While the front-end experience of modern banking often appears seamless, with instant payments and digital asset trading, the underlying infrastructure supporting these transactions remains remarkably complex and largely rooted in legacy systems. This intricate web of operations, built on a foundation of independent ledgers and message-based coordination, leads to significant operational friction, extended settlement times, and substantial annual costs for financial institutions globally. A growing number of major banks and market infrastructures are now exploring and implementing blockchain technology not as a replacement, but as an evolutionary layer designed to enhance efficiency, security, and transparency within this established framework.

The Intricacies of Traditional Banking Infrastructure: A Deep Dive into Reconciliation

At its core, traditional banking relies on a vast network of interconnected yet distinct entities—banks, clearinghouses, custodians, and various intermediaries—each maintaining their own private records of transactions. Every payment, securities trade, or asset transfer necessitates a meticulous process of reconciliation, wherein these disparate ledgers are compared and synchronized to ensure agreement on ownership and transaction finality. This "comparing of notebooks," as it’s often described, is a pervasive and costly exercise.

The sheer volume and complexity of global financial transactions mean that discrepancies are frequent. These often require manual intervention, leading to delays that can stretch wire transfers to several days for settlement. This extended settlement window, known as T+2 (trade date plus two business days) for many securities, ties up significant capital, exposes participants to counterparty risk, and generates billions of dollars in operational expenses annually. Industry estimates suggest that reconciliation and back-office processes can account for a substantial portion of a bank’s operating budget, with inefficiencies costing the global financial sector an estimated $15-20 billion per year. The inherent fragmentation and lack of a single, authoritative source of truth contribute to operational risk, making the system vulnerable to errors, fraud, and delays.

Blockchain as a Foundational Coordination and Execution Layer

The emergence of blockchain technology offers a compelling solution to these deeply ingrained coordination challenges. Fundamentally, a blockchain is a distributed digital ledger that records transactions in a cryptographically secure, immutable, and verifiable manner across a network of participants. Instead of each institution maintaining its own private ledger and then attempting to reconcile it with others, a blockchain-based workflow allows all participating entities to reference a single, shared, and continuously synchronized ledger state.

This paradigm shift from siloed records to a common, tamper-resistant data layer provides four core benefits for banks: enhanced data integrity, streamlined workflows, reduced operational risk, and increased transparency. Unlike the traditional message-based system, where Bank A informs Bank B of a transaction, requiring Bank B to independently update its records, a blockchain environment enables both banks to interact directly with and validate entries on a shared ledger. This eliminates the need for extensive post-transaction reconciliation, as all parties are working from the same real-time information.

The timing for this exploration is crucial. While customer-facing banking applications have undergone rapid modernization, the underlying "plumbing" of the financial system has lagged, often still relying on batch processing and antiquated communication protocols. Blockchain introduces a programmable state layer that can operate alongside existing infrastructure, offering an incremental path to modernization without requiring a complete overhaul of critical systems. This approach allows banks to achieve measurable efficiency gains while upholding stringent regulatory compliance and operational continuity standards.

Key Benefits of Blockchain for the Banking Sector

The strategic integration of blockchain technology promises to deliver transformative advantages across various banking operations:

-

Accelerated Transactions and Settlement: In traditional capital markets, the settlement of securities can take T+2 days, necessitating collateralization and increasing counterparty risk. Blockchain-based solutions can dramatically shorten this cycle, often enabling near-instantaneous (T+0) or atomic settlement. This is particularly impactful when combined with coordinated Delivery-versus-Payment (DvP) and Payment-versus-Payment (PvP) workflows, where the exchange of assets and payments occur simultaneously. By eliminating multi-day post-trade processes, blockchain frees up significant liquidity, reduces operational burdens, and mitigates settlement risk, which can be critical during periods of market volatility. The ability to unlock capital faster allows for more efficient allocation and utilization within the financial system.

-

Enhanced Security and Operational Resilience: Blockchain systems leverage advanced cryptography and distributed consensus mechanisms to validate and secure transactions across multi-party networks. This inherent design significantly strengthens resilience in workflows where data consistency is paramount. By distributing ledger copies and requiring consensus for validation, blockchain reduces reliance on centralized reconciliation points that are susceptible to single points of failure. This distributed architecture minimizes the risk of data manipulation, enhances auditability, and provides a robust defense against cyber threats, thereby increasing the overall integrity of financial transactions.

