The Decentralized Finance (DeFi) sector demonstrated remarkable resilience and growth throughout 2025, culminating in a robust market position as of early 2026. Despite persistent security challenges and regulatory scrutiny, the ecosystem expanded its total value locked (TVL) and diversified its revenue streams, cementing its role as a significant force in the broader digital asset economy. Key metrics from June and December 2025 indicate dynamic shifts in protocol dominance, an acceleration in multi-chain adoption, and a growing emphasis on real-world asset (RWA) integration.

Market Size and Dominance: A Snapshot of Capital Flows

The DeFi market’s sheer size is primarily gauged by its Total Value Locked (TVL), a critical metric representing the aggregate value of all assets deposited in DeFi protocols. As of June 2025, the landscape of leading protocols by TVL showcased both established giants and rapidly ascending innovators. Aave, a dominant lending protocol, held the top position with an impressive $24.4 billion TVL, experiencing a significant 19.78% increase over the preceding 30 days. This growth underscores continued confidence in its multi-chain lending infrastructure and perhaps, its strategic embrace of institutional engagement and RWA-backed collateral.

Close behind, Lido, a liquid staking derivative protocol, commanded $22.6 billion, though it saw a 19.81% decline in the same period. This fluctuation could be attributed to various factors, including shifts in staking yields, broader market sentiment towards liquid staking, or the emergence of competitive alternatives. EigenLayer, a relatively newer entrant focusing on restaking, rapidly ascended to $10.9 billion TVL, despite a 20.53% dip, highlighting the immense capital flowing into innovative yield-generation strategies. Its single-blockchain focus on Ethereum for restaking indicates a concentrated yet highly valued market segment.

Other notable protocols in the top ten included Sky, which experienced a remarkable 55.59% surge to $5.855 billion, and Spark, which nearly doubled its TVL with a staggering 95.54% increase to $4.392 billion. These substantial growths suggest successful new product launches, aggressive liquidity incentives, or significant institutional inflows. Conversely, protocols like Ethena (-26.38%) and Pendle (-38.36%) saw notable contractions, indicating that capital in DeFi remains highly fluid and responsive to yield opportunities and perceived risks. Uniswap, the stalwart decentralized exchange (DEX), maintained a strong presence with $3.817 billion across an expansive 30 blockchains, albeit with a modest 4.60% decrease, reflecting the competitive nature of the DEX market. The diversity in these movements illustrates a maturing market where capital efficiency and innovative mechanisms are constantly being tested.

Revenue Generation: A Deeper Look at Protocol Economics

Beyond TVL, the revenue generated by DeFi protocols offers crucial insights into their sustainable economic models and value proposition. Data from Binance Research as of December 31, 2025, highlighted a shift in revenue leadership, particularly towards Solana-based protocols. Meteora, a liquidity/DEX protocol on Solana, led the pack with an estimated US$1.25 billion in 2025 fee revenue. Its success is largely attributed to an efficient Dynamic Liquidity Market Maker (DLMM) model, which proved particularly effective for volatile assets, capturing significant trading volume and fees.

Jupiter, another Solana-based protocol specializing in aggregation and perpetuals, followed closely with US$1.1 billion. Its ability to aggregate routing across various sources and facilitate high-leverage perpetual trading capitalized on Solana’s speed and low transaction costs, drawing in a substantial trader base. Uniswap, while not leading in 2025 revenue, still demonstrated robust performance with US$1.06 billion. Its multi-chain presence and continuous innovation with V3/V4 pool fees ensured it remained a formidable revenue generator, particularly from its large long-tail trading volume.

Aave secured US$809 million, reinforcing its position through institutional usage and the burgeoning RWA-backed collateral market, which attracts more stable and larger capital. Hyperliquid, a derivatives platform operating on its own L1, generated over US$800 million, benefiting from high-frequency trading and market-maker activity that thrives on its specialized infrastructure. This revenue distribution underscores the increasing competition and specialization within DeFi, with high-performance blockchains like Solana gaining traction for specific use cases.

Regional Adoption and Future Trajectories

The global adoption of DeFi continued its upward trajectory in 2025, with Chainalysis identifying India and the United States as primary leaders. These countries exhibited the highest DeFi value received, indicating strong retail and institutional engagement. In India, factors such as a large tech-savvy population, growing economic digitalization, and increasing awareness of alternative financial services likely contributed to this surge. The United States, with its mature financial markets and significant venture capital investment in crypto, continued to be a hub for innovation and capital deployment in DeFi.

