Despite the veneer of instantaneous transactions that define modern consumer banking, the underlying financial system remains a labyrinth of intricate processes, legacy infrastructure, and multi-party coordination challenges. While a tap of a card or a click to buy a stock appears seamless to the end-user, the backend mechanics involve a complex interplay of banks, clearinghouses, and custodians, each maintaining separate ledgers of the same events. This inherent fragmentation necessitates a constant, resource-intensive process known as reconciliation—a "comparing of notebooks" that is responsible for multi-day settlement times, persistent operational risks, and annual industry costs estimated in the billions. As the financial sector seeks to modernize beyond its current limitations, blockchain technology is emerging as a pivotal solution, offering a shared, tamper-resistant layer that promises to synchronize records, automate execution, and significantly reduce reconciliation across diverse financial ecosystems. This article delves into the evolving role of blockchain in banking, not as a replacement for existing infrastructure, but as an innovative execution and coordination layer designed to enhance efficiency, security, and transparency.

The Foundational Challenges of Traditional Banking Infrastructure

The current architecture of global finance, largely developed over decades, relies heavily on siloed systems and message-based communication. When Bank A sends money to Bank B, it’s typically a message indicating a transfer, prompting Bank B to update its own database. Discrepancies between these independent records necessitate manual intervention, leading to delays and errors. This archaic system, while robust in its own right, is inherently inefficient. For instance, a simple wire transfer can take days to settle due to the sequential nature of validations and the need for each intermediary to confirm and update its own books. This delay, often referred to as settlement risk, ties up capital and exposes parties to market fluctuations, costing financial institutions an estimated $10-15 billion annually in operational overhead and liquidity costs. Moreover, the reliance on batch processing for many back-office functions further exacerbates these inefficiencies, creating a bottleneck in an otherwise fast-paced digital economy.

The financial industry’s back-office operations, often unseen by consumers, are burdened by a vast array of tasks ranging from transaction matching and exception handling to compliance checks and corporate actions processing. These tasks are frequently manual, prone to human error, and require extensive human resources, contributing significantly to operational expenditures. The sheer volume and complexity of these processes across global markets underscore the urgent need for a more streamlined, automated, and secure approach.

Blockchain: A Paradigm Shift Towards Shared Truth

At its core, a blockchain is a distributed digital ledger that records transactions in a tamper-resistant, verifiable manner. Instead of disparate institutions each maintaining their own private ledgers, a blockchain-based workflow allows all participating institutions to reference a single, shared ledger state. This fundamental shift from independent record-keeping to a common, synchronized truth delivers four foundational benefits that directly address long-standing infrastructure constraints in banking:

- Immutability and Verifiability: Once a transaction is recorded on a blockchain, it cannot be altered, providing an indisputable audit trail.

- Transparency and Auditability: Participants can view the shared ledger (with appropriate privacy controls), increasing trust and simplifying regulatory oversight.

- Automation via Smart Contracts: Programmable agreements, or smart contracts, can automatically execute predefined actions when certain conditions are met, eliminating manual steps.

- Decentralization and Resilience: The distributed nature of the ledger removes single points of failure, enhancing system resilience.

The widespread adoption of customer-facing digital platforms has created a stark contrast with the underlying banking stack, which often still relies on antiquated batch processing and manual reconciliation. A shared, programmable state layer, facilitated by blockchain, promises to reduce operational friction, accelerate settlement, and introduce unprecedented levels of automation without necessitating the wholesale replacement of existing systems. This incremental, standards-based approach allows banks to achieve measurable efficiency gains while preserving regulatory compliance and operational continuity, making the transition both practical and strategic.

Tangible Benefits of Blockchain for the Banking Sector

The potential benefits of integrating blockchain technology into banking operations are extensive and impactful, addressing critical areas of inefficiency and risk.