-

Substantial Cost Reduction Through Automation: One of the most significant cost savings potential lies in the automation capabilities of smart contracts. These self-executing contracts, with predefined "if-this-then-that" logic, can automate a wide array of financial processes that traditionally demand extensive manual intervention. This includes reconciliation, exception handling, corporate actions processing, and compliance checks. By encoding business rules directly into the execution workflows, banks can achieve higher straight-through processing (STP) rates, drastically reduce manual effort, and consequently lower administrative costs. For example, automating corporate actions, which are notoriously complex and error-prone, could save the industry billions annually.

-

Improved Transparency, Trust, and Compliance: A blockchain’s transparent, immutable ledger provides a single, verifiable view of transactions and asset states for all authorized participants. When combined with privacy-preserving identity solutions and granular access controls, blockchains can significantly improve auditability and streamline regulatory reporting without exposing sensitive proprietary data. This shared, trusted record strengthens confidence among institutions, regulators, and clients, fostering a more transparent and accountable financial ecosystem. Regulators can gain real-time insights into market activity, enhancing their oversight capabilities and promoting systemic stability.

Key Blockchain Use Cases in Banking

The practical applications of blockchain technology are diverse and target some of the most complex and costly areas of banking:

-

Payments and Money Transfers: Cross-border payments are infamous for their fragmentation, multiple intermediaries, and delayed finality, leading to high costs and reconciliation overhead. Blockchain-enabled workflows aim to dramatically improve coordination and settlement efficiency in this domain. The development of stablecoins, tokenized deposits, and Central Bank Digital Currencies (CBDCs) is maturing alongside traditional payment rails, offering new avenues for programmable payments. By connecting existing messaging standards (like ISO 20022) to blockchain environments, banks can coordinate execution and settlement against a shared ledger state, reducing operational friction and enhancing transparency without disrupting core payment infrastructure. This could unlock trillions of dollars currently trapped in payment float and significantly reduce transfer fees, particularly for remittances.

-

Clearing and Settlement: This area is arguably one of the most operationally intensive in finance, demanding precise data synchronization across a multitude of entities including custodians, clearinghouses, broker-dealers, and asset servicers. The current system heavily relies on message-based confirmations and extensive post-trade reconciliation across siloed systems. Blockchain can serve as a common coordination layer for post-trade activity, offering consistent access to verified records and substantially reducing reconciliation overhead. As financial assets become increasingly tokenized, standardized reference data and coordinated workflows across both traditional and blockchain environments become critical to achieving faster, lower-risk settlement. This transition has the potential to drastically reduce the capital required to back trades and accelerate market velocity.

-

Trade Finance: The trade finance sector remains heavily reliant on physical documentation, involving a complex ecosystem of banks, logistics providers, insurers, and customs authorities. Disconnected systems and manual paperwork introduce delays, disputes, and elevated fraud risks throughout the trade lifecycle. Blockchain-based workflows can synchronize key trade events—such as shipment status, document issuance, and ownership transfers—across all participants in near real-time. By maintaining a shared, tamper-resistant record, institutions can significantly reduce paperwork, accelerate settlement, and improve trust among parties, all while preserving existing operational roles and responsibilities. This could unlock billions in financing for small and medium-sized enterprises (SMEs) by making trade finance more accessible and efficient.

-

Identity Verification and Compliance: Identity management (Know Your Customer/KYC) and Anti-Money Laundering (AML) compliance are foundational to banking but are often costly and repetitive due to duplicated verification processes across institutions. Customers frequently resubmit sensitive documentation, while banks independently perform similar checks. Blockchain-based identity solutions, particularly those utilizing verifiable credentials, enable individuals and institutions to prove specific attributes (e.g., KYC status, eligibility for a financial product) without repeatedly sharing underlying personal data. This approach reduces duplication in compliance workflows, supports jurisdiction-specific regulatory requirements, and strengthens privacy protections, leading to a more efficient and secure onboarding process for clients.

