The global financial system, a labyrinthine network of institutions and infrastructures, forms the bedrock of the world’s economy, orchestrating the efficient allocation of resources, mitigating risks, and processing trillions in payments daily. As of December 29, 2025, this intricate system is undergoing an unprecedented transformation, driven by the emergence of blockchain technology and the widespread adoption of tokenization. This paradigm shift promises to deliver a more efficient, resilient, and inclusive financial landscape, with key innovations like Chainlink serving as critical infrastructure bridging traditional finance with decentralized networks.

The Foundation: Pillars of the Global Financial System

At its core, the global financial system connects savers with investors, facilitating capital flow through marketplaces where assets like stocks, bonds, and derivatives are bought and sold. This ecosystem relies on a diverse array of specialized entities, each playing a vital role:

- Asset Managers: Firms like BlackRock and Vanguard provide investment products and services, managing portfolios for pension funds, corporations, and government entities, employing rigorous investment research, portfolio construction, and risk management strategies.

- Brokerage Firms: Entities such as Charles Schwab and UBS execute trades for clients, offering advisory services, account management, and margin lending, acting as essential conduits to financial markets.

- Central Banks: The Federal Reserve and the European Central Bank oversee monetary policy, regulate financial stability, issue currency, and manage foreign exchange, serving as lenders of last resort to maintain systemic integrity.

- Central Securities Depositories (CSDs): Organizations like DTCC and Euroclear hold and manage securities, maintain ownership records, and facilitate settlement, acting as crucial post-trade infrastructure.

- Clearing Houses (CCPs): CME Clearing and LCH Group stand as intermediaries in securities transactions, significantly reducing counterparty risk through novation, margin requirements, and default funds.

- Commercial Banks: JPMorgan Chase and Bank of America offer comprehensive banking services, including deposits, loans, payments, wealth management, and trade financing, catering to individuals, businesses, and governments.

- Credit Rating Agencies: Moody’s, S&P Global Ratings, and Fitch Ratings assess the creditworthiness of various entities and financial instruments, providing essential indicators of default risk to investors.

- Custodian Banks: BNY Mellon and State Street safeguard financial assets for institutional investors, manage transaction settlement, process corporate actions, and handle tax reporting.

- Exchanges: NYSE, NASDAQ, and LSE provide centralized platforms for trading financial instruments, ensuring price discovery and enforcing market rules.

- Insurance Companies: MetLife and Allianz pool risk, underwrite policies, collect premiums, and process claims, investing substantial policyholder funds into the broader economy.

- Investment Banks: J.P. Morgan and Goldman Sachs offer advisory services for capital raising, mergers & acquisitions, underwriting new securities, and market making.

- Messaging Standards: Swift, leveraging ISO 20022, provides secure, standardized financial communication, enabling efficient cross-border transaction processing.

- Payment Processors: Mastercard and Visa facilitate digital and card-based transactions, handling authorization, settlement, and fraud prevention for everyday commerce.

- Pension Funds: CalPERS and Universities Superannuation Scheme manage retirement funds, making long-term investments to secure beneficiaries’ futures.

- Transfer Agents: Computershare maintains shareholder records, issues certificates, distributes dividends, and manages investor communications.

- Trade Repositories: CME Group and UnaVista collect and maintain records of OTC derivatives, providing vital data for regulatory oversight.

While this overview highlights the primary actors, the broader financial ecosystem also includes specialized entities like family offices, fintech companies, hedge funds, market makers, microfinance institutions, mutual fund companies, neobanks, primary dealers, private equity firms, real estate investment trusts (REITs), sovereign wealth funds, and venture capital firms, all contributing to the system’s vast complexity.

The Catalyst for Change: Addressing Systemic Inefficiencies

Despite its sophistication, the traditional global financial system grapples with inherent inefficiencies that impede its full potential. These challenges include:

- Fragmentation and Silos: The reliance on disparate, often legacy, systems across institutions and jurisdictions leads to data silos and complex reconciliation processes, increasing operational costs and risks.

