Cross-border payments, the indispensable arteries of global commerce, financial markets, and remittances, underpin a colossal global payment market valued at approximately $1 quadrillion annually. For decades, the movement of money between different countries has been a critical yet often cumbersome process, frequently characterized by inefficiency, opacity, and high costs. Traditional systems, heavily reliant on a web of intermediaries and batch-based settlement processes, introduce significant friction, leading to slower transaction times, elevated fees, and inherent risks. However, a new paradigm is emerging: blockchain technology, offering shared, programmable settlement layers that operate ceaselessly, 24/7, and finalize transactions in mere seconds. This article delves into how blockchain technology fundamentally improves cross-border payments and outlines the pivotal role of platforms like Chainlink in powering reliable, transparent, and secure cross-border and cross-chain transactions through its standards for data, interoperability, compliance, and privacy.

The Enduring Challenges of Traditional Cross-Border Payments

The current architecture for cross-border payments, largely built on the correspondent banking model, is a relic of an earlier financial era ill-suited for the demands of a hyper-connected global economy. When an individual or business wishes to send money from one country to another, the transaction typically navigates a complex journey through multiple banks and financial institutions, each acting as an intermediary. This convoluted path introduces several systemic challenges:

- Sluggish Settlement Times: Transactions can take days, or even weeks, to settle. This delay stems from the necessity for banks to verify funds across different ledgers, reconcile accounts, manage varying business hours across time zones, and process payments in batches rather than continuously. This protracted settlement ties up capital, creates liquidity challenges, and hinders efficient business operations.

- Exorbitant Costs and Opaque Fees: Each intermediary in the payment chain charges a fee, cumulatively driving up the total cost of a transaction. These fees can be a significant burden, particularly for remittances, where every dollar counts for recipients in developing nations. Furthermore, currency exchange rates often include hidden markups, and the exact cost of a transaction is frequently unclear to senders and recipients until after the payment is completed, leading to a lack of transparency. According to some estimates, traditional cross-border payments can incur fees ranging from 5% to 10% or more, far higher than domestic transactions.

- Operational Complexity and Error Potential: The manual processes involved in reconciliation, compliance checks, and messaging between disparate systems are prone to human error. Such errors necessitate costly and time-consuming investigations and corrections, further delaying payments and increasing operational overhead for financial institutions.

- Limited Transparency and Traceability: Once a payment is initiated, tracking its real-time status can be challenging. Senders and recipients often lack clear visibility into where their money is in the payment pipeline, leading to frustration and increased customer service inquiries. This opacity also complicates auditing and regulatory oversight.

- Increased Risk Exposure: The extended settlement periods expose parties to various risks, including counterparty risk (the risk that a party defaults before settlement) and liquidity risk. The need for banks to pre-fund nostro and vostro accounts in various currencies also ties up significant capital, which could otherwise be deployed more productively.

- Regulatory Fragmentation: Navigating diverse regulatory frameworks across multiple jurisdictions adds layers of complexity. Each country has its own Know Your Customer (KYC) and Anti-Money Laundering (AML) requirements, sanctions lists, and data privacy laws, which must be meticulously adhered to by every intermediary in the payment chain. This patchwork of regulations often necessitates redundant checks and specialized compliance teams, contributing to costs and delays.

Blockchain Technology: A Paradigm Shift for Global Transactions

At its core, a blockchain is a highly secure and reliable distributed ledger technology (DLT) that allows participants to record transaction activity, store data, and exchange value in a decentralized network. For payments, this level of reliability, underpinned by cryptographic security and consensus mechanisms, enables near-instant finality, always-on operations, and automated value transfer workflows. The advent of blockchain technology offers a fundamental re-imagining of how cross-border payments can function, addressing many of the inherent inefficiencies of legacy systems.

- Unprecedented Speed and Efficiency: Blockchain networks enable near-instant settlement, with transaction finality often reached within seconds or minutes, a stark contrast to the days-long settlement times of traditional systems. This dramatic reduction in time significantly mitigates counterparty and settlement risk. Unlike traditional banking systems bound by specific business hours and cutoff times, blockchains operate 24 hours a day, 7 days a week, 365 days a year, allowing payments to move continuously across any time zone without delay. This continuous operation eliminates the bottlenecks associated with weekend closures and public holidays, ensuring an always-on global payment rail.

