—that Russia is using.

The ultimate value of the ELR will be determined by whether the payment path survives contact with the global market. If the risk of secondary sanctions makes foreign counterparties unwilling to accept crypto from Russian entities, the corridor will remain a symbolic gesture rather than a practical tool. Conversely, if offshore liquidity pools remain accessible and "friendly" nations develop their own internal crypto-to-fiat clearinghouses, the ELR could mark the beginning of a truly bifurcated global financial system.

As the pilot progresses, the international community will be watching for operational signals: the frequency of wallet freezes, the emergence of new Russian-focused exchanges in "neutral" jurisdictions, and potential disclosures from the Bank of Russia regarding settlement volumes. For now, the corridor stands as a high-stakes test of whether decentralized technology can truly overcome the centralized power of global sanctions.