The global financial system, a colossal network of institutions, markets, and infrastructures, serves as the indispensable backbone of the world’s economy. It orchestrates the efficient allocation of capital, manages complex risks, and facilitates the seamless processing of trillions of dollars in daily transactions. From a German investor acquiring shares on NASDAQ to a tech giant issuing bonds for expansion, and even the simplest everyday purchase, this intricate ecosystem connects savers with investors, channels funds to their most productive uses, and employs sophisticated risk management tools to mitigate the impact of unforeseen market events. As of December 29, 2025, this system stands at a pivotal juncture, poised for a transformative shift driven by the integration of blockchain technology, smart contracts, and oracle networks, signaling a new era of efficiency and accessibility.

The Foundational Pillars: Institutions and Infrastructures Powering Global Finance

At its core, the global financial system is defined by a diverse array of specialized institutions and critical infrastructures, each playing a vital role in maintaining stability and facilitating economic activity. These entities ensure the flow of capital, manage risk, and process payments across borders and asset classes.

- Asset Managers: Firms like BlackRock and Vanguard offer investment products and services to a vast client base, including pension funds, corporations, and government entities. They conduct extensive investment research, construct and manage portfolios, facilitate trades, and implement sophisticated risk management strategies. BlackRock, for instance, manages trillions in assets, highlighting the scale of their influence on capital markets.

- Brokerage Firms: Companies such as Charles Schwab and UBS act as intermediaries, enabling clients to buy and sell securities. Beyond trade execution, they provide account management, investment advisory services, margin lending, and prime brokerage for institutional clients.

- Central Banks: The Federal Reserve and the European Central Bank exemplify these institutions, which oversee and regulate financial markets, control monetary policy, and safeguard financial stability. Their functions include currency issuance, acting as a lender of last resort, and managing foreign exchange reserves. Their policy decisions ripple through global markets, influencing everything from interest rates to inflation.

- Central Securities Depositories (CSDs): Entities like DTCC, Clearstream, and Euroclear are crucial for the safekeeping and management of securities on behalf of financial institutions. They maintain detailed ownership records, facilitate settlement processes, and manage corporate actions such as dividend distributions and stock splits. The DTCC alone processes trillions of dollars in securities transactions daily.

- Clearing Houses (CCPs): CME Clearing and LCH Group serve as critical intermediaries in securities transactions, significantly mitigating counterparty risk between buyers and sellers. They achieve this through novation (stepping in as buyer to every seller and vice-versa), setting margin requirements, maintaining default funds, and employing various risk management techniques.

- Commercial Banks: Global behemoths like JPMorgan Chase and Bank of America provide a wide range of banking services to individuals, businesses, and governments. Their services encompass deposits, loans, payments and transfers, wealth management, trade financing, and foreign exchange operations, forming the bedrock of everyday financial interactions.

- Credit Rating Agencies: Moody’s, S&P Global Ratings, and Fitch Ratings assess the creditworthiness of corporations, governments, and financial instruments, providing crucial indicators of default risk to investors. Their ratings influence investment decisions and the cost of capital for issuers worldwide.

- Custodian Banks: BNY Mellon and State Street safeguard financial assets for institutional investors, corporations, and high-net-worth individuals. They also manage transaction settlement, process corporate actions, handle tax reporting, and facilitate foreign exchange transactions. These banks often hold assets worth tens of trillions of dollars globally.

- Exchanges: The NYSE, NASDAQ, and London Stock Exchange are centralized platforms where buyers and sellers trade financial instruments like stocks and derivatives, ensuring price discovery and enforcing trading rules to maintain market integrity.

- Insurance Companies: MetLife, Prudential, and Allianz pool risk to protect policyholders against financial losses across various sectors. They engage in underwriting, premium collection, claims processing, and strategic investment of policyholder funds.

- Investment Banks: J.P. Morgan, Goldman Sachs, and Morgan Stanley provide specialized advisory and capital-raising services to corporations, governments, and institutions. This includes mergers & acquisitions advisory, underwriting new securities issuances, and market making and trading.

- Messaging Standards: Swift (utilizing ISO 20022) provides the standardized messaging formats that enable secure and efficient financial communication globally, facilitating cross-border transactions and ensuring data privacy. Swift processes millions of messages daily, underpinning global financial flows.