While specific rankings for the Top 20 Global Crypto Adoption Index based on DeFi value received were not detailed, the inclusion of these two giants sets a precedent for understanding global trends. The European DeFi market also demonstrated significant activity in 2025. With the impending and operational impacts of the Markets in Crypto-Assets (MiCA) regulation, Europe began to establish a more harmonized, albeit stringent, regulatory framework. This clarity, while initially perceived as a potential dampener, is increasingly viewed by industry participants as a catalyst for institutional adoption and long-term stability. Analysts project a steady growth trajectory for DeFi across regions from 2025 to 2033, with emerging economies potentially outpacing developed markets as financial inclusion and digital literacy improve.

Key Sectors Driving DeFi Innovation

The DeFi ecosystem is a multifaceted landscape composed of several interconnected sectors, each contributing uniquely to its functionality and growth.

Decentralized Exchanges (DEXs) remain the bedrock of DeFi, enabling peer-to-peer cryptocurrency trading without intermediaries. The evolution from basic Automated Market Makers (AMMs) to sophisticated models like concentrated liquidity (Uniswap V3) and Dynamic Liquidity Market Makers (DLMMs) used by Meteora, has significantly improved capital efficiency and reduced slippage. DEXs like Uniswap and Jupiter continue to process billions in daily volume, reflecting their critical role in price discovery and liquidity provision. However, they face ongoing challenges related to impermanent loss for liquidity providers and regulatory scrutiny over listing practices.

Lending protocols, exemplified by Aave, facilitate decentralized borrowing and lending of cryptocurrencies. These platforms typically employ overcollateralization, though innovations like flash loans and experiments in uncollateralized lending through credit scores or reputation are continually explored. The ability to earn interest on deposited assets or access capital without traditional credit checks has democratized finance, but also introduced unique risks, especially during periods of high market volatility.

Stablecoins are indispensable to the DeFi ecosystem, providing a much-needed hedge against the inherent volatility of cryptocurrencies. Tether (USDT), USD Coin (USDC), and Dai (DAI) continue to dominate, serving as primary mediums for trading, lending, and payments within DeFi. The growth and increasing regulatory focus on stablecoins, particularly their backing reserves and transparency, underscore their systemic importance and the ongoing debate about their classification and oversight.

The integration of Real World Assets (RWAs) into DeFi represents a significant bridge between traditional finance and blockchain. This sector involves the tokenization of tangible and intangible assets like real estate, bonds, and commodities, bringing substantial liquidity and utility to DeFi. Aave’s early adoption of RWA-backed collateral is a testament to this trend, offering new avenues for institutional participation and expanding the potential use cases for decentralized finance beyond purely crypto-native assets. This trend is expected to accelerate, unlocking vast pools of capital and diversifying risk profiles within DeFi.

Prediction Markets like Augur and Gnosis offer decentralized platforms for users to bet on future events, ranging from political outcomes to sports results. They leverage the "wisdom of the crowd" for forecasting and provide an alternative to centralized betting houses, emphasizing transparency and censorship resistance. While niche, they represent an intriguing application of decentralized technology for information aggregation.