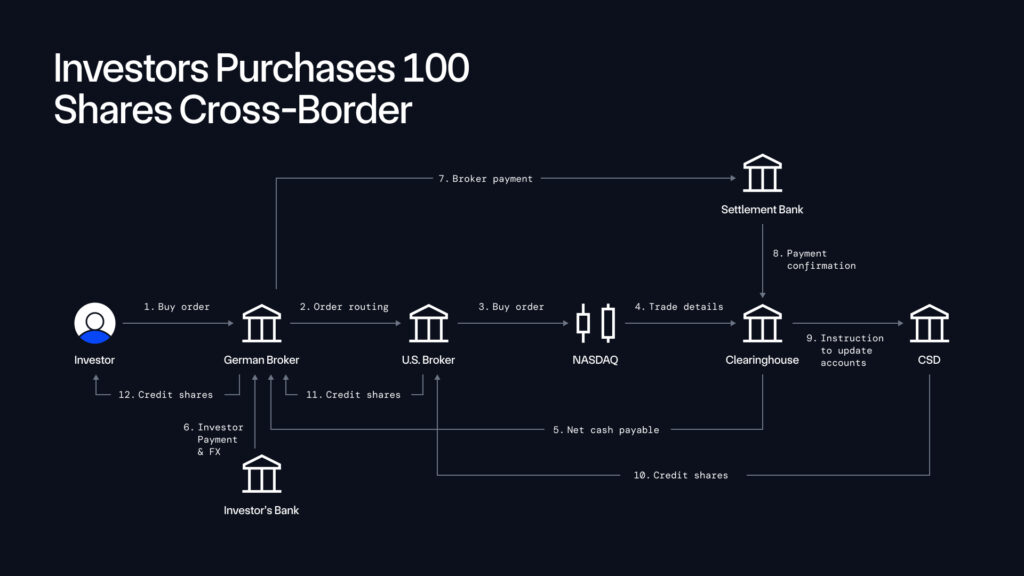

- Slow and Costly Settlement: Many securities transactions still operate on a T+2 or T+3 settlement cycle, meaning funds and assets are locked up for days, hindering capital efficiency. The numerous intermediaries involved in these processes also add significant costs.

- Limited Transparency: While regulated, certain aspects of the system, particularly in over-the-counter (OTC) markets, can lack real-time transparency, complicating risk management and regulatory oversight.

- Operational Complexity: Cross-border transactions, involving multiple currencies, legal frameworks, and settlement systems, are notoriously complex and prone to delays and errors.

- Accessibility Barriers: High minimum investment thresholds and geographical limitations often restrict access to certain financial products and markets, particularly for retail investors and emerging economies.

These challenges underscore the pressing need for innovation, a need that blockchain and tokenization are uniquely positioned to address.

The Dawn of a New Era: Tokenization and the Future of Finance

The financial system of tomorrow, while retaining the core functions of resource allocation, risk management, and payment processing, is increasingly envisioned to operate on blockchains, leveraging smart contracts and oracle networks. This transformation is encapsulated by tokenization, the process of representing real-world assets as digital tokens on a blockchain. Industry leaders, including BlackRock CEO Larry Fink, have lauded tokenization as "the next generation for markets," with an overwhelming 97% of asset managers agreeing that it will revolutionize asset management. Boston Consulting Group projects the market for tokenized assets to reach a staggering $16 trillion by 2030, signaling a profound shift.

The advantages offered by tokenization are manifold and directly tackle the inefficiencies of the traditional system:

- Enhanced Accessibility and Fractional Ownership: Tokenization democratizes access to illiquid assets like real estate, private equity, or art by enabling fractional ownership, lowering investment barriers and attracting a broader investor base.

- Increased Liquidity: By allowing for 24/7 trading on global platforms and reducing the friction of transfers, tokenization can significantly boost the liquidity of traditionally illiquid assets.

- Streamlined Processes and Automation: Smart contracts can automate various financial processes, from dividend distribution and interest payments to corporate actions and compliance checks, drastically reducing manual intervention and operational overhead.

- Reduced Costs: Fewer intermediaries and automated processes translate directly into lower transaction fees and administrative costs for both institutions and investors.

- Improved Transparency and Auditability: Blockchain’s immutable ledger provides a real-time, auditable record of all transactions and ownership, enhancing transparency and simplifying regulatory compliance.

- Faster Settlement (T+0): The ability to execute atomic swaps (simultaneous exchange of assets and funds) on a blockchain eliminates settlement delays, enabling near-instantaneous (T+0) settlement and freeing up locked capital.

- Interoperability: Standardized token formats and cross-chain solutions facilitate seamless transfer and interaction between different blockchain networks and even traditional systems.

