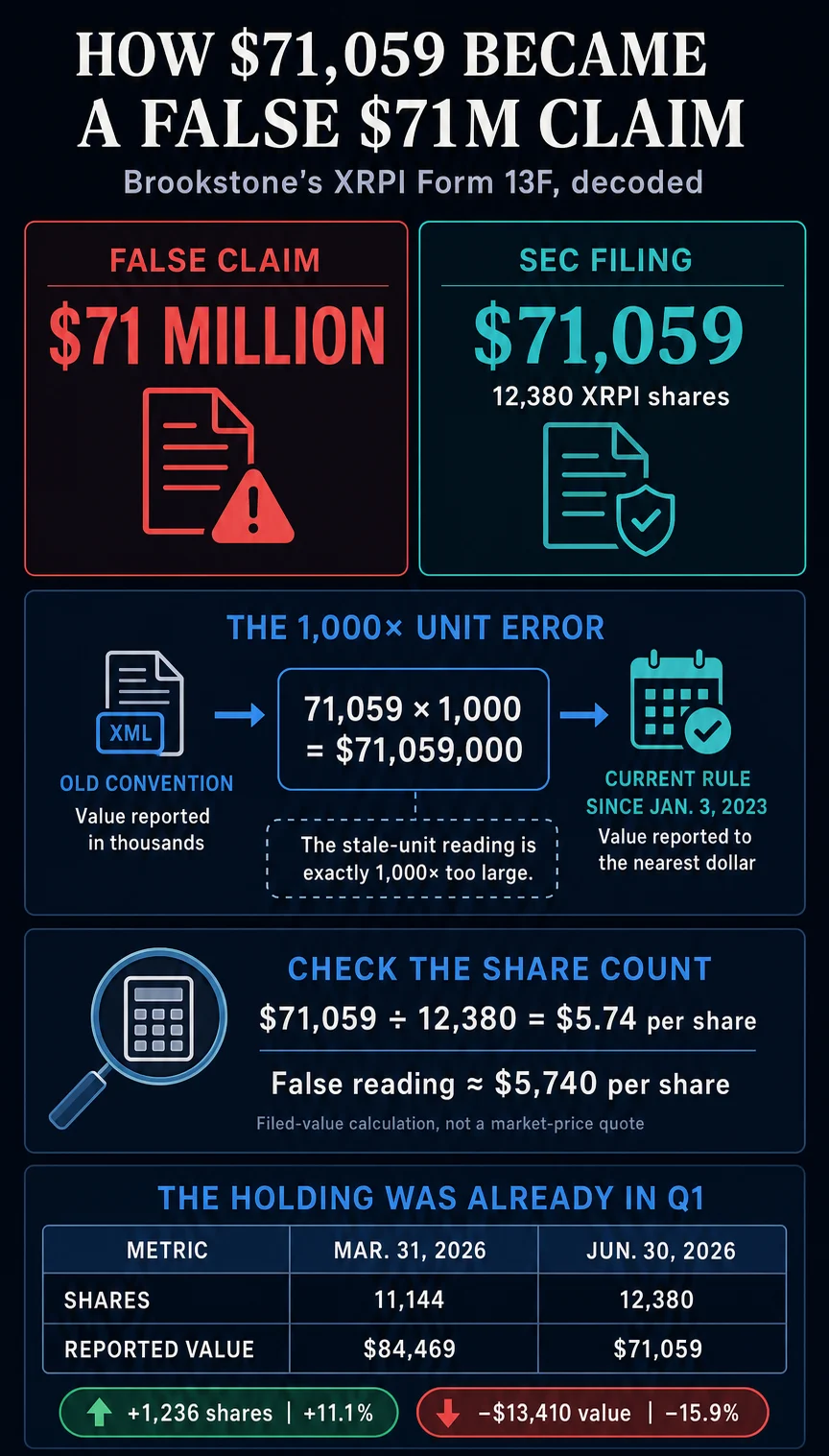

An analysis of recent U.S. Securities and Exchange Commission (SEC) filings has uncovered a significant discrepancy in reported holdings related to a Volatility Shares XRP ETF, leading to widespread social media speculation about a massive $71 million investment. The filings, however, indicate that the actual reported value is approximately $71,059, with the inflated figure stemming from a misunderstanding of an outdated SEC reporting convention. Investment manager Brookstone Capital Management disclosed its holdings as of June 30, 2026, detailing 12,380 shares of the Volatility Shares XRP ETF, identified by CUSIP 92864M780. While the filing clearly states a fair value of $71,059 for these shares, social media platforms quickly circulated claims of a $71 million position, a figure that is precisely 1,000 times the reported amount.

The genesis of this misinformation lies in a procedural change implemented by the SEC regarding how financial institutions report their holdings on Form 13F. Prior to January 3, 2023, the standard practice for these filings was to round dollar values to the nearest thousand dollars. However, the SEC amended this rule, mandating that all filings submitted on or after that date report dollar values rounded to the nearest whole dollar. This technical adjustment, detailed in EDGAR Release 22.4.1, means that the figure "71,059" in a post-2023 filing represents $71,059, not $71,059,000 as might have been interpreted under the previous system.

Decoding the Form 13F Filing: A Tale of Two Units

Brookstone Capital Management’s Form 13F filing for the quarter ending June 30, 2026, explicitly lists the Volatility Shares XRP ETF under CUSIP 92864M780. The disclosed quantity is 12,380 shares, with a reported fair value of $71,059. This figure, according to the SEC’s current reporting guidelines, is to be understood as the precise monetary value of the holding.

The misinterpretation arose when social media users, particularly on X (formerly Twitter), paired the share count with a rounded figure of "$71M." For instance, posts on X, such as one by user @Xaif_Crypto, juxtaposed the share count with this inflated monetary value. Shortly thereafter, other accounts, like @RippleXity, amplified the "$71 million" narrative. This viral spread of misinformation highlights a critical need for greater financial literacy and understanding of regulatory reporting standards within the rapidly evolving cryptocurrency landscape.

