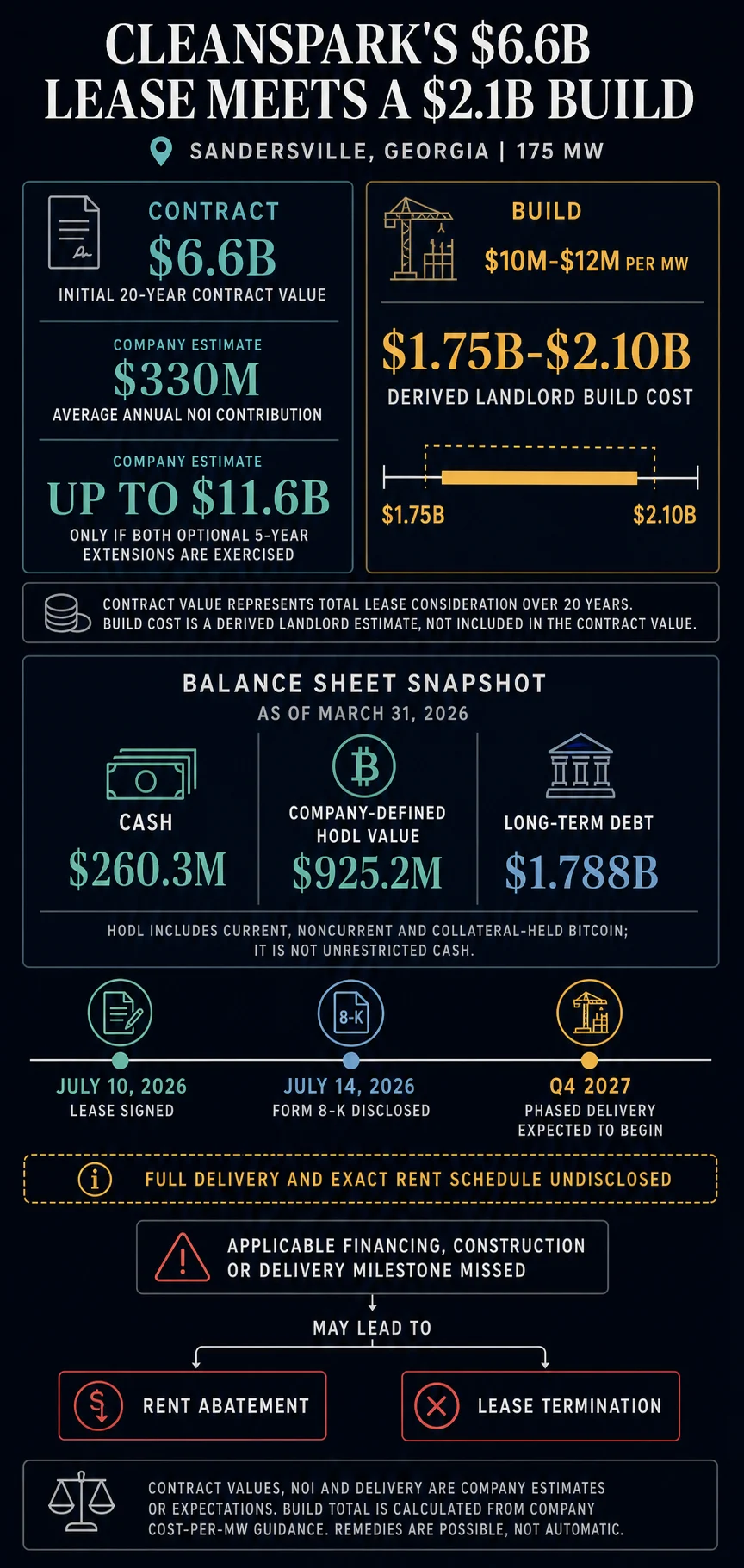

CleanSpark Inc. (NASDAQ: CLSK), a prominent leader in the Bitcoin mining and data center development sector, has formalized a significant 20-year triple-net lease for its Sandersville, Georgia, facility, signaling a major strategic expansion into high-performance computing (HPC) and artificial intelligence (AI) infrastructure. The agreement, executed on July 10 and disclosed in a Form 8-K filing on July 14, covers 175 megawatts (MW) of critical IT load. While the contract is projected to generate billions in revenue over its lifespan, the company now faces the formidable task of securing between $1.75 billion and $2.10 billion in financing to complete the necessary data center construction.