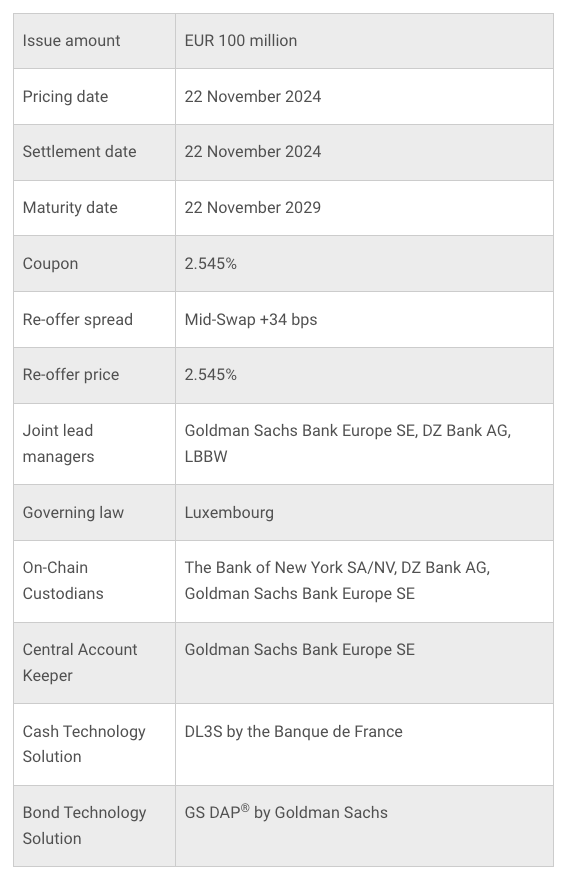

Concrete examples of this accelerating adoption are already emerging. The European Investment Bank (EIB) recently issued a EUR 100 million digital bond, a testament to the growing acceptance of DLT in sovereign-grade debt markets. This tokenized bond, issued on Banque de France’s DLT platform with a 2.545% coupon maturing in 2029, was a collaborative effort involving Banque Centrale du Luxembourg, Banque de France, and Goldman Sachs, demonstrating high-level institutional engagement in exploring blockchain for financial instruments.

Chainlink: A Key Architect of the Onchain Future

At the forefront of this financial revolution is Chainlink, a decentralized oracle network that serves as critical middleware, enabling smart contracts to securely interact with real-world data and traditional systems. Working collaboratively with established institutions and infrastructures like Swift, Fidelity International, and ANZ Bank, Chainlink is powering next-generation applications across banking, asset management, and capital markets.

1. Next-Generation Tokenized Funds:

Under the Monetary Authority of Singapore’s (MAS) Project Guardian initiative, SBI Digital Markets, UBS Asset Management, and Chainlink successfully demonstrated the automation of fund subscriptions and redemptions using blockchains and smart contracts. This innovative model leverages Chainlink to coordinate complex operations between asset managers, fund distributors, and fund administrators across disparate blockchains and existing financial systems. The pilot project showcased significant efficiency gains in fund management, reducing manual processes and enhancing the speed and accuracy of fund administration.

