Stablecoins, digital assets designed to maintain a stable value relative to a reference asset like the U.S. dollar, are poised to significantly benefit from the burgeoning landscape of AI-driven payments over time, despite current limitations in early adoption. This forward-looking assessment comes from a recent report by Bernstein, a prominent global research and brokerage firm, shared in a Monday note with Cointelegraph. The report underscores the transformative potential of stablecoins in facilitating machine-to-machine (M2M) transactions and programmable, conditional payments between autonomous software agents, a domain where human intervention is increasingly minimized or eliminated.

The core argument from Bernstein posits that stablecoins possess inherent characteristics that make them ideal for the nascent machine economy. Their ability to enable microtransactions efficiently and their programmability are critical for unlocking a future where AI agents can autonomously exchange value. However, the report also offers a sober evaluation of the current state, noting that traction in this specific niche remains limited. This dual perspective – immense long-term potential coupled with nascent current usage – frames the evolving narrative around stablecoins and artificial intelligence.

The Promise of Autonomous Payments: Fueling the Machine Economy

The concept of machine-to-machine (M2M) payments is not entirely new, but the advent of sophisticated AI agents has injected a new urgency and complexity into the field. These autonomous entities, ranging from smart devices in the Internet of Things (IoT) to complex software algorithms managing data flows, require mechanisms to pay for services, data, or access to resources without human oversight. Traditional payment systems, often burdened by high transaction fees, slow settlement times, and a lack of inherent programmability, are ill-suited for the high volume, low-value, and automated nature of these interactions.

Stablecoins emerge as a compelling solution due to several key attributes:

- Efficiency for Microtransactions: The blockchain infrastructure underpinning stablecoins often allows for significantly lower transaction costs compared to traditional banking rails, making economically viable payments of fractions of a cent or a few cents possible. This is crucial for scenarios where an AI agent might pay for each API call, data packet, or computational task.

- Programmability: Smart contracts, integral to many stablecoin platforms, enable conditional payments. This means payments can be automatically executed only when specific predefined conditions are met, ensuring trust and automation in transactions between machines. For example, an AI agent could be programmed to pay for a data feed only after verifying its integrity and delivery.

- Near-Instant Settlement: Unlike traditional banking transfers that can take days to settle, stablecoin transactions on many blockchains settle in seconds or minutes, facilitating real-time economic interactions between machines.

- Global Accessibility: Stablecoins operate on open, permissionless blockchains, allowing for seamless cross-border transactions without the complexities and costs associated with traditional international wire transfers.

This vision paints a future where AI agents, whether performing tasks like data analysis, logistics coordination, or even content creation, can autonomously manage their finances, pay for necessary inputs, and receive payment for outputs, creating an entirely new layer of the digital economy.

Recent Developments and Early Traction in AI Payment Protocols

The interest in autonomous payment solutions is not merely theoretical; several prominent players in both traditional finance and the crypto space have recently launched initiatives to explore this frontier.