- Payment Processors: Mastercard and Visa enable digital and card-based transactions between consumers and businesses, providing transaction authorization, payment settlement, and crucial fraud prevention services. They form the backbone of modern retail commerce.

- Pension Funds: CalPERS and Universities Superannuation Scheme (USS) manage vast retirement funds, making strategic investments to ensure long-term returns for beneficiaries. Their investment decisions significantly influence global capital markets.

- Transfer Agents: Companies like Computershare maintain security ownership records, facilitate dividend distribution, and manage investor communications for publicly traded companies.

- Trade Repositories: CME Group and UnaVista collect and maintain records of over-the-counter (OTC) derivatives transactions, providing essential trade data to regulators for financial oversight and systemic risk monitoring.

While this overview covers key players, the financial ecosystem also includes family offices, fintech companies, hedge funds, market makers, microfinance institutions, mutual fund companies, neobanks, primary dealers, private equity firms, real estate investment trusts (REITs), sovereign wealth funds, and venture capital firms, all contributing to its multifaceted nature.

The Global Financial System In Action: Navigating Intricate Pathways

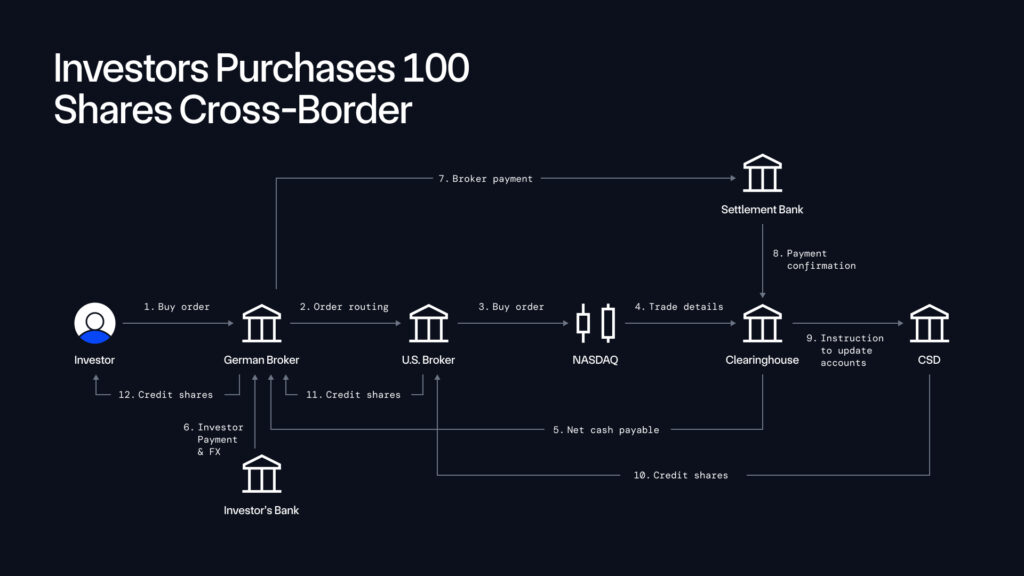

The current operational model of the global financial system, while robust, is characterized by its complexity, fragmentation, and reliance on numerous intermediaries. Consider a seemingly straightforward cross-border transaction, such as a German investor purchasing 100 shares listed on NASDAQ. This involves multiple steps across different jurisdictions and institutions: the investor’s local brokerage, a custodian bank, international payment systems, a US-based broker, the NASDAQ exchange, a US custodian, and a clearing house. Each step introduces potential delays, costs, and reconciliation challenges. Settlement, the final transfer of ownership and funds, often takes T+2 or T+3 days, meaning two or three business days after the trade date, tying up capital and introducing counterparty risk.

Similarly, a tech company issuing a bond to fund expansion requires a syndicate of investment banks, legal counsel, credit rating agencies, and a complex distribution network. The bond issuance and subsequent secondary market trading involve multiple ledgers, manual reconciliation processes, and a chain of custodians and transfer agents to manage ownership and coupon payments. These processes, while functional, are inherently inefficient, expensive, and opaque, built on decades of incremental technological advancements rather than a holistic digital design. The multiplicity of systems and the need for constant reconciliation across different ledgers contribute to operational friction and vulnerability to errors, highlighting the need for a more streamlined, real-time approach.