-

Faster Transactions and Settlement: In traditional markets, the settlement of a trade can take several days (T+2 or T+1 in many markets), tying up significant capital and increasing counterparty exposure. Blockchain-based settlement, particularly when combined with coordinated Delivery-versus-Payment (DvP) and Payment-versus-Payment (PvP) workflows, can drastically shorten this cycle, potentially achieving near-instantaneous (T+0) atomic settlement. This simultaneous exchange of assets and payment materially reduces settlement risk, frees up liquidity, and significantly lowers the operational burden associated with multi-day post-trade processes. Estimates suggest that moving to T+0 settlement could unlock trillions in trapped capital globally.

-

Greater Security and Operational Resilience: Blockchain systems leverage advanced cryptography and consensus validation mechanisms to protect transaction integrity across multi-party networks. This inherent design strengthens resilience in workflows where data consistency is paramount, reducing reliance on centralized reconciliation points and manual controls that are susceptible to delays, errors, and single points of failure. The distributed nature of the ledger also makes it significantly more resistant to cyberattacks and data breaches compared to centralized databases.

-

Cost Reduction Through Automation: Smart contracts are a game-changer for automating financial processes. They enable rules-based execution across critical banking functions such as reconciliation, exception handling, corporate actions, and compliance checks—areas that traditionally demand substantial manual intervention. By embedding "if-this-then-that" logic directly into execution workflows, banks can dramatically improve straight-through processing (STP) rates, reduce manual effort, and consequently lower administrative costs. Industry analysts project that blockchain adoption could reduce infrastructure costs for banks by $15-20 billion annually by 2030, primarily through automation and reduced reconciliation.

-

Improved Transparency, Trust, and Compliance: A transparent, immutable ledger provides a single, verifiable view of transactions and asset states across all authorized participants. When combined with privacy-preserving identity and compliance controls, blockchains can significantly enhance auditability and streamline regulatory reporting without exposing sensitive data. This fosters greater trust among institutions, regulators, and clients, creating a more robust and accountable financial ecosystem. Regulators, such as the Monetary Authority of Singapore, have actively explored blockchain’s potential to improve oversight without compromising privacy.

Key Blockchain Use Cases Revolutionizing Banking Operations

The theoretical benefits of blockchain are translating into practical applications across various facets of banking:

-

Payments and Money Transfers: Cross-border payments are notoriously inefficient, characterized by fragmented messaging systems, multiple intermediaries, and delayed finality, all contributing to high costs and reconciliation overhead. Blockchain-enabled workflows aim to dramatically improve coordination and settlement efficiency. The maturation of stablecoins, tokenized deposits, and Central Bank Digital Currencies (CBDCs) alongside traditional payment rails presents a compelling future. Institutions are actively exploring how existing messaging standards, such as ISO 20022, can be integrated with blockchain environments to support programmable payments, reducing operational friction and improving transparency. The World Bank estimates that remittance fees alone cost consumers billions annually, a figure blockchain could significantly reduce.

-

Clearing and Settlement: This area represents one of the most operationally complex segments of finance, demanding precise data synchronization across custodians, clearinghouses, broker-dealers, and asset servicers. The current system relies heavily on message-based confirmation and extensive post-trade reconciliation across siloed systems. Blockchain can serve as a common coordination layer for post-trade activity, drastically reducing reconciliation overhead and providing consistent access to verified records. As assets become increasingly tokenized, standardized reference data and coordinated workflows across both traditional and blockchain environments become critical to achieving faster, lower-risk settlement.

-

Trade Finance: Trade finance remains a document-heavy and coordination-intensive domain involving a multitude of parties, including banks, logistics providers, insurers, and customs authorities. Disconnected systems and manual documentation introduce significant delays, disputes, and elevated fraud risk throughout the trade lifecycle. Blockchain-based workflows can synchronize key trade events—such as shipment status, document issuance, and ownership transfers—across all participants in near real-time. By maintaining a shared, tamper-resistant record, institutions can reduce paperwork by up to 80%, accelerate settlement, and enhance trust while preserving existing operational roles and responsibilities.