- Substantial Cost Reduction: By replacing multiple layers of intermediaries with shared, immutable infrastructure, blockchains streamline the payment process and significantly reduce associated costs. On-chain transfers eliminate the need for numerous clearing entities, correspondent banks, and the associated fees, helping lower the all-in cost of cross-border payments for both businesses and consumers. This efficiency can translate into savings of several percentage points per transaction, freeing up capital for productive use.

- Enhanced Transparency and Security: Payments executed on blockchain networks are verifiable in real-time by all participating parties, providing unprecedented visibility into transaction status and associated fees. The built-in cryptographic guarantees and immutable nature of distributed ledgers ensure data integrity, making it exceptionally difficult to commit fraud or tamper with transaction records. Every transaction is time-stamped and recorded permanently, creating an unalterable audit trail. Additionally, on-chain records simplify audits and reporting processes, offering a clear and accessible history of all transactions, which is invaluable for regulatory compliance and dispute resolution.

- Increased Accessibility and Financial Inclusion: By reducing costs and simplifying the payment process, blockchain technology can extend financial services to underserved populations globally. Individuals and small businesses in remote areas, who may lack access to traditional banking infrastructure, can participate in the global economy through more affordable and accessible digital payment solutions.

Key Use Cases of Blockchain in Cross-Border Payments

The transformative potential of blockchain extends across various sectors requiring efficient cross-border money movement:

- Remittances: For migrant workers sending money home, blockchain offers a lifeline. The ability to send funds quickly and cheaply directly to recipients bypasses expensive money transfer operators, ensuring a larger portion of the remittance reaches the intended family members. This has significant socio-economic implications for developing economies.

- Corporate Treasury Management: Multinational corporations can leverage blockchain for streamlined intra-company transfers, supplier payments, and liquidity management across different jurisdictions. Real-time settlement and reduced costs improve cash flow management and operational efficiency, allowing treasurers to gain a holistic, real-time view of global finances.

- Trade Finance: Integrating blockchain into trade finance processes can revolutionize how international trade is conducted. Smart contracts can automate the execution of letters of credit, guarantees, and supply chain financing, reducing paperwork, speeding up transactions, and increasing trust among trading partners. This can unlock billions in trapped capital and reduce the risk of fraud.

- Interbank Settlements: Financial institutions are exploring direct settlement of interbank obligations using DLT, reducing reliance on central clearing houses and traditional correspondent banking networks. This can lower systemic risk, improve liquidity management, and reduce the operational burden of reconciliation. Projects like Fnality and JPM Coin are prime examples of this trend.

- Stablecoins and Central Bank Digital Currencies (CBDCs): The emergence of stablecoins (cryptocurrencies pegged to fiat currencies) and the ongoing development of CBDCs by central banks worldwide are pivotal for blockchain-based cross-border payments. Stablecoins offer a digital representation of fiat currency on a blockchain, combining the stability of traditional money with the efficiency of crypto. CBDCs, issued and backed by central banks, could provide a highly secure and efficient infrastructure for both domestic and international payments, potentially bypassing commercial banks for certain transactions and offering greater control over monetary policy.

Chainlink’s Orchestrating Role in Advanced Blockchain Payments

While blockchains provide the foundational ledger, they often require external data and connectivity to fulfill the complex requirements of institutional-grade cross-border payments. This is where Chainlink, the industry-standard oracle platform, becomes indispensable. Chainlink provides the essential data, interoperability, compliance, and privacy standards needed to power advanced blockchain use cases for tokenized assets, including cross-border payments. These payments depend on accurate market data, verified collateral for stablecoins, and secure cross-chain messaging, all while remaining compliant with each jurisdiction’s existing regulatory requirements—capabilities uniquely enabled by Chainlink.

- Real-Time Price Data with Chainlink Data Feeds: Cross-border payments frequently involve currency conversions. Chainlink Data Feeds provide highly reliable, tamper-resistant market data for foreign exchange (FX) conversion, rate locking, and complex settlement logic. By aggregating data from numerous high-quality off-chain sources and delivering it on-chain in a decentralized manner, Chainlink ensures that payments are executed at accurate, real-time prices, minimizing slippage and ensuring fair value for all parties.