This move marks a pivotal moment for CleanSpark as it transitions from a pure-play Bitcoin miner to a diversified infrastructure provider for the burgeoning AI sector. The scale of the Sandersville project is unprecedented for the company, with an estimated initial contract value of $6.6 billion. If the anonymous tenant exercises two optional five-year extensions, the total value could climb to $11.6 billion. Despite the massive revenue potential, the immediate capital requirements present a significant hurdle that will test the company’s balance sheet and its ability to leverage the creditworthiness of its new global technology partner.

The Sandersville Agreement: Terms and Projections

The Sandersville lease is structured as a binding 20-year triple-net (NNN) agreement, a common framework in commercial real estate where the tenant is responsible for most operational costs, including taxes, insurance, and maintenance. According to the SEC filing, the lease includes annual rent escalators and covers the entirety of the 175 MW capacity at the Georgia campus. CleanSpark anticipates that the project will contribute approximately $330 million in average annual net operating income (NOI) once fully operational.

The identity of the tenant remains undisclosed, described only as a "high-investment-grade global technology company." This anonymity is typical in large-scale data center deals involving hyperscalers or major cloud providers, who often seek to keep their infrastructure footprints confidential for competitive reasons. CleanSpark has emphasized that the tenant’s strong credit profile is a cornerstone of the deal, as it is expected to facilitate access to the specialized financing required for a build of this magnitude.

However, the "triple-net" designation does not absolve CleanSpark of the initial construction burden. The company’s own estimates suggest landlord project costs will range from $10 million to $12 million per MW. For the 175 MW Sandersville site, this results in a calculated capital expenditure (CapEx) requirement of $1.75 billion to $2.10 billion.

The Capital Expenditure Challenge

The primary challenge facing CleanSpark is the gap between its current liquidity and the projected construction costs. As of March 31, 2026, the company reported a financial position that, while robust for a mining operation, falls short of the requirements for a multi-billion-dollar data center build.

CleanSpark’s reported cash reserves stood at $260.3 million, with an additional $925.2 million in "Bitcoin HODL value." Even when combining these figures, the total liquidity of roughly $1.18 billion covers only about 56% to 67% of the low-end construction estimate. Furthermore, the HODL figure includes Bitcoin that may be held by counterparties under collateral arrangements, meaning it is not entirely unrestricted or immediately available for capital expenditure without potentially triggering tax events or margin risks.

The financial pressure is further highlighted by the company’s existing debt load. As of the end of March 2026, CleanSpark reported $1.788 billion in long-term debt and total liabilities of $1.927 billion. The projected Sandersville build cost is roughly equivalent to 98% to 117% of the company’s existing long-term debt, suggesting that a significant expansion of the balance sheet will be necessary to bring the project to fruition.

Chronology of the Sandersville Development

The path to the current lease agreement reflects a rapid acceleration of CleanSpark’s infrastructure goals:

- July 10, 2026: CleanSpark enters into the binding 20-year infrastructure lease for the 175 MW Sandersville campus.

- July 14, 2026: The company files a Form 8-K with the SEC, disclosing the financial estimates and terms of the agreement.

- Q4 2027: Phased delivery of the IT load is expected to begin. This timeline suggests a construction window of approximately 15 to 18 months before the first phase of the tenant’s equipment can be energized.

- Post-2027: The commencement of full rent payments will depend on the completion of subsequent phases. The exact schedule for the full 175 MW delivery has not yet been made public.

This timeline places CleanSpark in a race to secure funding and break ground to meet the Q4 2027 delivery target. Any delays in financing could jeopardize the phased delivery schedule and, consequently, the projected revenue stream.

Financing Pathways and Risk Distribution

CleanSpark has several avenues for funding the Sandersville build, each carrying different implications for shareholders and the company’s risk profile.

1. Project-Level Financing

The most likely path involves project-specific debt. Because the lease is backed by a high-investment-grade tenant, lenders may be willing to provide non-recourse or limited-recourse financing based on the contractual cash flows of the lease itself. This would isolate the debt to the Sandersville asset, potentially protecting the broader company from a default. However, lenders may still require a significant equity contribution from CleanSpark or corporate guarantees.