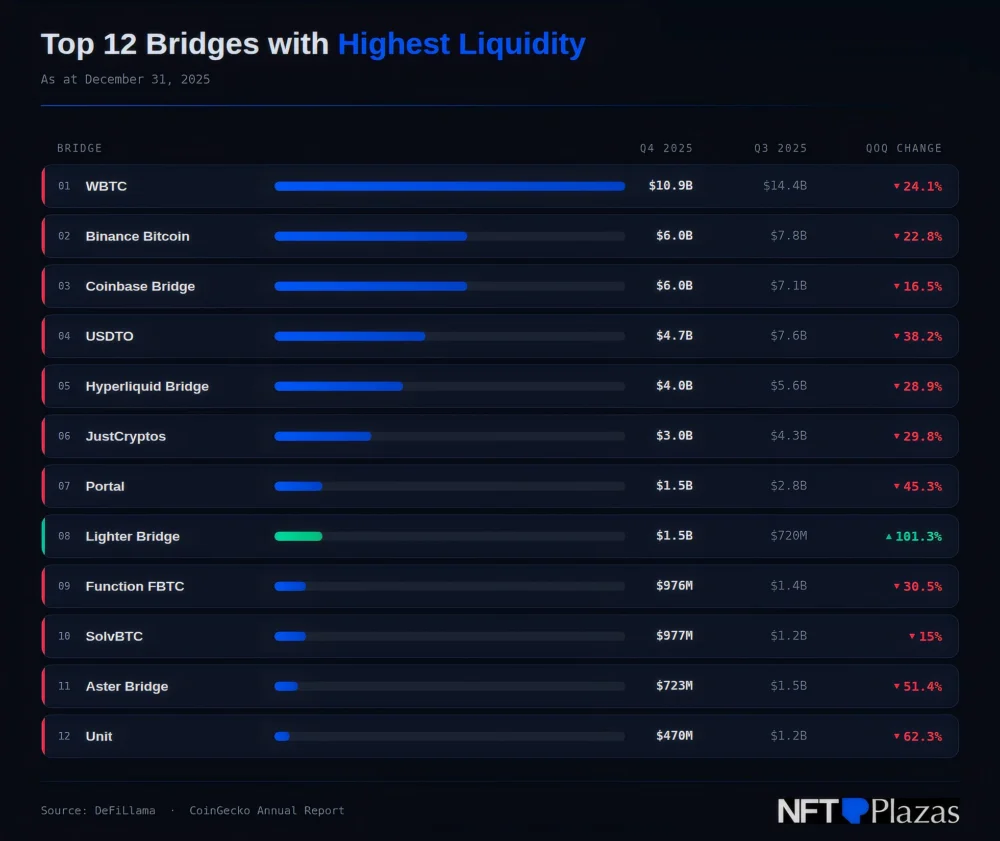

Bridges are crucial for interoperability, allowing assets and data to flow between different blockchain networks. Their importance has grown exponentially with the rise of multi-chain ecosystems. However, bridges have also become a primary target for sophisticated exploits due to their complex smart contract interactions and large liquidity pools. The image depicting "Top DeFi Bridges by Liquidity" highlights the critical infrastructure these protocols provide, but also implicitly warns of the concentrated risk they represent. Maintaining robust security for these vital links remains a top priority for the entire ecosystem.

Decentralized Autonomous Organizations (DAOs) form the governance backbone for many DeFi protocols. These organizations allow token holders to vote on key decisions, from protocol upgrades and parameter changes to treasury management. While promoting transparency and community ownership, DAOs grapple with challenges such as voter apathy, concentration of voting power among large token holders, and the complexities of decentralized decision-making at scale.

Decentralized Applications (DApps) represent the user-facing layer of the blockchain ecosystem. The third quarter of 2025 saw significant engagement, with "Total UAW" (Unique Active Wallets) serving as a key metric for user activity. KAI-CHING led with 177 million UAW, followed by World of Dypians (135 million), HOT Protocol (78.5 million), Raydium (50.2 million), and KGeN (37.2 million). This data indicates a strong user base for applications beyond pure financial transactions, with gaming, social platforms, and specialized utilities gaining considerable traction. The diversification of DApps into key categories like gaming, social media, metaverses, and various utility tools suggests a broadening appeal of blockchain technology to a mainstream audience, moving beyond early adopter financial speculation.

Security, Hacks, and Exploits: A Persistent Challenge

Despite the rapid innovation and growth, the DeFi sector continues to be plagued by security vulnerabilities, hacks, and exploits. 2025 witnessed numerous notable incidents, underscoring the persistent challenges in securing complex smart contract systems and cross-chain infrastructure. While specific details of every incident were not provided, common attack vectors included flash loan attacks, reentrancy vulnerabilities, oracle manipulation, private key compromises, and bridge exploits. These incidents often resulted in significant financial losses, eroding user trust and attracting intense regulatory scrutiny.

The cumulative impact of these exploits is substantial, not only in monetary terms but also in shaping public perception and investor confidence. Each hack serves as a stark reminder of the nascent nature of the technology and the critical need for continuous security enhancements. Industry efforts have intensified, focusing on rigorous smart contract auditing, bug bounty programs, formal verification methods, and multi-signature security for critical operations. Furthermore, protocols are increasingly adopting advanced monitoring systems and incident response plans to mitigate damages. However, the sophistication of attackers continues to evolve, necessitating a proactive and adaptive approach to security from developers and users alike. Regulatory bodies globally are also pushing for clearer accountability and stronger security standards to protect consumers and maintain market integrity.

Conclusion: Navigating Growth and Challenges

The DeFi market, as observed in early 2026, is a vibrant and rapidly evolving ecosystem characterized by both tremendous innovation and inherent risks. The strong TVL and revenue figures, coupled with expanding regional adoption, signal a maturing sector that is increasingly integrated into the global financial landscape. The diversification into specialized protocols, the rise of multi-chain strategies, and the burgeoning RWA sector all point towards a future where decentralized finance plays a more pervasive role.

However, the shadow of security breaches looms large, serving as a constant reminder that technological advancement must be matched by robust security practices and a commitment to protecting user assets. The ongoing dialogue around regulation, particularly in regions like Europe, suggests a move towards a more structured environment, which could foster greater institutional participation while simultaneously presenting compliance challenges for existing protocols. The next few years will likely see continued innovation in areas like scalability, user experience, and cross-chain interoperability, alongside a concerted effort to enhance security and navigate the complex global regulatory landscape, ultimately shaping the long-term trajectory and mainstream adoption of decentralized finance.