The Dawn of a New Era: Tomorrow’s Financial System Through Tokenization

The financial system of tomorrow will continue to fulfill its fundamental roles – allocating resources, managing risks, and processing payments – and will still be powered by many of today’s leading institutions. However, its underlying infrastructure is undergoing a profound transformation, moving towards an architecture built on blockchains, smart contracts, and oracle networks. This shift is heralded by the accelerating trend of tokenization, where real-world assets (RWAs) are represented as digital tokens on a blockchain.

BlackRock CEO Larry Fink has unequivocally identified tokenization as "the next generation for markets," a sentiment echoed by the industry, with a staggering 97% of asset managers agreeing that tokenization will revolutionize asset management. According to a collaborative report by Boston Consulting Group and ADDX, the market for tokenized assets is projected to reach an astounding $16 trillion by 2030, a testament to the technology’s disruptive potential. This growth is driven by a desire to overcome the inherent limitations of traditional finance, paving the way for a more efficient, transparent, and globally interconnected system.

The advantages of tokenization are multifaceted and compelling:

- Enhanced Accessibility: Tokenization lowers the barriers to entry for investors, enabling fractional ownership of high-value assets like real estate, art, or private equity. This democratizes investment opportunities, allowing a broader range of participants to access markets previously reserved for institutional or high-net-worth individuals.

- Increased Liquidity: By breaking down assets into smaller, more easily tradable units and facilitating peer-to-peer transactions on global blockchain networks, tokenization dramatically improves asset liquidity. This reduces transaction friction and expands trading hours beyond traditional market closures.

- Streamlined Processes and Automation: Smart contracts, self-executing agreements stored on a blockchain, can automate complex financial operations such as settlement, dividend distribution, and corporate actions. This drastically reduces manual intervention, minimizes operational errors, and accelerates transaction speeds from days to minutes or even seconds.

- Greater Transparency and Auditability: All tokenized asset transactions are recorded on an immutable, distributed ledger, providing an unparalleled level of transparency and auditability. This can help reduce fraud, improve regulatory compliance, and build greater trust in financial markets.

- Reduced Costs: Automation and the removal of multiple intermediaries can significantly lower transaction fees, administrative costs, and the overhead associated with managing traditional financial instruments.

- Improved Security: Blockchain’s cryptographic security features make tokenized assets highly resistant to tampering and fraud.

- Global Interoperability: Tokenized assets, by existing on interconnected blockchain networks, can move seamlessly across different platforms and jurisdictions, fostering a truly global and integrated financial market.

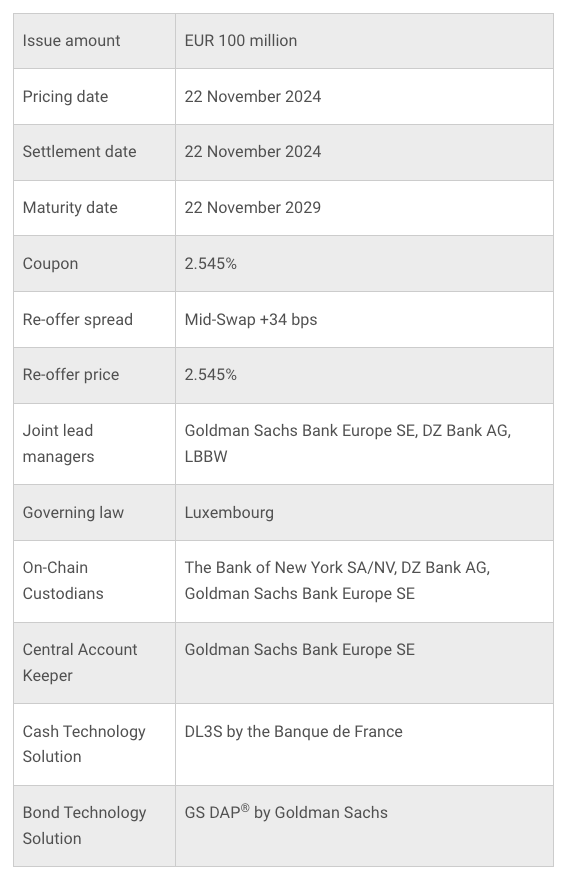

A significant real-world example highlighting this increasing digital asset adoption is the European Investment Bank (EIB)’s issuance of a EUR 100 million digital bond. In collaboration with Banque Centrale du Luxembourg, Banque de France, and Goldman Sachs, this tokenized bond was issued on Banque de France’s DLT platform, offering a coupon of 2.545% and maturing in 2029. This initiative demonstrates how leading financial institutions and central banks are actively exploring and implementing blockchain solutions for core financial products, validating the technology’s readiness for institutional adoption. It represents a crucial step towards understanding the operational, legal, and regulatory implications of a tokenized financial landscape.

