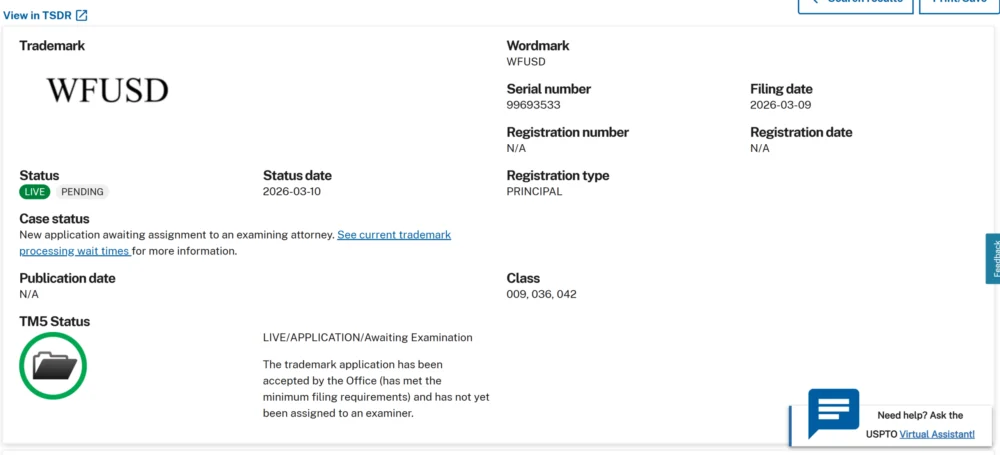

US banking giant Wells Fargo has formally submitted a comprehensive trademark application to the US Patent and Trademark Office (USPTO), indicating a significant strategic expansion into the burgeoning realm of cryptocurrency trading, digital payments, and advanced blockchain software services. The filing, dated Tuesday, seeks to secure the branding for "WFUSD," a designation that strongly suggests an intention to launch offerings closely tied to the US dollar and digital assets. This move positions one of America’s "Big Four" banks at the forefront of traditional financial institutions increasingly embracing the digital asset economy, moving beyond mere exploration to active infrastructure development.

The application, currently awaiting assignment to an examining attorney within the USPTO system, details an extensive array of potential products and services. These span the full spectrum of digital asset engagement, from direct financial services to underlying technological infrastructure. Specifically, the filing outlines "cryptocurrency trading services," "cryptocurrency exchange services," "cryptocurrency payment processing," "financial brokerage services for cryptocurrency trading," and "electronic transfer of virtual currencies." This broad scope highlights Wells Fargo’s intent to capture various segments of the digital asset market, catering to both institutional and potentially retail clients seeking exposure to cryptocurrencies.

Beyond direct transactional services, the trademark also encompasses sophisticated software tools integral to the functioning and expansion of blockchain ecosystems. The application explicitly lists "downloadable software for staking digital assets," which refers to the process of locking up cryptocurrencies to support a blockchain network and earn rewards. It also covers software for "accessing non-fungible tokens (NFTs)," a rapidly growing sector of digital collectibles and unique digital assets, "managing crypto wallets" for secure storage of digital currencies, and "executing digital asset trades." This commitment to providing foundational software solutions underscores a deep dive into the technological aspects of Web3, rather than just offering a superficial entry point.

Further elaborating on its ambitions, the filing includes references to a range of enterprise-grade blockchain and digital asset services. These include comprehensive "cryptocurrency payment processing" solutions, efficient "electronic transfers of virtual currencies," and "financial data feeds providing price information to blockchain-based smart contracts." The latter is particularly significant, as reliable real-time data is crucial for the functionality of decentralized finance (DeFi) applications and other smart contract-driven financial instruments.

Moreover, Wells Fargo’s trademark application details plans for "software-as-a-service (SaaS) platforms" designed for advanced blockchain functionalities. These platforms aim to facilitate "tokenizing assets," a process that converts real-world assets like real estate, art, or commodities into digital tokens on a blockchain, thereby increasing liquidity and fractional ownership possibilities. The application also mentions services for "verifying blockchain transactions," crucial for integrity and security, and "enabling cryptocurrency staking operations." Additional services like "authentication services" and "blockchain-based data transmission tools used in decentralized applications" further illustrate a strategic focus on building robust, secure, and integrated infrastructure for the next generation of financial services.

The Evolving Stance of Traditional Finance Towards Digital Assets

Wells Fargo’s latest move is not an isolated incident but rather a clear indicator of a broader, accelerating trend within traditional financial institutions (TradFi) to embrace digital assets. For years, major banks maintained a cautious, often skeptical, distance from cryptocurrencies, citing regulatory ambiguities, market volatility, and concerns over illicit finance. However, a confluence of factors has prompted a significant shift. The relentless growth of the cryptocurrency market, which has at times surpassed a multi-trillion-dollar valuation, coupled with increasing institutional adoption and clearer (albeit still evolving) regulatory frameworks in various jurisdictions, has made it increasingly untenable for major players to remain on the sidelines.

The growing demand from institutional clients, who are keen to diversify portfolios and explore new asset classes, has also been a powerful driver. Many traditional financial firms initially focused on custody solutions for digital assets, providing a secure way for institutions to hold cryptocurrencies without direct exposure to the complexities of self-custody. However, as confidence grew and regulatory clarity began to emerge, the focus expanded to include trading, brokerage, and more sophisticated blockchain-based services.