The discrepancy becomes starkly apparent when one considers the pre-2023 reporting convention. If the filing had adhered to the old rule, a value of "71,059" would indeed have represented $71,059,000. This outdated convention, which was in effect for many years, has led to a situation where a simple numerical value can be interpreted in drastically different ways depending on the reporting period. The SEC’s decision to shift to reporting to the nearest dollar was intended to provide greater precision and clarity in financial disclosures. However, in this instance, the legacy of the older system has inadvertently fueled a significant misunderstanding.

A Historical Perspective: The Evolution of SEC Reporting

The SEC’s Form 13F is a quarterly report filed by institutional investment managers with the SEC. It requires them to disclose their holdings of certain publicly traded securities as of the end of each calendar quarter. This form plays a crucial role in providing transparency into the portfolios of major financial players. The change in reporting units from thousands to the nearest dollar, effective January 3, 2023, was a significant procedural update.

The SEC’s guidance on Form 13F, available on its official website, clearly outlines these changes. The rationale behind the amendment was to enhance the granularity of reported data, allowing for more precise tracking of investment positions. The XML schema for the filing was updated to reflect this, with the value field now accommodating values rounded to the nearest dollar. This change aimed to eliminate the ambiguity that could arise from rounding to the nearest thousand, especially for smaller holdings or when precise valuations were critical.

Analyzing the Data: Share Count and Value Per Share

To further illustrate the discrepancy, a simple calculation can be performed: dividing the reported fair value by the number of shares. In Brookstone’s June 30 filing, $71,059 divided by 12,380 shares yields an approximate fair value of $5.74 per share. This per-share valuation is consistent with the current market price of many exchange-traded products, particularly those dealing with futures contracts.

Conversely, if one were to apply the obsolete thousands convention, the implied per-share price would be approximately $5,740 ($71,059,000 / 12,380 shares). Such a per-share valuation for an XRP-related ETF would be extraordinarily high and inconsistent with the known market dynamics of cryptocurrency-linked investment vehicles, especially given that XRP itself has not historically traded at such elevated individual token prices. This per-share calculation serves as a strong indicator that the $71 million figure is not supported by the actual filing data.