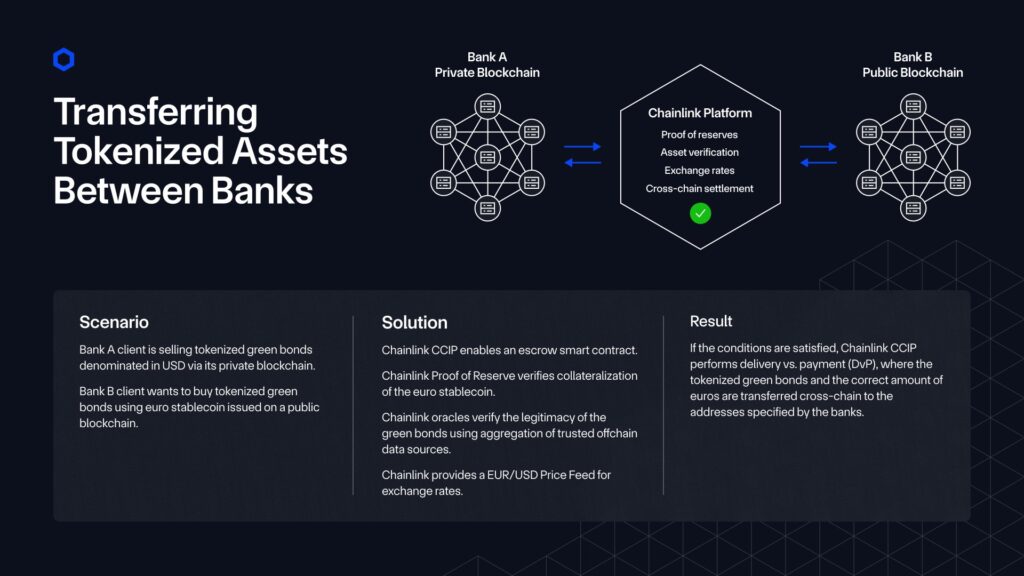

2. Transferring Tokenized Assets Cross-Chain:

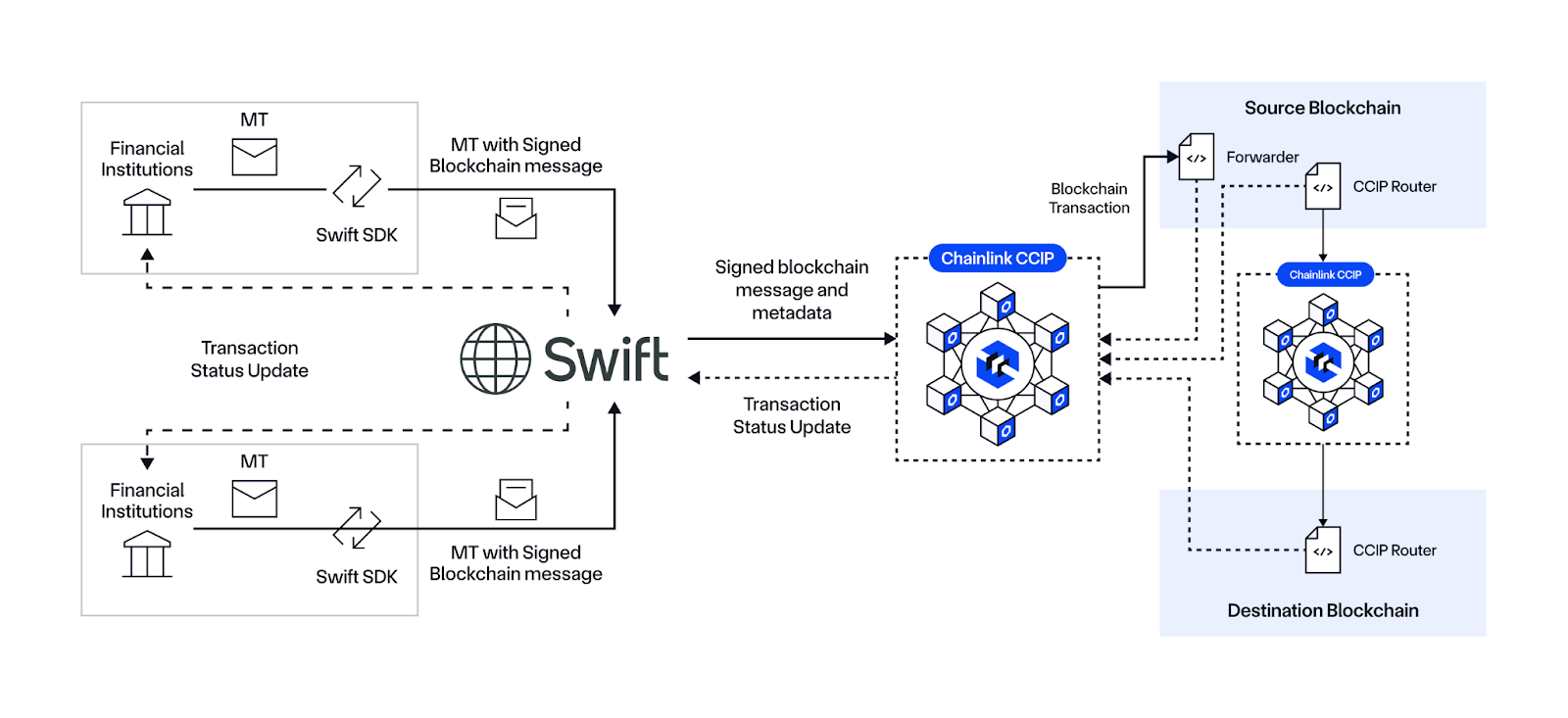

Swift, the international bank messaging standard connecting over 11,000 financial institutions globally, is actively collaborating with Chainlink to unlock tokenization at scale. Their joint efforts have successfully demonstrated a secure and scalable method for transferring tokenized assets cross-chain using Chainlink’s Cross-Chain Interoperability Protocol (CCIP). This groundbreaking collaboration involved more than 12 world-leading financial institutions, including Euroclear, Clearstream, ANZ, Citi, BNY Mellon, BNP Paribas, Lloyds Banking Group, and SDX. The success of this initiative provides a clear pathway for the seamless integration of existing financial infrastructure with blockchain networks, addressing a crucial interoperability challenge for enterprise-grade tokenization.