Real-World Examples of Blockchain Adoption in Banking

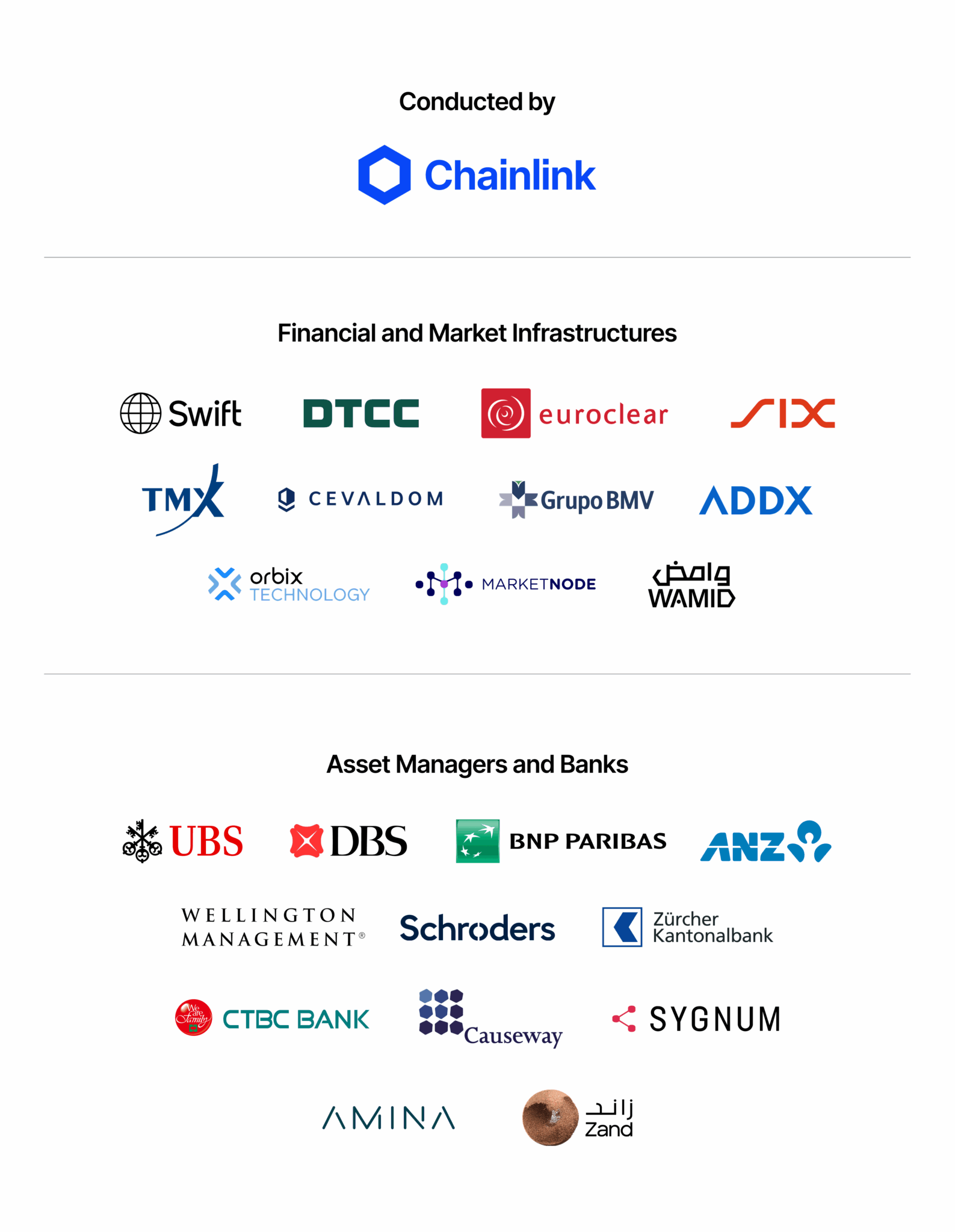

The theoretical benefits of blockchain are increasingly being demonstrated through tangible, production-grade initiatives involving leading financial institutions and market infrastructures. These projects underscore a pragmatic, standards-based integration approach, connecting blockchain platforms with existing enterprise systems and regulatory frameworks. Chainlink, as a decentralized oracle network, has played a pivotal role in powering critical data, interoperability, compliance, and privacy solutions across many of these groundbreaking use cases.

-

SWIFT Connectivity and Cross-Chain Settlement: A landmark collaboration between Chainlink and SWIFT has enabled financial institutions to connect to various public and private blockchain networks using SWIFT’s existing infrastructure and messaging standards. By leveraging Chainlink’s Cross-Chain Interoperability Protocol (CCIP), these initiatives demonstrate how tokenized asset settlement workflows can be coordinated seamlessly alongside traditional payment rails. Under the Monetary Authority of Singapore’s Project Guardian, SWIFT, UBS Asset Management, and Chainlink successfully demonstrated the issuance and settlement of tokenized assets using existing fiat payment infrastructure, offering a clear, standards-based pathway for institutional adoption without necessitating the replacement of core messaging systems. This signifies a crucial step towards bridging the traditional financial world with the nascent digital asset economy.