-

Identity Verification and Compliance: Identity and compliance (e.g., KYC – Know Your Customer, AML – Anti-Money Laundering) are fundamental to banking but are often costly and repetitive due to duplicated verification processes across institutions. Customers frequently resubmit sensitive documentation, while banks independently perform similar checks on the same information. Blockchain-based identity solutions, particularly those leveraging verifiable credentials, enable individuals and institutions to prove specific attributes (e.g., KYC status, eligibility) without repeatedly sharing underlying personal data. This approach reduces duplication in compliance workflows, supports jurisdiction-specific regulatory requirements, and strengthens privacy protections, potentially saving institutions billions in compliance costs.

Real-World Examples of Blockchain Adoption in Banking

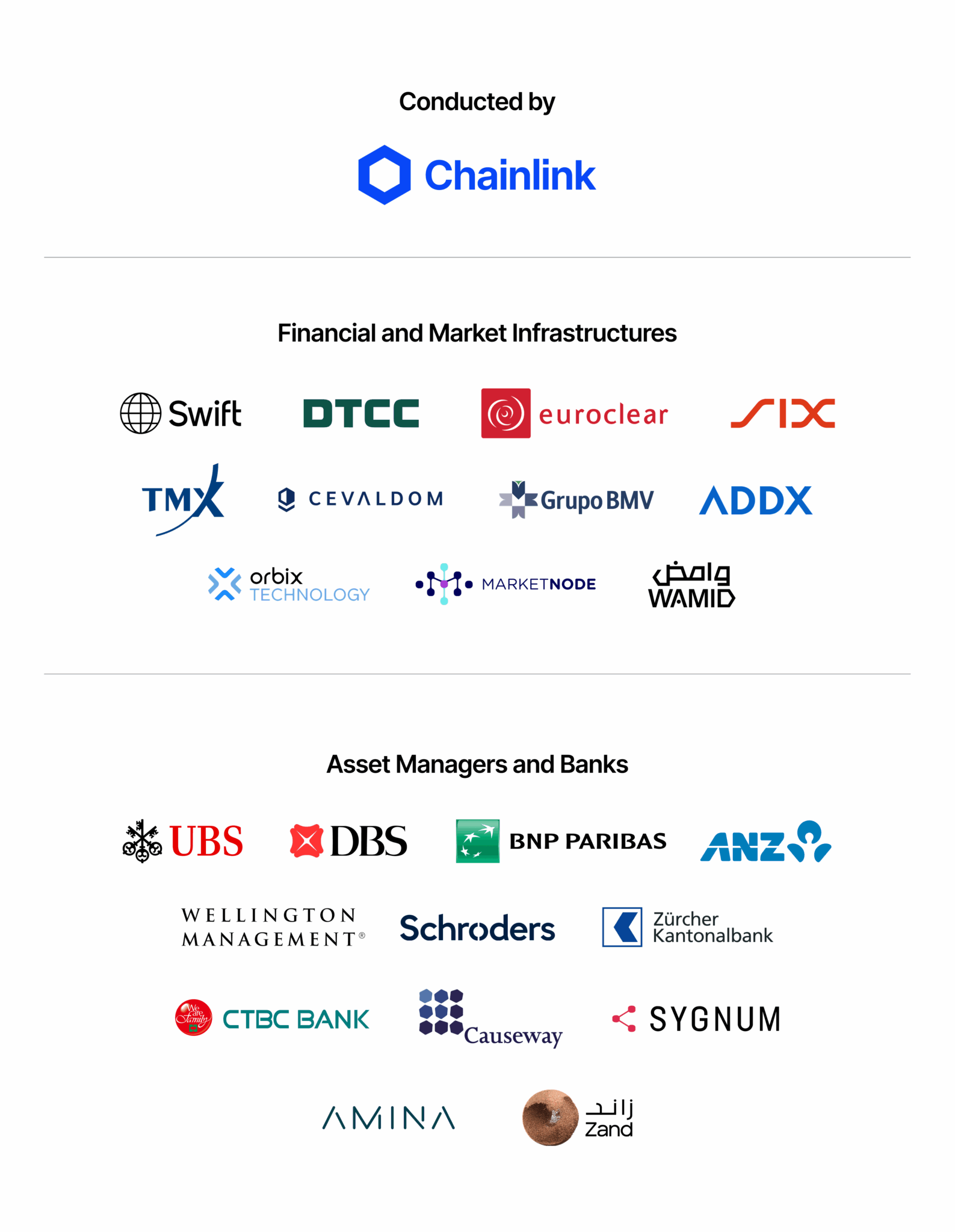

The transition from theoretical potential to practical application is well underway, with major banks and market infrastructures actively integrating blockchain platforms with their existing systems and regulatory frameworks. These initiatives underscore a pragmatic adoption strategy, demonstrating how blockchain can deliver value while upholding the infrastructure and controls that institutions rely on. Chainlink, a decentralized oracle network, has emerged as a critical enabler in many of these pioneering efforts, providing essential data, interoperability, compliance, and privacy solutions.

-

Swift Connectivity and Cross-Chain Settlement: A landmark collaboration between Chainlink and Swift has enabled financial institutions to connect to multiple public and private blockchain networks using existing Swift infrastructure and messaging standards. Leveraging the Chainlink Cross-Chain Interoperability Protocol (CCIP), these initiatives demonstrate how tokenized asset settlement workflows can be coordinated alongside traditional payment rails, crucially without requiring banks to replace core messaging systems. Under the Monetary Authority of Singapore’s Project Guardian, Swift, UBS Asset Management, and Chainlink successfully demonstrated the issuance and settlement of tokenized assets using existing fiat payment infrastructure, charting a practical, standards-based path to institutional adoption. This project, completed in late 2023, was hailed as a significant step towards unlocking new liquidity pools.