- Verifying Collateralization with Chainlink Proof of Reserve (PoR): The integrity of stablecoins and other tokenized assets used in cross-border payments is paramount. Chainlink Proof of Reserve provides smart contracts with the data needed to calculate the true collateralization of any on-chain asset backed by off-chain or cross-chain reserves. This ensures that assets used in payments are transparently and continuously backed by verifiable reserves, building trust and stability within the system.

- Secure Cross-Chain Messaging with Chainlink CCIP: The blockchain ecosystem is fragmented, with multiple public and private blockchains coexisting. For cross-border payments to truly thrive, seamless interoperability between these disparate networks is crucial. Chainlink CCIP (Cross-Chain Interoperability Protocol) acts as a secure "internet of blockchains," enabling cross-chain data and value transfers across any public or private blockchain. Applications can use CCIP to trigger token transfers or status updates to execute cross-border and cross-chain payments with the highest level of cross-chain security, ensuring atomic transfers of value and data without relying on trusted third parties.

- Unlocking Real-World Asset Utility with Chainlink SmartData: The tokenization of real-world assets (RWAs) is a growing trend, and Chainlink SmartData is a suite of on-chain data offerings designed to unlock the utility, accessibility, and reliability of these tokenized assets. In the context of cross-border payments, SmartData enables applications to enforce settlement limits, validate collateralization, and provide accurate asset valuations across various jurisdictions, ensuring that tokenized assets can be reliably used as payment instruments or collateral.

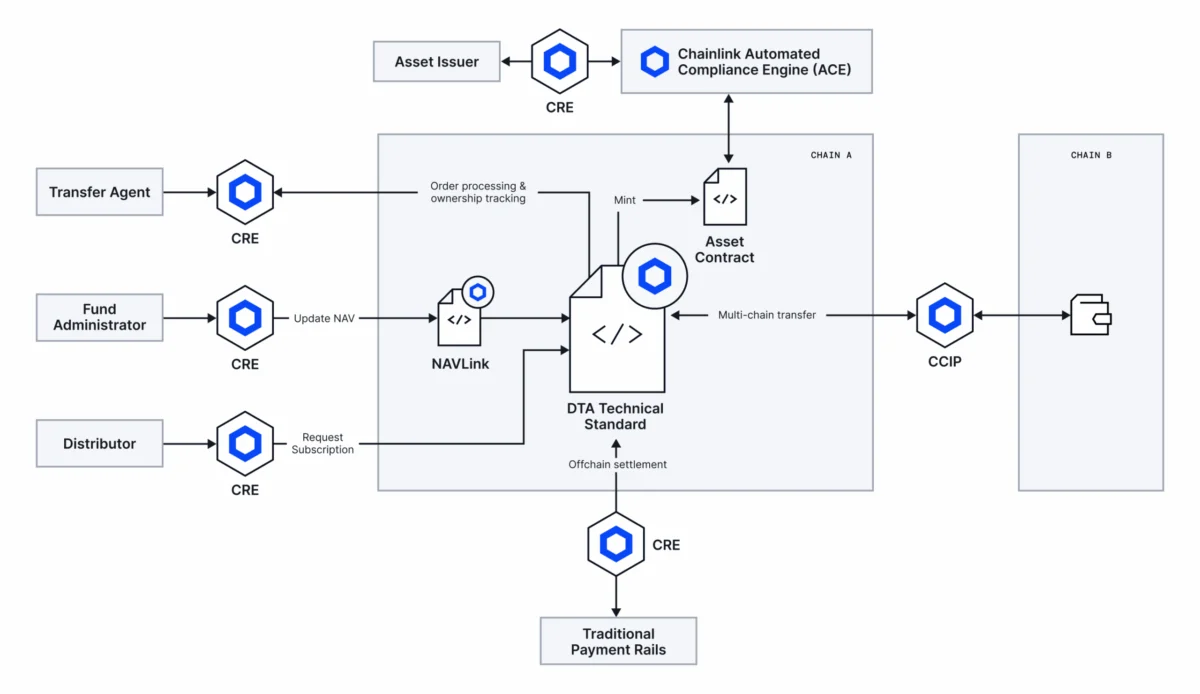

- Compliant Cross-Border Transactions with Chainlink ACE: Institutional adoption of blockchain for cross-border payments hinges on robust compliance. Chainlink’s Automated Compliance Engine (ACE) enables users to build, manage, and execute complex financial transactions across multiple jurisdictions, counterparties, digital assets, and environments, all in a compliance-focused and privacy-preserving manner. For cross-border payments, Chainlink ACE enforces jurisdiction-specific KYC/AML, sanctions screening, and other compliance policies directly on-chain by evaluating both identity and compliance data before a payment is executed, automating a previously manual and labor-intensive process.

