The United States Securities and Exchange Commission (SEC) staff recently issued a significant clarification, confirming that registered broker-dealers are permitted to apply a 2% "haircut" to their stablecoin holdings for net capital calculation purposes. This nuanced guidance, provided last week, marks a crucial shift from previous uncertainties where broker-dealers largely operated under the assumption that a 100% haircut was necessary, effectively preventing them from counting dollar-pegged stablecoins toward their regulatory net capital requirements. The move is widely seen as a positive step towards integrating digital assets more seamlessly into traditional financial frameworks and fostering greater participation from regulated entities.

Understanding the Regulatory Haircut

In financial regulation, a "haircut" refers to the percentage reduction applied to the market value of an asset when it is used to calculate regulatory capital. This reduction reflects the potential for price volatility and liquidity risk associated with the asset. For example, a 2% haircut on a $100 million stablecoin holding means only $98 million can be counted towards a broker-dealer’s net capital requirements. The purpose of net capital rules, as mandated by the SEC, is to ensure that broker-dealers maintain sufficient liquid assets to meet financial obligations, absorb potential losses during market downturns, and protect investors. Historically, assets deemed higher risk or less liquid are subject to larger haircuts, sometimes up to 100%, which effectively renders them unusable for capital purposes.

Prior to this clarification, the ambiguity surrounding stablecoin treatment meant that many broker-dealers, out of an abundance of caution, applied a punitive 100% haircut. This effectively de-incentivized or even prohibited them from holding stablecoins, as doing so would negatively impact their capital ratios, potentially requiring them to hold significantly more reserves elsewhere to compensate. The lack of specific guidance from the SEC had created a regulatory grey area, hindering the broader adoption of stablecoins by regulated financial institutions.