3. Establishing a Unified Standard for Asset Servicing with the Chainlink Platform, Blockchains, and AI:

Chainlink, in partnership with 24 of the world’s largest financial institutions and market infrastructures—including Swift, DTCC, Euroclear, UBS, and Wellington Management—has made significant strides in corporate actions processing. Building upon the foundations laid in Phase 1, the second phase introduced a production-grade system incorporating new data attestor and data contributor roles. These roles empower trusted institutions to validate and enrich corporate actions records extracted using Large Language Models (LLMs), achieving 100% data accuracy for confirmed records. This solution establishes an "onchain golden record" for corporate actions: an attested, real-time source of truth simultaneously accessible by smart contracts, custodians, and post-trade systems. This innovation enables tokenized equities, a rapidly growing category of tokenized assets, to reference the same confirmed records across both public and private blockchains, laying essential groundwork for enhanced synchronization and increased automation across onchain markets. By standardizing the extraction, validation, and delivery of corporate actions data, this initiative creates a shared foundation for asset servicing that spans both blockchain networks and traditional financial infrastructure.

4. Privacy-Enabled, Cross-Chain, Cross-Border Tokenized Commercial Paper:

Another significant development under MAS Project Guardian saw ANZ Bank, ADDX, and Chainlink collaborate on a use case supporting the entire lifecycle of tokenized commercial paper. This project addresses the critical need for privacy in institutional finance by expanding access to tokenized assets across borders while meeting confidentiality requirements. This was achieved using Chainlink CCIP’s Private Transactions capability, demonstrating how DLT can handle sensitive institutional data securely and privately, a prerequisite for broader adoption in capital markets.

5. Europe’s First Tokenized Securities Trading and Settlement System:

In Europe, 21X is leveraging the Chainlink standard to build the continent’s first EU-regulated financial market infrastructure (FMI) for tokenized securities. This system will provide order matching, trading, settlement, and registry services for tokenized money and securities. By adopting Chainlink, 21X ensures that its tokenized assets are enriched with high-quality data and benefit from cross-chain interoperability, marking a significant step towards regulated and interconnected tokenized markets in Europe.

6. CBDC Project for Trade Finance:

The Central Bank of Brazil (BCB) has selected a consortium comprising Banco Inter, Chainlink, Microsoft Brazil, and 7COMm to develop a trade finance solution for the second phase of Brazil’s Drex CBDC project. This initiative leverages the Chainlink standard and blockchain technology to automate supply chain management and improve trade finance processes. This project showcases a practical application of Central Bank Digital Currencies (CBDCs) and distributed ledger technology (DLT) in international trade, promising enhanced efficiency and transparency in a historically complex sector.

Broader Implications and Industry Outlook

The convergence of traditional financial systems with blockchain technologies marks a pivotal moment, poised to redefine capital markets and reshape the future of finance. The implications are far-reaching:

- Regulatory Evolution: The rapid pace of innovation necessitates agile regulatory frameworks. Central banks and financial authorities worldwide are actively exploring DLT, as evidenced by initiatives like Project Guardian and Brazil’s Drex. The challenge lies in harmonizing regulations across jurisdictions to facilitate global, interoperable tokenized markets.

- Economic Impact: Tokenization holds the potential to unlock new market opportunities, increase financial inclusion by lowering barriers to investment, and drive global economic growth through more efficient capital allocation.

- Technological Convergence: The integration of blockchain is not an isolated event. It is occurring alongside advancements in Artificial Intelligence (AI) and the Internet of Things (IoT), promising a future where these technologies collectively enhance automation, data analysis, and decision-making in finance.

- Challenges and Opportunities: While the benefits are clear, challenges remain, including scalability of blockchain networks, robust security measures, legal certainty for tokenized assets, and overcoming institutional inertia. However, the ongoing collaborations demonstrate a strong commitment from industry leaders to navigate these hurdles.

The real-world adoption of tokenization is no longer a distant vision; it is a current reality fundamentally transforming capital markets. By enhancing accessibility, improving liquidity, and fostering cross-border connectivity, these innovations are laying the groundwork for financial systems that are not only more efficient and resilient but also significantly more inclusive.

As 2025 draws to a close, the global financial system stands on the cusp of an era defined by unprecedented innovation. The symbiotic relationship between established financial institutions and groundbreaking blockchain infrastructure, exemplified by Chainlink’s pivotal role, is forging a new future. For those seeking deeper insights into this evolving landscape, Chainlink’s "Definitive Guide to Tokenized Assets," featuring contributions from BCG, 21Shares, Paxos, and Backed, and their "Future Is On" series, which includes perspectives from leaders at Citi, Standard Chartered, and Deutsche Bank, offer invaluable perspectives on this transformative journey.