-

Standardizing Corporate Actions Across Global Markets: Corporate actions processing, such as dividends, stock splits, and mergers, is a notoriously complex and costly area, estimated to cost the industry billions annually due to manual processes and reconciliation challenges. Chainlink has powered a global industry initiative involving 24 financial institutions and market infrastructures, including SWIFT, DTCC, Euroclear, UBS, DBS Bank, ANZ, BNP Paribas, Wellington Management, and Schroders. This collaborative effort aims to transform fragmented, manual corporate actions workflows into standardized, near-real-time processes by combining oracle networks and blockchains with structured data extraction and validation. The result is projected to be significantly reduced operational costs, lower error rates, and considerably less reconciliation overhead across diverse jurisdictions.

-

Tokenized Fund and Digital Asset Settlement: Several major institutional initiatives have leveraged Chainlink for tokenized assets and stablecoins. Collaborations with Kinexys by J.P. Morgan, Ondo Finance, and other market participants have showcased atomic Delivery-versus-Payment (DvP) settlement workflows. These demonstrations coordinate both the asset and payment legs of a transaction to reduce settlement risk and operational complexity. The ability to execute and coordinate within a shared, programmable environment provides greater certainty and efficiency for tokenized asset settlement, laying the groundwork for a more agile digital asset market.

-

Cross-Border Compliance and Identity Workflows: In Asia, Chainlink has facilitated compliant cross-chain settlement under initiatives such as the Hong Kong Monetary Authority’s e-HKD+ program. Institutions including ANZ Bank, China AMC, and Fidelity International utilized Chainlink infrastructure to verify investor eligibility, enforce jurisdiction-specific controls, and execute tokenized asset transactions across borders. These workflows demonstrate how blockchain-based settlement can meet stringent regulatory requirements while preserving privacy and supporting complex cross-jurisdictional operations, which is vital for global finance.

-

Integration with Institutional Messaging and Transfer Agency Systems: The Chainlink Runtime Environment (CRE) enables financial institutions to initiate on-chain fund workflows directly from existing enterprise infrastructure, including ISO 20022 messages transmitted via SWIFT. In a significant collaboration with UBS Tokenize, Chainlink demonstrated how subscription and redemption requests for tokenized funds could be orchestrated on-chain through standardized transfer agency workflows. This innovation allows for the integration of blockchain capabilities without requiring the replacement of core banking systems or operational processes, proving that legacy and new technologies can coexist and complement each other.

Challenges and Future Considerations for Blockchain in Banking

Despite significant progress and promising real-world applications, the widespread adoption of blockchain in banking still faces several challenges. These include navigating complex regulatory frameworks across different jurisdictions, ensuring the scalability of blockchain networks to handle the immense volume of global financial transactions, addressing interoperability issues between diverse blockchain platforms and legacy systems, and managing the inherent complexities of integrating new technology into deeply entrenched operational structures. These realities explain why most institutional initiatives prioritize standards-based integration, incremental deployment, and controlled automation, rather than radical, wholesale overhauls. The industry is actively working through these hurdles, often through collaborative consortia and regulatory sandboxes, to establish best practices and standardized approaches.

Chainlink’s Pivotal Role in Driving Blockchain Adoption Across the Banking Sector

Modern banking’s adoption of blockchain requires more than just the ability to issue tokens. It necessitates trusted and reliable data feeds, secure cross-network coordination, and seamless integration with existing institutional workflows and compliance frameworks. The Chainlink platform addresses these critical requirements by enabling banks to operationalize blockchain-based processes in production environments.

Chainlink facilitates this by providing:

- Secure and Reliable Data: Access to high-quality, tamper-proof market data and reference data, essential for accurate on-chain financial operations.

- Cross-Chain Interoperability: The ability to securely connect and transfer value and data between different blockchain networks and traditional systems, crucial for fragmented financial markets.

- Enhanced Privacy and Confidentiality: Solutions that allow sensitive institutional data to remain private while still leveraging the benefits of a shared ledger, satisfying strict regulatory and business confidentiality requirements.

- Standards-Based Integration: Tools and frameworks that enable integration with existing enterprise systems and industry standards (like ISO 20022), minimizing disruption and facilitating smoother transitions.

By enabling standards-based connectivity between legacy systems and advanced blockchain environments, Chainlink empowers financial institutions to innovate across both traditional finance (TradFi) and nascent on-chain finance (OnchainFi). This approach allows banks to modernize and integrate blockchain workflows that deliver tangible value, all while maintaining the stringent reliability, security, and control standards demanded by global capital markets. The ongoing evolution points towards a future where blockchain acts as an invisible yet indispensable layer, making banking more efficient, secure, and resilient for everyone.