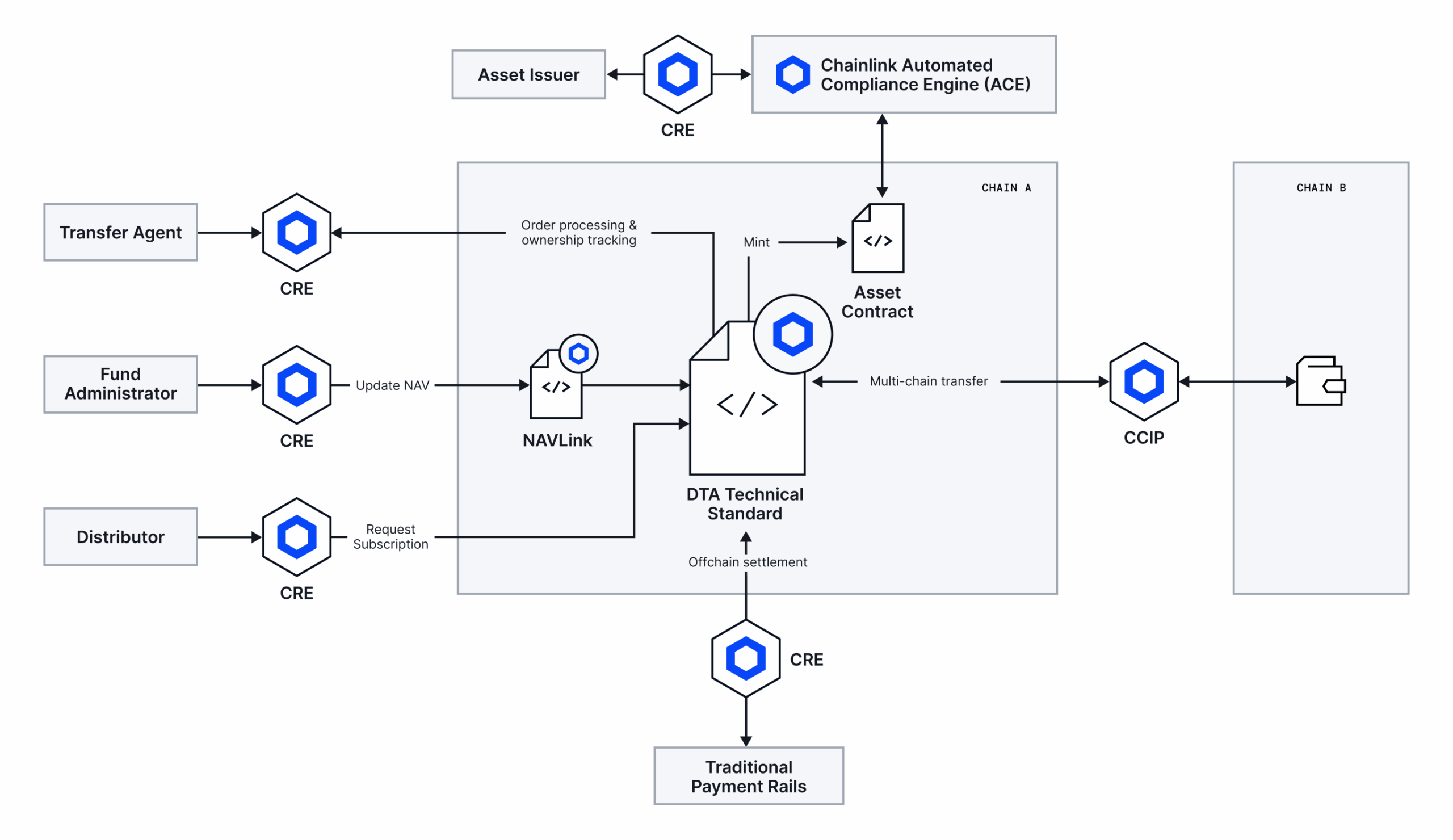

Pioneering the Future: Chainlink’s Role in Bringing the Global Financial System Onchain

Chainlink, as the industry-standard decentralized oracle network, is at the forefront of this transformation, acting as the critical bridge between traditional financial systems and the burgeoning world of blockchain. By providing secure, reliable, and tamper-proof real-world data and cross-chain communication capabilities, Chainlink is empowering next-generation applications across banking, asset management, and other major sectors. Its collaborations with established institutions and infrastructures like Swift, Fidelity International, and ANZ Bank underscore its pivotal role in building the financial system of tomorrow.