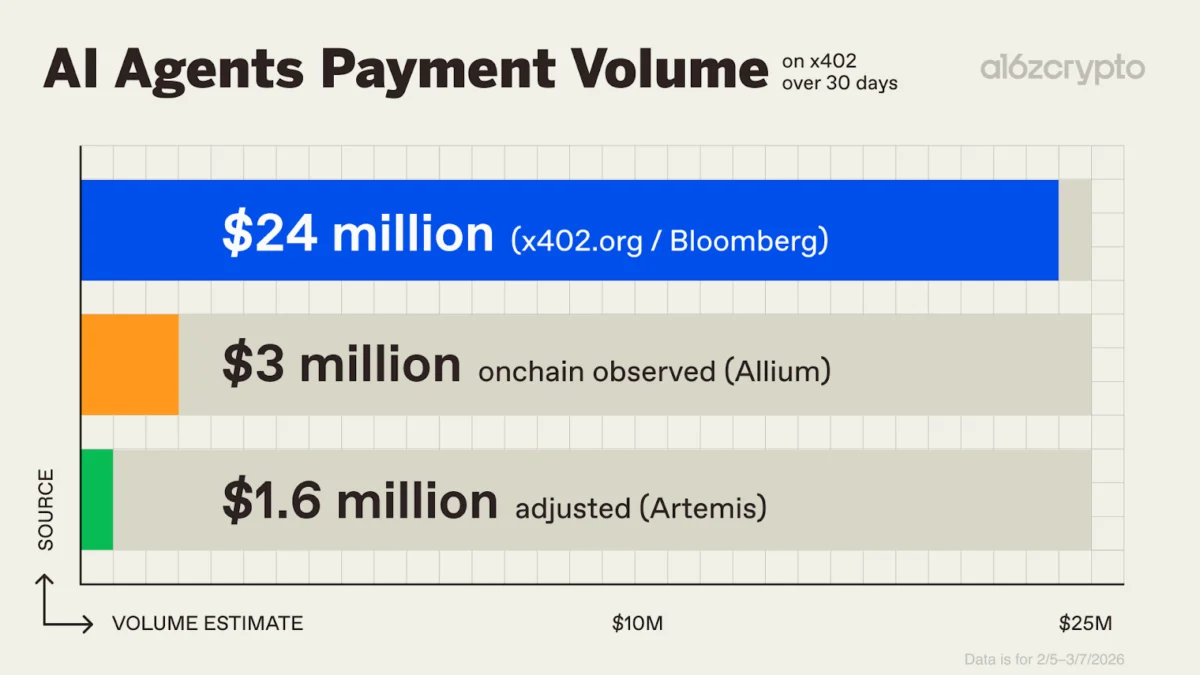

A significant development highlighted by Bernstein is Coinbase’s x402 protocol. x402 is a payment standard developed by the cryptocurrency exchange giant, designed to enable AI agents to automatically make payments over the internet, often for API access or data services. The protocol aims to simplify the integration of crypto payments into existing web infrastructure. However, Bernstein’s note indicates that the traction for x402 has been modest, recording approximately $24 million in stablecoin volume over the past 30 days according to their chart.

Another key player entering this space is Tempo, a Stripe-backed entity that recently launched its blockchain and payment protocol specifically tailored for machine payments. In its initial week, Tempo’s protocol recorded roughly $5,000 in stablecoin volume, indicating the very early stages of market adoption for these specialized solutions.

Further cementing the growing trend, Visa’s crypto division, a global leader in payment technology, also launched a tool enabling AI agents to make same-day payments. This move by a legacy financial institution like Visa signals a broader recognition of the inevitable shift towards autonomous financial interactions and the need for robust infrastructure to support them. These concurrent developments from diverse industry players – a major crypto exchange, a fintech innovator backed by a payment processing giant, and a global card network – underscore the strategic importance being placed on the future of AI-driven payments.

Navigating Early Data: The Wash Trading Conundrum

While the enthusiasm for AI-driven payments is palpable, the early reported transaction volumes for these nascent protocols have drawn scrutiny. Bernstein’s initial figure of $24 million for Coinbase’s x402 protocol over 30 days, while modest in the grand scheme of crypto, raised eyebrows among some industry observers.

Noah Levine, a partner at venture capital firm a16z (Andreessen Horowitz), provided a critical perspective on these metrics. Utilizing a wash trading filter developed by Artemis Analytics, Levine revealed a significantly lower adjusted volume for x402. After applying this filter, the AI Agent payment volume on x402 amounted to only $1.6 million, a stark reduction from the initial $24 million reported by some news outlets, including Bloomberg.

Wash trading is a practice where an entity simultaneously buys and sells the same asset to create artificial trading volume and misleadingly inflate market activity. While prevalent in some less regulated segments of the crypto market, its potential presence in new protocols highlights the need for robust analytics and transparent reporting. Levine, in a March 11 X post, acknowledged that "$1.6 million is not a big number." However, he quickly pivoted to emphasize the more crucial aspect: "But the infrastructure being built around it is." He pointed out that x402 was already being integrated by major technology companies like Stripe, Cloudflare, Vercel, and Google’s agent payments protocol. This distinction is vital: while current transactional volume might be low due to genuine early adoption or even inflated by questionable practices, the foundational infrastructure being laid by significant industry players signals a strong belief in the long-term potential. The focus, according to Levine, should be on the strategic investments in the underlying technology and integrations rather than immediate, potentially misleading, headline figures.

The Bedrock of Stablecoin Growth: Beyond AI Payments

Despite the futuristic promise of AI-driven payments, Bernstein’s report makes it clear that stablecoins do not solely rely on this emerging use case for their continued growth. In fact, the "bigger point" for Bernstein is that current stablecoin demand is robustly driven by a range of well-established and expanding applications. The report positions AI payments as an "upside case" rather than the "core thesis" for stablecoin adoption.

The primary engines of stablecoin demand, as identified by Bernstein, include:

- Cross-border Business Payments: Stablecoins offer a faster, cheaper, and more transparent alternative to traditional SWIFT transfers for international business transactions, bypassing the inefficiencies of correspondent banking.

- Remittances: For individuals sending money across borders, stablecoins can significantly reduce fees and transfer times, a critical advantage for migrant workers supporting families internationally.

- Card-Linked Products: Integration of stablecoins with debit cards and other payment instruments allows users to spend their digital assets in traditional retail environments, bridging the gap between crypto and everyday commerce.

- Neobanking and Digital Wallets: Many modern digital banking platforms and fintech applications are incorporating stablecoins, offering users new ways to save, send, and receive money with enhanced efficiency.