Wells Fargo’s Digital Asset Chronology

While Wells Fargo has been historically known for its conservative approach, its engagement with blockchain and digital assets has been progressively deepening. The bank was among the first major US financial institutions to explore internal applications of blockchain technology, notably for cross-border payments. In 2019, Wells Fargo revealed its own proprietary blockchain platform, Wells Fargo Digital Cash, designed to facilitate internal book transfers of tokenized US dollars across its global network. This initial foray, while not public-facing, demonstrated an early recognition of blockchain’s potential for improving efficiency in traditional banking operations.

The current "WFUSD" trademark filing represents a significant escalation of these efforts, moving from internal operational improvements to potential client-facing services. This evolution aligns with discussions reported in 2025, where Wells Fargo, alongside other banking giants like JPMorgan, Bank of America, and Citigroup, reportedly explored a joint stablecoin project. Such collaborative efforts underscore the industry’s recognition that a unified approach could accelerate adoption and standardization within the regulated financial ecosystem. The progression from internal experimentation and collaborative discussions to a formal, broad trademark application for public services signals a maturing strategy and a commitment to integrating digital assets into its core business model.

The Surge in Bank-Backed Stablecoins and Tokenization

The "WFUSD" nomenclature itself, strongly reminiscent of the US dollar, points towards the growing interest in stablecoins within the banking sector. Stablecoins, cryptocurrencies designed to maintain a stable value relative to a fiat currency or other asset, are increasingly seen as a bridge between traditional finance and the crypto world. They offer the efficiency and speed of blockchain transactions while mitigating the extreme volatility associated with unpegged cryptocurrencies like Bitcoin.

JPMorgan Chase has been a pioneer in this space with its JPM Coin, launched in 2020. Initially used for internal wholesale payments for corporate clients, JPM Coin facilitates instant, round-the-clock transfers of US dollars and euros between participating institutions. Its success has demonstrated the practical utility of bank-issued digital currencies in improving liquidity management and streamlining interbank settlements. This model has served as a blueprint for other financial institutions exploring similar ventures.

More recently, in a significant development earlier this year, Fidelity Digital Assets launched the Fidelity Digital Dollar (FIDD). This 1:1 US dollar-pegged, fully collateralized stablecoin operates on the Ethereum blockchain, showcasing how major asset managers are also venturing into the issuance of regulated digital currencies. These initiatives, including Wells Fargo’s potential "WFUSD," highlight a collective industry push towards creating a more efficient, programmable, and interconnected financial system built on blockchain technology. The increasing number of stablecoin trademark filings from banks globally, including a reported surge in South Korean bank stocks following similar stablecoin announcements, further corroborates this global trend.

The concept of "tokenizing assets," explicitly mentioned in Wells Fargo’s filing, is another critical area of focus for TradFi. Tokenization allows for the creation of digital representations of real-world assets on a blockchain, enabling fractional ownership, enhanced liquidity, and streamlined transferability. This could revolutionize markets for real estate, private equity, bonds, and even intellectual property, making illiquid assets more accessible to a broader range of investors and facilitating new forms of capital formation.

Implications for the Financial Landscape and Regulatory Environment

Wells Fargo’s aggressive move into digital assets carries profound implications for both the traditional financial sector and the cryptocurrency market. For traditional banks, it represents a crucial step towards modernizing their offerings and remaining competitive against agile fintech firms and native crypto platforms. By integrating crypto trading, payments, and blockchain infrastructure, Wells Fargo can potentially capture new revenue streams, reduce operational costs through blockchain’s efficiencies, and enhance its appeal to a tech-savvy client base.

The entry of a "Big Four" bank into this space also lends significant legitimacy to the digital asset market. It signals to institutional investors and mainstream consumers that cryptocurrencies and blockchain technology are maturing and becoming integral components of the future financial system. This could accelerate broader adoption and investment, further integrating crypto into the global economy.

However, this expansion also brings increased scrutiny from regulatory bodies. Regulators in the US, including the Office of the Comptroller of the Currency (OCC), the Federal Reserve, and the Securities and Exchange Commission (SEC), have been grappling with how to effectively regulate digital assets while fostering innovation. Wells Fargo’s comprehensive filing, encompassing a wide range of services from trading to staking and NFTs, will undoubtedly intensify regulatory discussions. This could potentially hasten the development of clearer guidelines and frameworks for banks operating in the crypto space, addressing critical areas such as consumer protection, anti-money laundering (AML), know-your-customer (KYC) compliance, and systemic risk management.

Potential Challenges and Opportunities

Despite the clear strategic intent, Wells Fargo, like other traditional financial institutions, will face several challenges in fully realizing its digital asset ambitions. Integrating legacy IT systems with nascent blockchain technology can be complex and costly. Cybersecurity remains a paramount concern, as digital assets are attractive targets for hackers. Moreover, the inherent volatility of many cryptocurrencies, coupled with the rapidly evolving regulatory landscape, presents ongoing operational and compliance risks.

Yet, the opportunities are substantial. By leveraging blockchain, Wells Fargo could significantly enhance the speed and cost-effectiveness of cross-border payments, reduce settlement times, and introduce innovative financial products. The ability to tokenize a vast array of assets could unlock trillions of dollars in new market value by creating more liquid and accessible markets. Furthermore, by offering secure, regulated access to digital assets, Wells Fargo could tap into a demographic of investors eager for institutional-grade crypto services.

While trademark filings do not guarantee the immediate launch of products, they serve as a vital indicator of a company’s strategic direction and commitment to securing intellectual property for future offerings. Wells Fargo’s "WFUSD" filing is more than just a legal formality; it is a powerful statement about the bank’s long-term vision for its role in a financial world increasingly shaped by digital innovation. As the lines between traditional finance and the digital asset economy continue to blur, such moves by established giants like Wells Fargo are poised to redefine the future of banking and investment.