-

Standardizing Corporate Actions Across Global Markets: Corporate actions processing—events like mergers, dividends, and stock splits—is notoriously complex, fragmented, and prone to errors, costing the industry billions annually. Chainlink has powered a global industry initiative involving 24 financial institutions and market infrastructures, including Swift, DTCC, Euroclear, UBS, DBS Bank, ANZ, BNP Paribas, Wellington Management, and Schroders, to address this challenge. By combining oracle networks and blockchains with structured data extraction and validation, this work transforms fragmented, manual corporate actions workflows into standardized, near-real-time processes. The result is a projected reduction in operational cost, lower error rates, and significantly less reconciliation overhead across jurisdictions, improving market efficiency and reducing risks for investors.

-

Tokenized Fund and Digital Asset Settlement: Chainlink has been instrumental in multiple major institutional initiatives involving tokenized assets and stablecoins. Collaborations with Kinexys by J.P. Morgan, Ondo Finance, and other market participants have demonstrated atomic Delivery-versus-Payment (DvP) settlement workflows. These solutions coordinate asset and payment legs to reduce settlement risk and operational complexity, showcasing how tokenized assets can settle with greater certainty and efficiency when execution and coordination occur within a shared, programmable environment. These projects, often initiated in 2022-2023, have moved beyond proof-of-concept to pilot-scale implementations.

-

Cross-Border Compliance and Identity Workflows: In Asia, Chainlink has enabled compliant cross-chain settlement under initiatives such as the Hong Kong Monetary Authority’s e-HKD+ program. Institutions including ANZ Bank, China AMC, and Fidelity International utilized Chainlink infrastructure to verify investor eligibility, enforce jurisdiction-specific controls, and execute tokenized asset transactions across borders. These workflows demonstrate the capability of blockchain-based settlement to meet stringent regulatory requirements while preserving privacy and supporting complex cross-jurisdictional operations, paving the way for more efficient global capital flows.

