The decentralized finance (DeFi) sector, which serves as the cornerstone of the Ethereum ecosystem, is currently exhibiting technical indicators that suggest a significant shift in market dynamics. After a prolonged period of consolidation and declining on-chain activity following the market turbulence of 2022, a basket of "blue chip" DeFi tokens is showing signs of a robust recovery. These assets, which include Uniswap (UNI), Aave (AAVE), Maker (MKR), Curve (CRV), Synthetix (SNX), Compound (COMP), Balancer (BAL), and Sushiswap (SUSHI), are widely regarded as the foundational pillars of decentralized financial services. Their collective performance and network health metrics often serve as a leading indicator for the broader appetite for risk and innovation within the cryptocurrency industry.

Recent on-chain data provided by Glassnode reveals a pivotal trend reversal in the momentum of token transfers and user acquisition. For the first time in over a year, short-term activity metrics have eclipsed long-term averages, signaling an expansion phase that has historically preceded broader market rallies. This resurgence comes at a time when the digital asset industry is navigating a complex landscape of regulatory scrutiny, institutional interest in spot exchange-traded funds (ETFs), and a fundamental shift in how value is settled on the blockchain.

The Significance of Blue Chip DeFi Protocols

To understand the current growth trajectory, it is essential to define the role of these "blue chip" protocols. Unlike speculative assets that rely on hype, these tokens are tied to functional protocols with established track records, high Total Value Locked (TVL), and consistent revenue generation.

Uniswap remains the preeminent decentralized exchange (DEX), facilitating billions of dollars in monthly trading volume without the need for a centralized intermediary. Aave and Compound represent the primary lending markets, allowing users to earn interest or borrow against their holdings in a permissionless manner. MakerDAO, the issuer of the DAI stablecoin, has recently integrated real-world assets (RWAs) into its collateral base, bridging the gap between traditional finance and blockchain technology.

The performance of these tokens is more than just a reflection of price action; it is a measure of the utility and adoption of the Ethereum network. As the underlying infrastructure for these applications, Ethereum benefits from the increased transaction fees and network demand generated by these protocols. The current data suggests that the "utility phase" of the market is returning, with users moving beyond simple asset holding to active participation in decentralized credit and liquidity markets.