2. Bitcoin-Backed Borrowing

CleanSpark has historically utilized its Bitcoin holdings to secure credit. As of March 31, 2026, the company had $400 million in unused Bitcoin-backed credit lines. Utilizing these would require pledging a portion of its 9,000+ BTC (based on HODL value) as collateral. This path preserves Bitcoin ownership but exposes the company to liquidation risk if the price of Bitcoin drops significantly during the construction phase.

3. Equity Dilution

The company could opt to raise capital through the issuance of new common stock or equity-linked securities. While this avoids increasing debt, it dilutes existing shareholders. Given the $2.1 billion requirement, an equity raise of this size would represent a substantial portion of the company’s market capitalization.

4. Convertible Notes

CleanSpark has previously utilized zero-coupon convertible notes, with a carrying balance of $1.769 billion reported in early 2026. While these offer low-interest costs, they eventually convert to equity, leading to future dilution.

The ultimate financing structure will determine whether the "risk" of the project stays with the project’s cash flows or is pushed onto the company’s Bitcoin reserves and shareholders.

Operational Milestones and Execution Risks

The $6.6 billion contract value is not a guaranteed windfall; it is contingent upon CleanSpark meeting rigorous performance and construction milestones. The SEC filing notes that the agreement includes covenants related to financing, construction progress, and delivery dates.

Failure to meet these milestones could result in rent abatements—where the tenant pays reduced or no rent for a period—or, in extreme cases, the termination of the lease. These "milestone remedies" ensure that the tenant is protected if CleanSpark fails to deliver the high-spec environment required for modern AI workloads, which often require advanced liquid cooling and redundant power systems far more complex than standard Bitcoin mining setups.

Furthermore, the reported $378.3 million net loss in the quarter ending March 31, 2026, serves as a reminder of the volatility inherent in CleanSpark’s core business. While much of that loss was attributed to non-cash Bitcoin fair-value adjustments ($224.1 million), it underscores the fact that the company’s internal cash generation is heavily tied to the crypto market, making external financing for the Sandersville project even more critical.

The Broader Context: The Great AI Pivot

CleanSpark’s move is part of a larger trend where Bitcoin miners are repurposing their power assets for AI. The "Great AI Pivot" is driven by the massive demand for data center space from companies like NVIDIA, Microsoft, and Google. Competitors such as Core Scientific and Hut 8 have already signed similar deals, seeking to trade the volatility of Bitcoin mining rewards for the steady, long-term cash flows of enterprise AI leases.

CleanSpark’s Sandersville deal is particularly ambitious due to its 20-year term, which is significantly longer than the 10-to-12-year terms seen in many standard data center leases. This duration suggests that the tenant views the Sandersville site as a long-term strategic hub for its AI operations.

Beyond Georgia, CleanSpark is eyeing even larger expansions. The company recently signed a letter of intent (LOI) and an exclusivity agreement with the same tenant for a 718-acre portfolio in Texas, representing up to 885 MW of potential capacity. While the Texas deal is not yet a binding lease, it illustrates the scale of CleanSpark’s ambitions and the potential for the company to become one of the largest specialized data center operators in the United States.

Conclusion and Market Outlook

The Sandersville lease transforms CleanSpark’s fundamental value proposition. It moves the company from being a speculative play on Bitcoin prices to an infrastructure partner for the global technology elite. However, the "infrastructure" label comes with infrastructure-sized costs.

The coming months will be critical as CleanSpark seeks to finalize its financing package. The market will be watching for the specific terms of the debt: the interest rates, the collateral requirements, and the extent of any equity dilution. If CleanSpark can successfully fund the $2.1 billion build without over-leveraging its balance sheet or liquidating its Bitcoin reserves, it will have successfully navigated one of the most significant transitions in the history of the digital asset industry.

For now, the Sandersville project remains a high-stakes endeavor. The $6.6 billion revenue target is a powerful incentive, but the path to Q4 2027 is paved with significant capital requirements and operational hurdles that CleanSpark must clear to prove it can compete in the elite world of AI infrastructure.