-

Integration With Institutional Messaging and Transfer Agency Systems: The Chainlink Runtime Environment (CRE) facilitates the initiation of on-chain fund workflows directly from existing enterprise infrastructure, including ISO 20022 messages transmitted via Swift. In collaboration with UBS Tokenize, Chainlink demonstrated how subscription and redemption requests for tokenized funds could be orchestrated on-chain through standardized transfer agency workflows without replacing core banking systems or operational processes. This project, showcasing a direct bridge between legacy systems and blockchain, highlights the practical approach to incremental modernization.

Challenges and Considerations for Widespread Adoption

Despite the undeniable progress, the full-scale adoption of blockchain in banking faces several significant challenges:

- Regulatory Uncertainty: The evolving nature of blockchain technology often outpaces regulatory frameworks. Clear guidelines are needed regarding digital asset classification, custody, data privacy (e.g., GDPR compliance), and anti-money laundering (AML) protocols. Regulators are actively engaging, but a globally harmonized approach is still nascent.

- Interoperability: The proliferation of different blockchain networks (public, private, permissioned) necessitates robust interoperability solutions to ensure seamless communication and asset transfer across disparate chains and with legacy systems. Without this, new data silos could emerge.

- Scalability: Enterprise-grade blockchain solutions must demonstrate the capacity to handle the immense transaction volumes of global financial markets, which can reach hundreds of thousands or millions of transactions per second during peak times.

- Data Privacy: While blockchains offer transparency, financial transactions often require strict confidentiality. Solutions like zero-knowledge proofs and privacy-preserving computation are crucial to balance transparency with data privacy requirements.

- Integration with Legacy Systems: Banks operate complex, deeply entrenched legacy systems. Integrating new blockchain layers without disrupting existing operations or incurring prohibitive costs is a major technical and logistical hurdle.

- Talent Gap: A shortage of skilled professionals with expertise in both traditional finance and blockchain technology can impede development and deployment efforts.

These realities explain why most institutional initiatives prudently focus on standards-based integration, incremental deployment, and controlled automation, rather than radical overhauls.

Chainlink’s Pivotal Role in Accelerating Blockchain Adoption

Modern banking’s embrace of blockchain extends beyond mere token issuance; it demands trusted data, secure cross-network coordination, and seamless integration with existing institutional workflows. The Chainlink platform is uniquely positioned to operationalize blockchain-based processes in production environments by enabling:

- Secure Interoperability: Through CCIP, Chainlink provides a secure, reliable, and auditable standard for cross-chain communication and asset transfers, connecting disparate blockchain networks and bridging them with traditional financial systems.

- Real-World Data Integration: Chainlink’s decentralized oracle networks deliver tamper-proof real-world data (e.g., market prices, FX rates, corporate actions data) to smart contracts, ensuring the accuracy and reliability of automated financial processes.

- Advanced Computation: Chainlink offers verifiable off-chain computation services, allowing complex calculations to be performed privately and efficiently, which is crucial for compliance checks and sophisticated financial models without burdening the blockchain.

- Enterprise-Grade Standards and APIs: Chainlink provides standardized APIs and tools that allow banks to connect their existing enterprise infrastructure (e.g., Swift messages, core banking systems) directly to blockchain environments, facilitating a smooth transition.

This comprehensive approach empowers banks to modernize and integrate blockchain workflows that add tangible value, all while maintaining the reliability, security, and stringent controls required by global capital markets. By enabling standards-based connectivity between legacy systems and blockchain environments, Chainlink is not just facilitating innovation but is actively shaping the future where traditional finance (TradFi) and decentralized finance (DeFi) converge to create a more efficient, secure, and inclusive global financial system. The ongoing collaborations with industry giants signify a broader industry consensus that blockchain, supported by robust middleware like Chainlink, is no longer a distant future but a present imperative for competitive advantage and operational excellence in banking.