- Orchestrating Cross-Border Payments Between Systems with Chainlink CRE: The Chainlink Runtime Environment (CRE) serves as an all-in-one orchestration layer, unlocking institutional-grade smart contracts for on-chain finance. CRE coordinates the full transaction lifecycle, including crucial steps such as compliance checks, FX data retrieval, settlement execution, and off-chain system reporting. In a single, secure execution environment, CRE connects various blockchain networks, integrates critical data, and interfaces with existing enterprise systems while automating compliance and privacy. This delivers fast, verifiable, and enterprise-grade cross-chain operations, allowing institutions to seamlessly integrate blockchain payments into their existing infrastructure. For instance, a payment application collects funds on Chain A, uses CCIP to send a token transfer to Chain B where the payment settles in a stablecoin, while Chainlink Data Feeds provide real-time FX rates, and Proof of Reserve verifies collateral backing—enabling fast, transparent payments with built-in verification and compliance.

- Enabling Privacy for Cross-Border Transactions with Confidential Compute: A major concern for institutions utilizing public blockchains is the exposure of proprietary or sensitive information. Chainlink addresses this through Confidential Compute, which allows sensitive logic and data to be processed off-chain in secure, trusted execution environments (TEEs) while only verifiable outcomes are recorded on-chain. As part of Chainlink’s privacy standard, this architecture enables private cross-border payments, selective disclosure for compliance purposes, and confidential cross-chain execution, allowing institutions to leverage the benefits of public blockchains for cross-border settlement without compromising sensitive financial data.

Industry Adoption and the Regulatory Landscape

The potential of blockchain in cross-border payments has not gone unnoticed by major financial players and regulatory bodies. Central banks worldwide are actively researching and piloting Central Bank Digital Currencies (CBDCs), often citing improved efficiency and reduced costs for cross-border payments as a primary motivation. Institutions like the Bank for International Settlements (BIS) have initiated projects like Project Dunbar and mBridge, exploring multi-CBDC platforms for international settlements.

Commercial banks and payment providers are also experimenting. Major financial institutions have formed consortia to explore DLT for interbank payments, and some have launched their own permissioned blockchain networks or digital currency initiatives (e.g., J.P. Morgan’s Onyx blockchain and JPM Coin). These initiatives underscore a growing consensus that DLT offers a viable path to modernize the global financial infrastructure.

However, the regulatory landscape remains complex and evolving. A lack of harmonized international regulations poses challenges for widespread adoption. Issues such as data privacy, consumer protection, and especially anti-money laundering (AML) and counter-terrorist financing (CTF) compliance, need robust and consistent frameworks across jurisdictions. Regulators are working to understand the unique characteristics of blockchain technology while ensuring financial stability and protecting consumers. The path forward will likely involve continued collaboration between innovators, financial institutions, and regulatory bodies to establish clear guidelines and standards that foster innovation while mitigating risks.

The Future of Cross-Border Payments Powered by Blockchain

Today’s global payment systems are slow, expensive, and opaque, often involving multiple intermediaries, high fees, and extended settlement times. Leveraging blockchains fundamentally transforms these transactions, making them faster, more transparent, and significantly more secure. As institutions and governments seek to further advance efficient and compliant financial infrastructure, blockchain-based cross-border payments are poised to play a key role in the next evolution of global finance.

The future will likely see a hybrid model where traditional financial systems increasingly integrate with blockchain networks. The focus will be on building interoperable ecosystems, enhancing scalability to handle massive transaction volumes, and improving user experience to ensure seamless adoption. Economic impacts could be profound, fostering greater global trade, enhancing financial inclusion, and potentially reshaping geopolitical financial dynamics. While challenges remain, including overcoming legacy infrastructure inertia, navigating regulatory hurdles, and ensuring robust cybersecurity, the trajectory toward a blockchain-powered future for cross-border payments is clear. Platforms like Chainlink, by bridging the gap between on-chain and off-chain worlds and providing critical infrastructure for data, interoperability, compliance, and privacy, are not merely facilitating this transition but actively orchestrating the realization of a truly interconnected, efficient, and equitable global financial system.