Next-Generation Tokenized Funds:

In a groundbreaking demonstration as part of the Monetary Authority of Singapore’s (MAS) Project Guardian initiative, SBI Digital Markets, UBS Asset Management, and Chainlink successfully automated fund subscriptions and redemptions using blockchains and smart contracts. This pilot showcased how Chainlink can coordinate operations between asset managers, fund distributors, and fund administrators across disparate blockchains and existing financial systems. By leveraging Chainlink’s infrastructure, the new model unlocks significant efficiency gains in fund management, reducing the manual overhead and complexity traditionally associated with fund administration and transfer agency processes. This sets a precedent for how tokenized funds can achieve greater operational fluidity and cost-effectiveness.

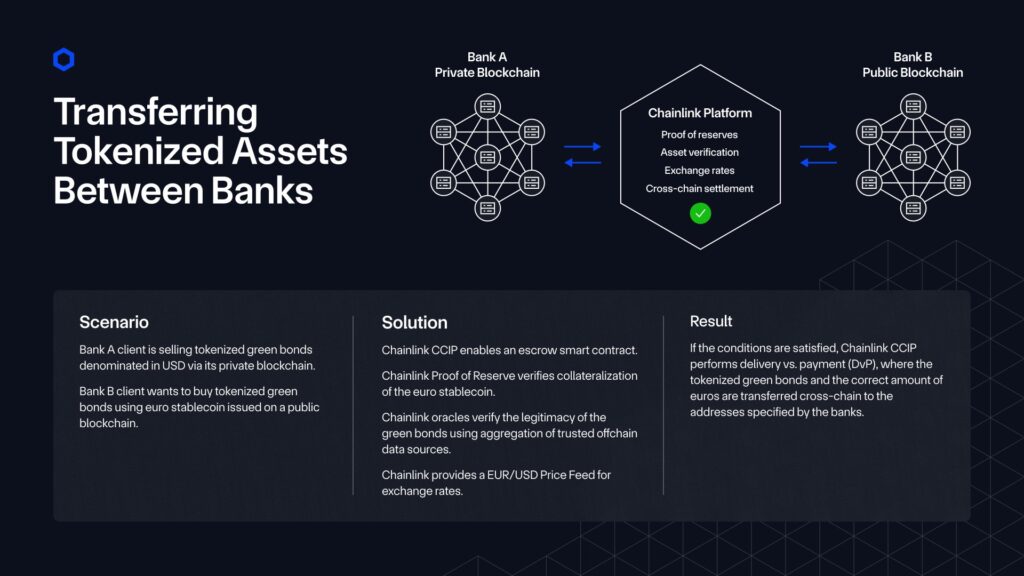

Transferring Tokenized Assets Cross-Chain:

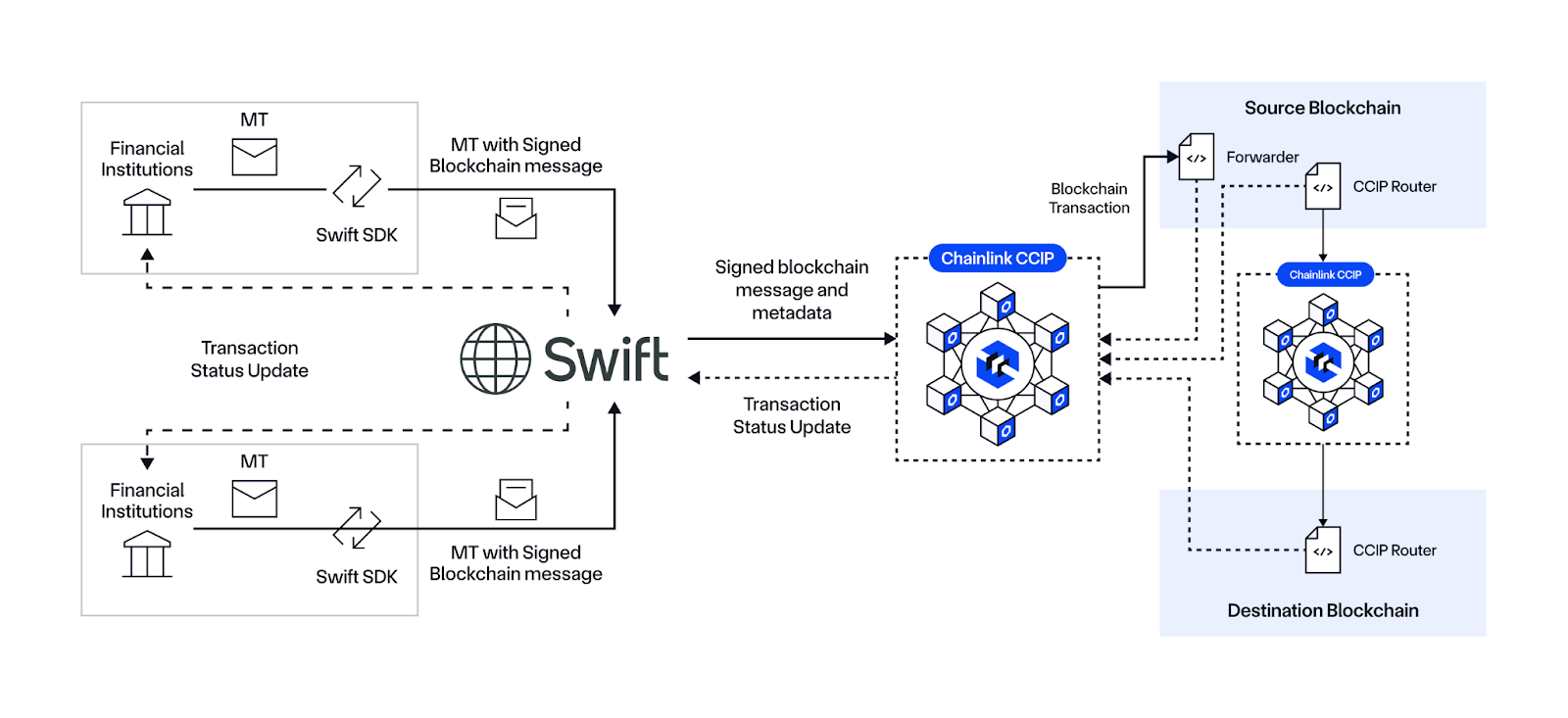

Recognizing the critical need for seamless interoperability, Swift, the international bank messaging standard serving over 11,000 banks, is actively working with Chainlink to unlock tokenization at scale. Their collaboration successfully demonstrated a secure and scalable method for transferring tokenized assets cross-chain using Chainlink’s Cross-Chain Interoperability Protocol (CCIP). This landmark initiative involved over 12 world-leading financial institutions, including Euroclear, Clearstream, ANZ, Citi, BNY Mellon, BNP Paribas, Lloyds Banking Group, and SDX. The success of this pilot proves that CCIP can serve as the universal standard for value and data transfer across both traditional financial systems and diverse blockchain networks, addressing one of the most significant challenges in the tokenization landscape: fragmentation. The implications are profound, enabling capital to flow freely and securely across a global network of tokenized assets.

Establishing a Unified Standard for Asset Servicing with the Chainlink Platform, Blockchains, and AI:

Chainlink, in collaboration with 24 of the world’s largest financial institutions and market infrastructures, including Swift, DTCC, Euroclear, UBS, and Wellington Management, has advanced its work on corporate actions processing. Building on initial foundations, the second phase introduced a production-grade system incorporating new data attestor and data contributor roles. These roles empower trusted institutions to validate and enrich corporate actions records extracted using Large Language Models (LLMs), achieving 100% data accuracy for confirmed records. This innovative solution establishes an "onchain golden record" for corporate actions – an attested, real-time source of truth accessible simultaneously by smart contracts, custodians, and post-trade systems. For tokenized equities, an increasingly adopted category of tokenized assets, this initiative enables them to reference the same confirmed records across both public and private blockchains, laying crucial groundwork for enhanced synchronization and increased automation across onchain markets. By standardizing the extraction, validation, and delivery of corporate actions data, this initiative creates a shared, reliable foundation for asset servicing across both blockchain networks and traditional financial infrastructure, significantly reducing reconciliation efforts and operational risks.