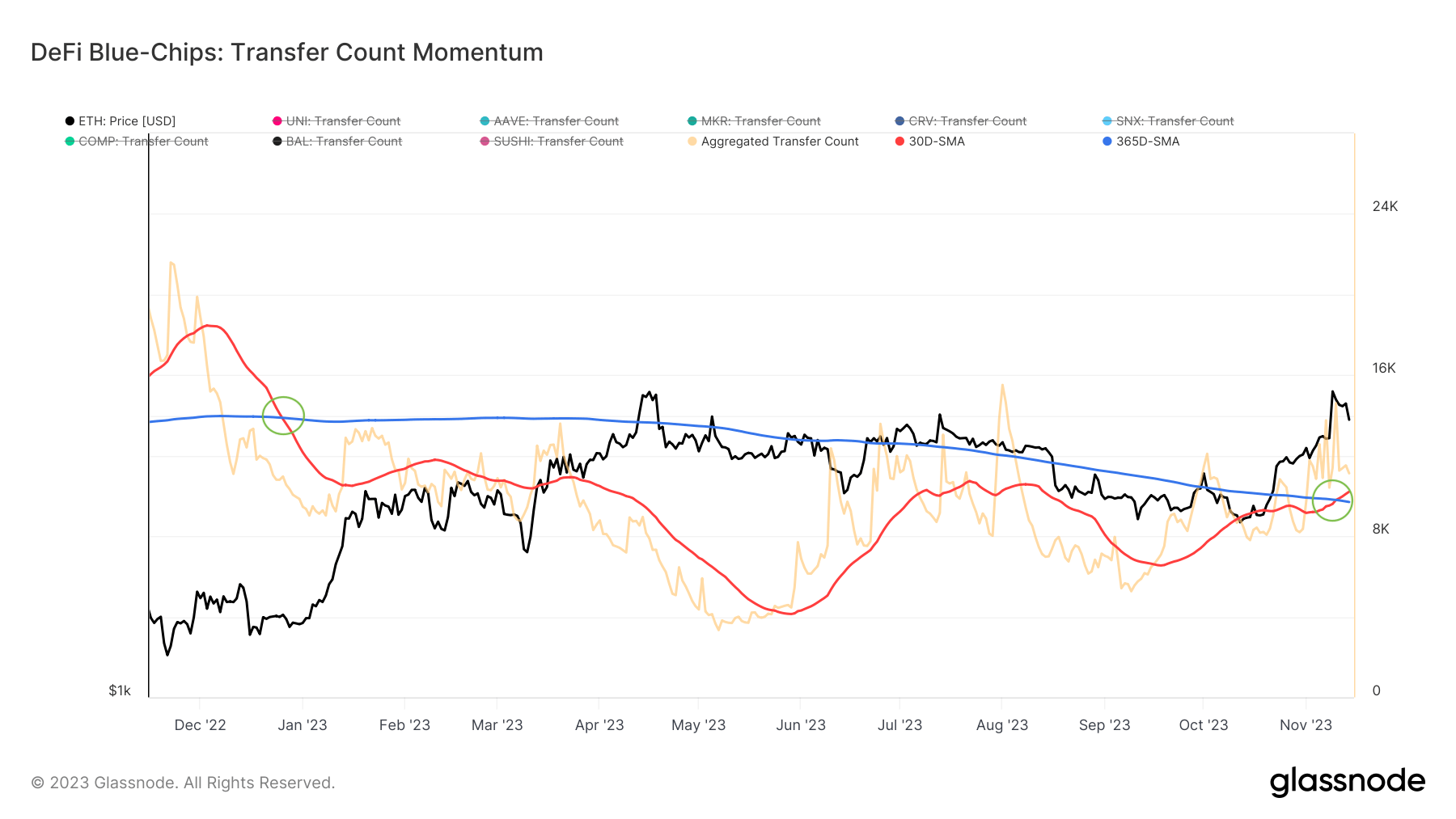

Analyzing Transfer Count Momentum: The 30D vs. 365D SMA

A primary metric used by analysts to gauge network health is the momentum of token transfers. This is calculated by comparing the 30-day Simple Moving Average (30D-SMA) of transactions against the 365-day Simple Moving Average (365D-SMA). This methodology effectively filters out daily volatility to reveal the underlying trend of user engagement.

When the 30D-SMA (representing short-term demand) crosses above the 365D-SMA (representing the long-term baseline), it indicates a "golden cross" of network activity. This phenomenon suggests that the demand for using and moving these tokens is accelerating faster than the yearly average, typically a precursor to price appreciation and ecosystem growth.

As of November 14, 2023, the 30D-SMA for Ethereum’s blue-chip DeFi tokens reached 12,208 transfers, significantly outpacing the 365D-SMA of 9,699. This gap represents a notable expansion in activity. Historically, such a crossover indicates that the "smart money" and active users are returning to the ecosystem, ending the period of contraction that began in late 2022. The fact that this metric has remained positive through the mid-November period suggests that the current momentum is not a momentary spike but a sustained increase in protocol utilization.

New Address Creation and User Adoption Trends

While transfer counts measure the activity of existing participants, the creation of new addresses is the definitive metric for network expansion. A growing number of unique addresses interacting with DeFi protocols suggests that the barrier to entry is lowering or that the value proposition of decentralized finance is attracting a fresh wave of capital.

The data regarding new address momentum for these blue-chip tokens is equally compelling. On November 14, the 30D-SMA of new addresses stood at 1,155, nearly converging with the 365D-SMA of 1,165. While the monthly average was slightly below the yearly average, the trajectory shows a sharp upward curve. This convergence marks a departure from the "dormant" phase of the market, where new user interest had flatlined.

This resurgence in user adoption is often attributed to several factors:

- Improved User Experience: The development of more intuitive wallets and layer-2 scaling solutions (like Arbitrum and Optimism) has made interacting with Ethereum-based DeFi protocols cheaper and faster.

- Yield Opportunities: As traditional interest rates stabilize, the "organic yield" provided by lending protocols like Aave and the staking rewards from Ethereum are becoming more attractive to yield-seeking investors.

- Institutional Validation: The entry of major financial institutions into the blockchain space has provided a "halo effect," encouraging retail and professional investors to explore established DeFi protocols.