Chronology of Disclosures: A Consistent Presence

Brookstone Capital Management’s filings reveal that the Volatility Shares XRP ETF has been a consistent holding over at least two quarters. The firm’s Form 13F for the quarter ending March 31, 2026, reported 11,144 shares of the same CUSIP (92864M780), with a disclosed fair value of $84,469. This prior-quarter report was filed on April 16, 2026, indicating that the investment manager had already disclosed its stake in this security well before the latest filing.

The most recent filing, detailing holdings as of June 30, 2026, was submitted on July 15, 2026. This timeline is crucial: the filing reports the position as it stood at the close of business on June 30. There is no indication within this filing that any new purchases or significant portfolio adjustments were made on the filing date itself (July 15 or July 16). The comparison between the March 31 and June 30 disclosures shows an increase in the number of shares held (from 11,144 to 12,380, an 11.1% rise) but a decrease in the reported fair value (from $84,469 to $71,059, a 15.9% decline). This pattern suggests a dynamic market valuation of the ETF rather than a sudden, massive new investment.

Understanding the Underlying Asset: XRPI ETF

The security in question, identified by CUSIP 92864M780, is the Volatility Shares 1x XRP Futures ETF, commonly known as XRPI. According to Volatility Shares’ official product information, XRPI is designed to provide investors with exposure to XRP through futures contracts, not by directly holding XRP tokens. The fund’s strategy explicitly states that it does not invest in XRP itself. This distinction is critical, as it clarifies that Brookstone Capital Management’s reported holding is in an ETF that tracks the performance of XRP futures, rather than a direct investment in the cryptocurrency.

CryptoSlate previously reported on the launch of the XRPI ETF in May 2025, noting its position as one of the first 1x XRP futures ETFs available to U.S. investors. This background context is important for understanding the nature of the asset being held and reported. Brookstone’s 13F filing signifies that the investment manager exercised investment discretion over these XRPI shares. It does not imply direct ownership or custody of XRP tokens.

Broader Implications: Navigating Crypto Narratives

The incident surrounding the Brookstone Capital Management filing underscores a recurring challenge in the cryptocurrency space: the rapid proliferation of unverified information and the ease with which narratives can be amplified without thorough scrutiny. As institutional investors increasingly engage with digital assets through regulated financial products like ETFs, the accuracy of reporting and the public’s understanding of these disclosures become paramount.

This event offers a valuable case study for investors and analysts seeking to interpret institutional crypto disclosures. A four-step verification process can be highly effective:

- Verify the Filing Source: Always refer to the official SEC EDGAR database for the primary source document.

- Check the Filing Date and Reporting Rules: Confirm the filing date to understand which SEC reporting conventions (pre- or post-2023) apply to the dollar values.

- Calculate Per-Share Value: Divide the reported total value by the number of shares to determine a plausible per-share price. Compare this to known market prices for similar assets.

- Analyze Prior Filings: Examine previous quarterly filings to track changes in holdings over time and identify any consistent patterns or significant shifts.

In the case of Brookstone Capital Management, applying these steps reveals that the narrative of a $71 million XRP ETF holding is a misinterpretation rooted in an outdated reporting unit. The actual disclosed value of $71,059, while significantly smaller, represents a legitimate investment by the firm in a regulated XRP futures ETF. The consistent appearance of the security in prior filings further solidifies that this was not a new, massive acquisition, but rather a continuation of an existing investment strategy.

The implications of such misinterpretations extend beyond individual instances. They can lead to unwarranted market speculation, influence investor sentiment, and potentially distort the perceived level of institutional adoption of crypto-related assets. As the regulatory landscape for digital assets continues to mature, fostering accurate reporting and clear communication will be essential for building trust and ensuring informed decision-making within the global financial community. The distinction between a $71,059 investment and a $71 million one is not merely a matter of scale; it reflects a fundamental misunderstanding of the reporting mechanisms that govern institutional finance.