Bernstein’s analysis provides compelling data to support this broader growth narrative. The firm estimated that total stablecoin payment volume surged from $213 billion in 2024 to an projected $375 billion in 2025. This substantial growth is not confined to a single sector but is led by consumer-to-consumer (C2C) flows, indicating widespread individual adoption. Furthermore, business-to-consumer (B2C), business-to-business (B2B), and consumer-to-business (C2B) activities also witnessed significant increases, highlighting the pervasive integration of stablecoins across various economic interactions. This diversification of use cases provides a strong foundation for stablecoin market expansion, regardless of the pace of AI payment adoption.

Key Players and Market Dominance: Coinbase, Circle, and USDC

In the dynamic landscape of stablecoins, Bernstein identifies specific entities as "best proxies for stablecoin upside" due to their strategic positioning and market share. Cryptocurrency exchange Coinbase and stablecoin issuer Circle are singled out due to their pivotal partnership concerning USD Coin (USDC). USDC, a stablecoin pegged to the U.S. dollar, is co-managed by Circle and Coinbase through the Centre Consortium.

Bernstein argues that USDC is particularly well-positioned to capture a dominant share of future machine-payment activity. This projection is based on two critical factors: USDC’s superior liquidity and its relatively strong regulatory standing among likely candidates. As of 2026, USDC has demonstrated impressive transaction volumes, recording $2.4 trillion in adjusted transaction volume year-to-date. This figure significantly outpaces Tether’s USDt (USDT), another major stablecoin, which recorded $1.4 trillion in adjusted transaction volume over the same period.

USDC’s emphasis on regulatory compliance, transparency through regular attestations of its reserves, and its widespread adoption across various blockchain networks make it an attractive choice for institutional players and developers building automated payment systems. The trust and predictability associated with a well-regulated stablecoin are paramount for enabling autonomous financial transactions, where the stakes of failure or instability are high. The competition between USDC and USDT, while intense, often sees USDC preferred in regulated environments and institutional use cases, precisely the areas where sophisticated AI payment protocols are likely to flourish first.

Broader Implications and Future Outlook

The convergence of AI and stablecoins holds profound implications for the global financial system and the broader digital economy.

- Reshaping Financial Infrastructure: Stablecoins, by offering a digital, programmable, and efficient medium of exchange, could fundamentally alter how value is transferred globally, particularly for microtransactions and cross-border payments. The potential to bypass traditional intermediaries could lead to significant cost savings and increased financial inclusion.

- Regulatory Scrutiny and Evolution: As stablecoins become more integral to the financial system, especially in novel areas like AI payments, regulatory bodies worldwide are intensifying their scrutiny. Issues such as consumer protection, anti-money laundering (AML), combating the financing of terrorism (CFT), and systemic risk will remain central. The development of clear, harmonized regulatory frameworks will be crucial for the widespread adoption and legitimate growth of stablecoins in the AI era.

- Competitive Dynamics: The race to build the infrastructure for AI-driven payments is drawing in a diverse set of competitors, including traditional financial giants (Visa), established fintechs (Stripe), and crypto-native companies (Coinbase, Circle). This competition will likely foster innovation, but also raise questions about interoperability, standardization, and potential market concentration. The success of open protocols like x402 will depend on broad industry adoption and integration.

- New Business Models and Automation: The ability for AI agents to conduct autonomous financial transactions opens the door to entirely new business models. Imagine self-owning vehicles paying for their own fuel or charging, smart homes automatically ordering and paying for groceries, or AI-powered services billing for usage in real-time. This level of automation could unlock unprecedented efficiencies and create value in ways previously unimaginable.

- The "Picks and Shovels" Play: As Noah Levine noted, even if immediate transaction volumes are low, the companies building the foundational infrastructure – the "picks and shovels" – for AI payments are making strategic investments. Companies like Cloudflare, Vercel, and Google integrating these protocols suggest a long-term bet on the eventual maturation of this market.

In conclusion, while the immediate adoption of stablecoins for AI-driven payments remains in its nascent stages, characterized by limited transaction volumes and early data challenges like wash trading, the long-term outlook is exceptionally promising. The fundamental advantages of stablecoins – efficiency, programmability, and rapid settlement – align perfectly with the requirements of an increasingly autonomous, AI-powered economy. However, their continued growth is not solely reliant on this future vision; existing, robust use cases in cross-border payments, remittances, and digital finance continue to fuel their expansion. Companies like Coinbase and Circle, with their strong stablecoin offerings and commitment to regulatory compliance, are well-positioned to capitalize on both the current growth trajectory and the eventual maturation of the AI-driven payment landscape, shaping a future where machines transact with the same fluidity as humans.