A Chronology of the DeFi Market Cycles (2020–2023)

The current "poised for growth" status of DeFi tokens must be viewed through the lens of the sector’s historical volatility. The timeline of Ethereum’s DeFi ecosystem is marked by periods of explosive innovation followed by necessary corrections.

- The DeFi Summer (2020): This period saw the birth of yield farming and the meteoric rise of protocols like Compound and Uniswap. TVL across the board jumped from under $1 billion to over $15 billion in a few months.

- The Institutional Peak (2021): DeFi tokens reached all-time highs as the broader crypto market surged. Ethereum’s transition toward Proof of Stake became a central narrative, and DeFi protocols handled record volumes.

- The Great Contraction (2022): The collapse of the Terra/Luna ecosystem and the subsequent bankruptcy of FTX led to a massive deleveraging event. Blue-chip DeFi tokens lost over 80% of their value, and transfer counts plummeted as users fled to the safety of stablecoins or fiat.

- The Accumulation Phase (Early to Mid-2023): For most of 2023, DeFi tokens traded in a tight range. Activity was low, and the 30D-SMA of transfers remained consistently below the 365D-SMA, indicating a lack of conviction among market participants.

- The Recent Pivot (Q4 2023): The data from November 14 marks the definitive end of the contraction phase. The "flip" in transfer momentum signals that the market has likely bottomed and is now in a stage of re-accumulation and growth.

Expert Analysis and Market Implications

Market analysts suggest that the recovery of blue-chip DeFi tokens is a sign of a "flight to quality." In the wake of centralized exchange failures, there is a renewed appreciation for the transparency of on-chain protocols. Unlike centralized entities, protocols like MakerDAO or Uniswap operate via immutable code, where solvency can be verified by anyone in real-time.

"The convergence of new address creation and the surge in transfer counts tells us that the utility of these protocols is outlasting the speculative mania," notes one industry analyst. "When you see MakerDAO generating significant revenue from Treasury bills and Uniswap maintaining its lead over centralized competitors, it creates a fundamental floor for token value that didn’t exist in 2020."

Furthermore, the integration of Real World Assets (RWAs) is viewed as a major catalyst. MakerDAO’s move to back DAI with short-term U.S. Treasuries has allowed it to capture high interest rates from the traditional financial world and pass those benefits to on-chain users. This synergy between "old" and "new" finance is providing a level of sustainability to DeFi that was missing during previous cycles.

Potential Risks and the Path Ahead

Despite the positive indicators, the path to sustained growth is not without obstacles. Regulatory clarity remains a significant hurdle, particularly in the United States, where the SEC has scrutinized decentralized platforms and their governance tokens. The question of whether a governance token constitutes a security remains a point of contention that could impact the liquidity and listing of these assets on major exchanges.

Additionally, the rise of competing Layer-1 blockchains and the fragmentation of liquidity across various Layer-2 solutions present a challenge. While Ethereum remains the "gravity well" for DeFi liquidity, it must continue to scale to prevent high gas fees from driving users to alternative networks during periods of high activity.

However, the current data suggests that the "blue chips" have built a sufficient moat. The "network effect"—where liquidity begets more liquidity—remains strongest on Ethereum. As the 30D-SMA continues to trend above the yearly average, the primary focus for investors and developers alike will be the sustainability of this new user adoption.

Conclusion: A Pivot Toward Maturity

The data from November 2023 serves as a statistical confirmation of a shift in market sentiment. Ethereum’s blue-chip DeFi tokens are no longer just surviving the "crypto winter"; they are actively expanding their footprint. The "golden cross" in transfer momentum and the resurgence in new address creation indicate that the ecosystem is entering a more mature phase of its lifecycle.

As these protocols continue to innovate—through the implementation of V4 hooks on Uniswap, the expansion of GHO stablecoins on Aave, or the further integration of RWAs on Maker—the distinction between "crypto" and "finance" continues to blur. For the Ethereum ecosystem, the growth of these blue-chip tokens is not merely a price narrative; it is a testament to the resilience and enduring utility of decentralized financial infrastructure. If the current trends persist, the DeFi sector may well lead the next major cycle of blockchain adoption, driven by verified on-chain activity rather than speculative fervor.