The global banking landscape is on the cusp of a potentially transformative shift as the Basel III rules, which dictate crucial bank capital requirements, are slated for a significant update in 2026. A pivotal aspect of these revisions involves the risk rating assigned to digital assets like Bitcoin (BTC). Should Bitcoin receive a more favorable, lower risk rating within the revised framework, it could act as a catalyst, potentially triggering a "huge" influx of liquidity into the BTC market, according to the insightful analysis of market analyst Nic Puckrin. This anticipated regulatory evolution represents a critical juncture for both the burgeoning cryptocurrency ecosystem and traditional financial institutions, with far-reaching implications for capital allocation, service offerings, and the broader integration of digital assets.

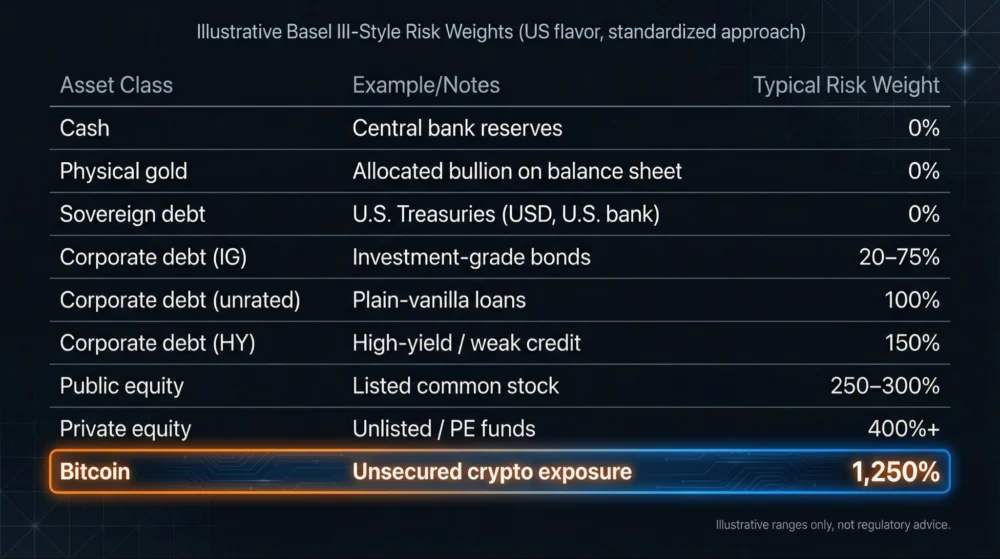

Under the prevailing Basel regulatory framework, Bitcoin and other similar unbacked digital assets are currently subjected to an extraordinarily high 1,250% risk weight. This stringent classification mandates that banks must hold reserve assets at a prohibitive 1:1 ratio to fully back any Bitcoin held on their balance sheets. Puckrin elaborated on this, explaining that such restrictive capital requirements render it "almost impossible" for banks to either hold BTC directly or to offer any Bitcoin-related services to their clientele without incurring substantial, often uneconomical, capital costs. The practical effect is a significant deterrent, effectively sidelining traditional banks from engaging meaningfully with the world’s largest cryptocurrency.

The potential for change has been amplified by recent developments in the United States. The Federal Reserve has recently unveiled a proposal outlining how these revised Basel rules will be implemented domestically, initiating a crucial 90-day public comment window. This period is vital, allowing industry stakeholders, advocacy groups, and the public to submit feedback that could influence the final regulatory posture. As Puckrin noted, "If BTC’s treatment improves even slightly, it could open the door for banks to finally integrate BTC into the financial system." This sentiment underscores the delicate balance regulators face between maintaining financial stability and fostering innovation.

Understanding the Basel Framework and Its Impact on Digital Assets

To fully grasp the significance of these impending changes, it is essential to delve into the genesis and purpose of the Basel Accords. The Basel Committee on Banking Supervision (BCBS) is an international committee that develops standards for banking regulation. Its recommendations, while not legally binding, are typically implemented by national legislatures and regulators worldwide, profoundly shaping global banking practices. The Basel III framework, specifically, emerged in the aftermath of the 2008 global financial crisis with the overarching goal of strengthening bank capital requirements, improving risk management, and enhancing the resilience of the global banking system.

The core of Basel III revolves around ensuring banks maintain sufficient capital buffers to absorb unexpected losses, thereby preventing taxpayer bailouts and safeguarding financial stability. This is achieved through a complex system of risk-weighted assets (RWAs), where different asset classes are assigned varying risk weights based on their perceived riskiness. The higher the risk weight, the more capital a bank must hold against that asset.