Privacy-Enabled, Cross-Chain, Cross-Border Tokenized Commercial Paper:

Under the Monetary Authority of Singapore (MAS) Project Guardian, ANZ Bank, ADDX, and Chainlink collaborated on a use case supporting the entire lifecycle of tokenized commercial paper. This project focused on expanding access to tokenized assets across borders while ensuring confidentiality requirements are met through Chainlink CCIP’s Private Transactions capability. This is crucial for institutional adoption, as financial institutions require robust privacy safeguards for sensitive transaction data. The successful demonstration of privacy-enabled cross-chain and cross-border connectivity for tokenized commercial paper marks a significant step towards building institutional-grade blockchain solutions that balance transparency with necessary data protection.

Europe’s First Tokenized Securities Trading and Settlement System:

21X is leveraging the Chainlink standard to enrich tokenized assets with high-quality data and enable cross-chain interoperability on Europe’s first EU-regulated financial market infrastructure (FMI). This pioneering system will provide integrated order matching, trading, settlement, and registry services for tokenized money and securities. The adoption of Chainlink’s standards by a regulated FMI is a strong indicator of the growing institutional confidence in blockchain technology and its potential to revolutionize capital markets within established regulatory frameworks.

CBDC Project for Trade Finance:

The Central Bank of Brazil (BCB) has selected a consortium comprising Banco Inter, Chainlink, Microsoft Brazil, and 7COMm to build a trade finance solution for the second phase of Brazil’s Drex CBDC project. This initiative leverages the Chainlink standard and blockchain technology to automate supply chain management and improve trade finance processes. By integrating real-world data and smart contract capabilities with a central bank digital currency, this project demonstrates the transformative potential of CBDCs for enhancing the efficiency, transparency, and accessibility of international trade finance, historically a complex and paper-intensive sector.

Implications and Future Outlook

2025 marks a pivotal moment for the global financial system, characterized by the convergence of traditional financial mechanisms with cutting-edge blockchain technologies. This fusion is not merely an incremental upgrade but a fundamental re-architecture, paving the way for a new era of financial products and services. The real-world adoption of tokenization, as evidenced by numerous institutional collaborations and projects, is already demonstrating a fundamental transformation in how capital markets operate.

The implications of this shift are far-reaching:

- Unprecedented Efficiency: Faster settlement times (near-instantaneous T+0), reduced operational costs due to automation, and streamlined workflows across the entire financial value chain.

- Enhanced Resilience: Distributed ledger technology offers inherent resilience against single points of failure, potentially making the financial system more robust.

- Greater Inclusivity: Fractional ownership and lower transaction costs can democratize access to investment opportunities for a broader global population, fostering financial inclusion.

- New Market Structures: The reduction of intermediaries could reshape the roles of traditional players and foster the emergence of new market participants and business models.

- Evolution of Regulation: Regulators worldwide are actively engaging with DLT, developing frameworks to ensure market integrity, consumer protection, and financial stability in the tokenized era. This dynamic regulatory landscape will be critical for the mainstream adoption of these technologies.

However, the transition is not without its challenges. Interoperability between various blockchain networks and legacy systems, scalability to handle global transaction volumes, robust cybersecurity measures, and clear, harmonized regulatory frameworks across jurisdictions remain key areas of focus. Chainlink’s role in addressing the interoperability challenge through CCIP and its focus on connecting existing institutions is vital for overcoming these hurdles.

Conclusion

The journey towards a fully onchain global financial system is underway, driven by the compelling benefits of tokenization and the innovative work of technologies like Chainlink. By enhancing accessibility, improving liquidity, reducing costs, and fostering cross-border connectivity, these innovations are poised to create financial systems that are not only more efficient and resilient but also more inclusive. As we move forward, the collaboration between traditional finance giants and blockchain innovators will continue to accelerate, reshaping the future of finance and unlocking unprecedented innovation in capital markets worldwide.

For deeper insights into this transformative period, interested parties are encouraged to explore Chainlink’s Definitive Guide to Tokenized Assets, featuring contributions from leading firms like BCG, 21Shares, Paxos, and Backed, and to watch Chainlink’s "Future Is On" series, which features discussions with leaders from Citi, Standard Chartered, Deutsche Bank, and other influential institutions. The future of finance is not just digital; it is decentralized, interconnected, and fundamentally onchain.