The BCBS first proposed specific capital requirements for cryptocurrencies in 2021, categorizing them into two main groups. Group 1 assets include tokenized traditional assets and stablecoins with effective stabilization mechanisms, which would be subject to capital requirements based on the risk of the underlying exposure. Group 2 assets, however, encompass unbacked cryptocurrencies like Bitcoin and other volatile digital assets, deemed to pose higher risks due to their price volatility, lack of historical data, operational risks, and potential for regulatory arbitrage. It was this proposal that placed Group 2 assets, including BTC, into the highest risk category with the aforementioned 1,250% risk weight. This effectively means that for every dollar’s worth of Bitcoin a bank holds, it must set aside an equal dollar amount of regulatory capital. This 1:1 capital backing requirement makes it economically prohibitive for banks to engage in significant crypto activities.

The Stark Disparity in Risk Weighting

The current capital requirements for Bitcoin stand in stark contrast to those for traditional financial assets, highlighting the perceived regulatory apprehension towards digital assets. As Jeff Walton, chief risk officer at Bitcoin treasury company Strive, has pointed out, while BTC and other Group 2 crypto assets carry a staggering 1,250% risk weight, investment-grade corporate bonds typically carry a risk weight of up to 75%. Even more telling is the fact that traditional safe-haven assets such as gold, government bonds, and physical cash are assigned a 0% risk weight, reflecting their perceived minimal credit risk. Walton succinctly articulated the industry’s perspective, stating that "risk is mispriced" under the current framework.

This disparity creates a significant barrier to entry for banks looking to participate in the burgeoning blockchain economy. For a bank, allocating precious capital to an asset with a 1,250% risk weight means that the potential returns from holding or servicing that asset must be astronomically high to justify the capital burden. In most cases, this simply isn’t feasible or aligns with their risk-adjusted return on capital (RAROC) metrics. Consequently, banks are largely excluded from a market that has grown to a multi-trillion-dollar valuation, despite growing client demand and the emergence of regulated investment products like spot Bitcoin ETFs in various jurisdictions.

Industry Calls for Reform and the "Chokepoint" Effect

The cryptocurrency industry, along with a growing number of traditional finance proponents, has been vocal in its demand for a re-evaluation of these punitive Basel rules. In February, several executives from crypto treasury companies publicly called for a reform of the Basel rules, advocating for the implementation of more accommodating risk weights for digital assets. Their arguments often center on the maturation of the Bitcoin market, its increasing institutional adoption, enhanced regulatory oversight in many jurisdictions, and its unique properties as a decentralized, immutable asset.

These industry leaders argue that the current rules stifle innovation and create an uneven playing field. They contend that as the market infrastructure for digital assets has matured, with robust custody solutions, regulated exchanges, and derivatives markets, the inherent risks associated with Bitcoin have become better understood and manageable. Furthermore, they highlight the long-term performance of Bitcoin, which, despite its volatility, has demonstrated remarkable resilience and growth over multi-year cycles, often outperforming traditional asset classes.

Chris Perkins, president of investment company CoinFund, offered a pointed critique of the Basel capital requirements, describing them as a "covert form of choking off the crypto industry." He drew a parallel, noting that these measures are more subtle than explicit efforts to "debank" crypto companies, akin to the infamous "Operation Chokepoint 2.0" tactics. Perkins elaborated, stating, "It’s a very nuanced way of suppressing activity by making it so expensive for the bank to do those activities." This "chokepoint" effect prevents traditional banks from offering competitive crypto services, pushing clients towards less regulated entities or entirely out of the regulated financial system for their digital asset needs. This, ironically, could introduce systemic risks that the Basel framework aims to mitigate.

The US Regulatory Implementation and Public Comment Window

The recent proposal by the Federal Reserve, in conjunction with the Federal Deposit Insurance Corporation (FDIC) and the Office of the Comptroller of the Currency (OCC), to implement the revised Basel III framework in the US is a critical development. This tripartite approach ensures a harmonized regulatory stance across the nation’s banking system. The 90-day public comment window is not merely a bureaucratic formality; it is a crucial mechanism through which stakeholders can directly influence the rulemaking process.

During this period, banks, financial industry associations, cryptocurrency firms, academic experts, and even individual investors can submit detailed arguments, data, and recommendations. These comments often highlight unintended consequences of proposed rules, present alternative approaches, or provide new information that regulators may not have fully considered. For instance, arguments against the 1,250% risk weight could emphasize the development of sophisticated risk management tools for digital assets, the emergence of regulated derivatives that allow for hedging, and the increasing understanding of Bitcoin’s distinct characteristics compared to other unbacked crypto assets. The outcome of this comment period could significantly shape how the US interprets and applies the BCBS recommendations, potentially leading to a more nuanced approach to Bitcoin’s risk classification.

Global Perspectives and Harmonization Challenges

While the Basel Committee provides a global standard, the actual implementation varies by jurisdiction. The European Union, for example, is also actively developing its own framework for digital assets, including specific capital requirements for banks. The UK, Japan, and other major financial centers are similarly engaged in adapting their regulatory regimes to accommodate or restrict crypto assets based on the Basel guidelines. The challenge lies in achieving a degree of global harmonization to prevent regulatory arbitrage, where financial institutions might gravitate towards jurisdictions with more lenient rules.

A fragmented regulatory landscape could complicate international banking operations and create inefficiencies. Therefore, any move by a major economy like the US to refine its approach to Bitcoin’s risk weighting under Basel III could influence other jurisdictions to reconsider their positions, potentially fostering a more globally consistent and accommodating environment for digital asset integration into mainstream finance.

Broader Implications of a Lower Risk Weight for Bitcoin

Should Bitcoin receive a lower risk rating, the ripple effects across the financial system and the crypto market would be profound and multifaceted:

-

Direct Bank Holdings: With reduced capital burdens, banks could begin to hold Bitcoin directly on their balance sheets. This might be for proprietary trading, hedging purposes, or even as a strategic reserve asset, mirroring their holdings of other commodities or currencies. This direct institutional demand could significantly absorb existing supply and drive price appreciation.

-

Expanded Banking Services: The primary impact would be the unleashing of a suite of Bitcoin-related services from traditional banks. This could include:

- Custody Solutions: Banks could offer secure, regulated custody for Bitcoin, providing a trusted alternative to existing crypto custodians.

- Lending and Borrowing: Facilitating BTC-backed loans or offering lending services to clients, leveraging their established credit infrastructure.

- Trading Desks: Setting up dedicated desks for institutional and high-net-worth clients to trade Bitcoin, bringing greater liquidity and depth to the market.

- Advisory Services: Providing expert guidance on digital asset investment strategies.

- Integration with Existing Products: Potentially integrating Bitcoin into wealth management portfolios, treasury management solutions, and even payment systems.

-

Enhanced Market Liquidity and Stability: The entry of traditional banks would dramatically increase institutional participation, leading to deeper order books and potentially reduced price volatility over time. With more regulated players, the market could become more robust and resilient to large price swings.

-

Bridging TradFi and Crypto: This regulatory shift would accelerate the integration of digital assets into the mainstream financial system, blurring the lines between traditional finance (TradFi) and decentralized finance (DeFi). It would legitimize Bitcoin further in the eyes of institutional investors and the broader public.

-

Competitive Dynamics: Banks would likely compete with existing crypto-native firms, potentially driving innovation and efficiency across the entire digital asset ecosystem. This competition could lead to better products, lower fees, and improved client experiences.

-

Economic Growth and Innovation: By removing significant regulatory hurdles, banks could become engines for innovation in the digital asset space, fostering new financial products and services that leverage blockchain technology beyond just Bitcoin.

Challenges and Regulatory Caution

Despite the compelling arguments for reform, regulators face legitimate concerns that underpin their cautious approach. The inherent volatility of Bitcoin, while potentially diminishing with market maturation, remains a significant factor compared to traditional assets. Regulators are also wary of operational risks, including cybersecurity threats, technological vulnerabilities, and the potential for market manipulation in still-nascent digital asset markets. Furthermore, anti-money laundering (AML) and combating the financing of terrorism (CFT) compliance remains a complex area for digital assets, requiring robust frameworks.

The debate also touches upon broader societal concerns, such as the environmental impact of Bitcoin mining, which has prompted calls for sustainable practices and disclosure from financial institutions engaging with crypto. These multifaceted challenges mean that any revision to Basel III’s treatment of Bitcoin will likely involve careful calibration, balancing the desire to foster innovation with the imperative to maintain financial stability and protect consumers.

Timeline and Future Outlook

The timeline leading up to the 2026 implementation date for the revised Basel III rules is crucial. The current 90-day public comment period in the US is a pivotal first step. Following this, regulators will analyze the feedback, potentially making adjustments to their proposals before issuing final rules. These final rules will then guide how banks in the US must capitalize their exposures to Bitcoin and other digital assets. Similar processes will unfold in other major jurisdictions, all working towards harmonizing with the overarching BCBS recommendations.

The future outlook presents several scenarios. A slight improvement in Bitcoin’s risk rating, moving from 1,250% to perhaps a still-high but less prohibitive 800% or 600%, could still open the door for limited bank participation. A more significant reduction, perhaps bringing it closer to the risk weights of certain equities or commodities, would truly unleash the "huge" liquidity influx anticipated by analysts. Conversely, if the risk weight remains unchanged or only marginally adjusted, banks will largely remain on the sidelines, perpetuating the current "chokepoint" and potentially ceding further ground to crypto-native firms.

Ultimately, the decisions made in the coming months and years regarding Basel III’s treatment of Bitcoin will be instrumental in shaping the trajectory of financial innovation and the eventual role of digital assets within the global banking system. The dialogue between regulators, financial institutions, and the crypto industry is set to intensify, with the stakes exceptionally high for the future of finance.