The Official Stance and Key Endorsements

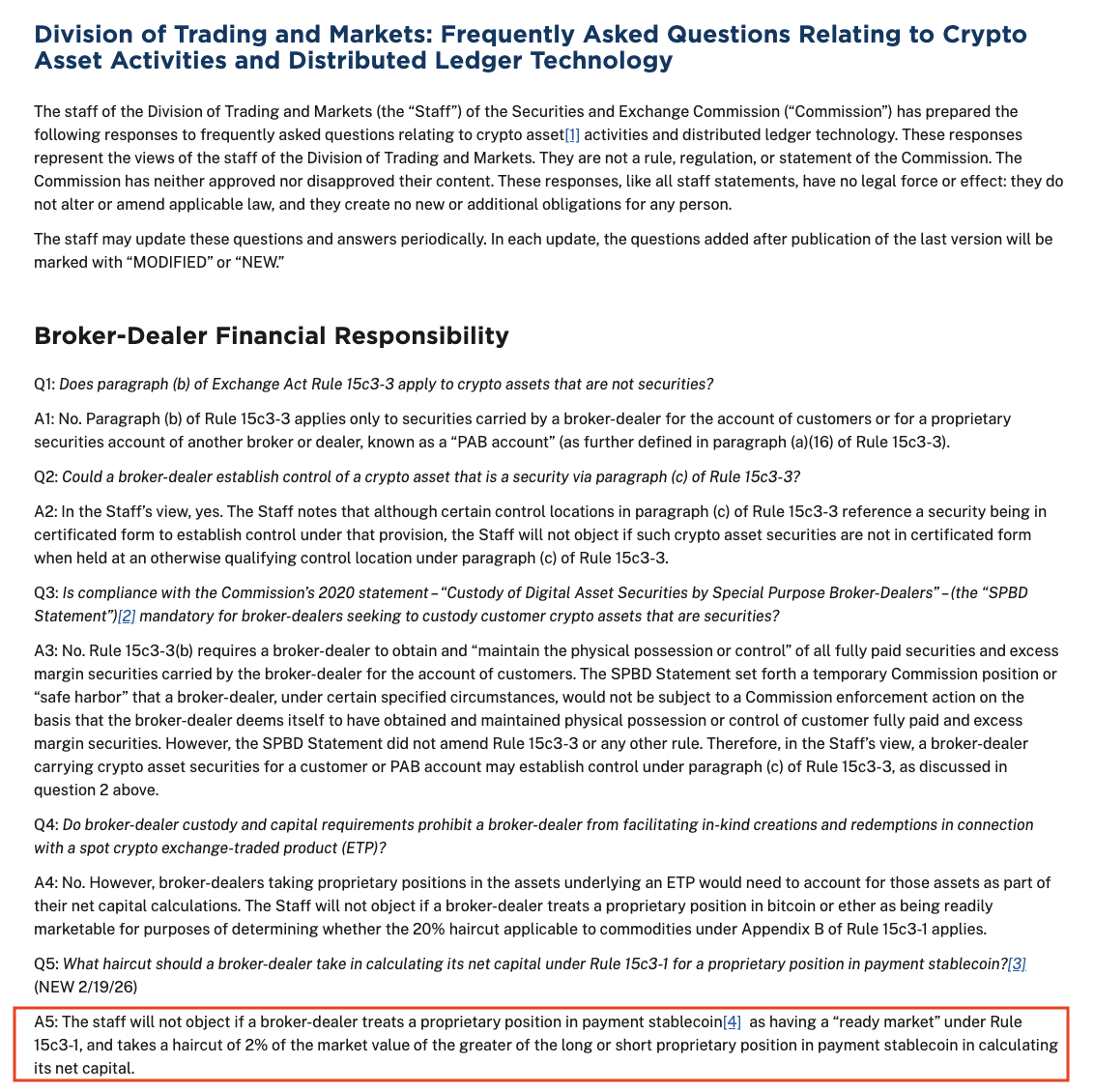

The clarification was formally published as an update to the staff of the SEC’s Division of Trading and Markets’ "Frequently Asked Questions Relating to Crypto Asset Activities and Distributed Ledger Technology." This document serves as a vital resource for market participants seeking to understand the SEC’s interpretive positions on emerging technologies and assets. While staff guidance does not carry the full weight of a formal rule, it provides crucial insight into the agency’s current thinking and approach, often serving as a de facto standard for compliance.

Following the release of this guidance, SEC Commissioner Hester Peirce, often referred to as "Crypto Mom" for her progressive stance on digital assets, voiced her strong approval. In a public statement, she articulated her long-held view: "In my view, a 100% haircut would be unnecessarily punitive given the underlying reserve assets that back payment stablecoins." Peirce further emphasized the practical benefits of this clarification, noting, "Stablecoins are essential to transacting on blockchain rails. Using stablecoins will make it feasible for broker-dealers to engage in a broader range of business activities relating to tokenized securities and other crypto assets." Her comments underscore the importance of stablecoins in facilitating efficient, blockchain-based transactions and highlight their potential to unlock new opportunities in the burgeoning field of tokenized finance.

The 2% haircut aligns stablecoins more closely with how traditional financial instruments, such as money market funds or short-term U.S. Treasurys, are treated for capital purposes. These low-risk cash equivalents typically incur minimal haircuts due to their high liquidity and stability. This parallel suggests that the SEC staff now views well-reserved stablecoins as possessing similar risk profiles to these conventional assets, a significant endorsement of their stability and reliability.

Implications for Broker-Dealers and Wall Street

For broker-dealers, the implications of this clarification are substantial. It provides regulatory certainty and capital efficiency, allowing them to hold stablecoins without incurring excessive capital charges. This newfound flexibility means they can integrate stablecoins into their operations, potentially using them for settlement, collateral management, or facilitating transactions in tokenized securities. The ability to count stablecoins toward net capital requirements frees up capital that would otherwise be tied up, enabling these firms to engage in a broader array of crypto-related activities.

Marc Baumann, CEO of crypto intelligence company 51, succinctly captured the industry’s sentiment in a social media post, describing the SEC staff communication as "a big deal." He elaborated, stating, "Wall Street can now actually hold and use stablecoins without destroying their capital ratios." This observation highlights the practical barrier that the 100% haircut previously posed and the significant relief that the 2% haircut offers to institutional players looking to enter or expand their presence in the digital asset space. The move is expected to enhance liquidity in the stablecoin market and facilitate deeper integration between traditional finance and decentralized finance (DeFi) ecosystems, particularly for tokenized real-world assets.

The Evolving Landscape of Stablecoins in the United States

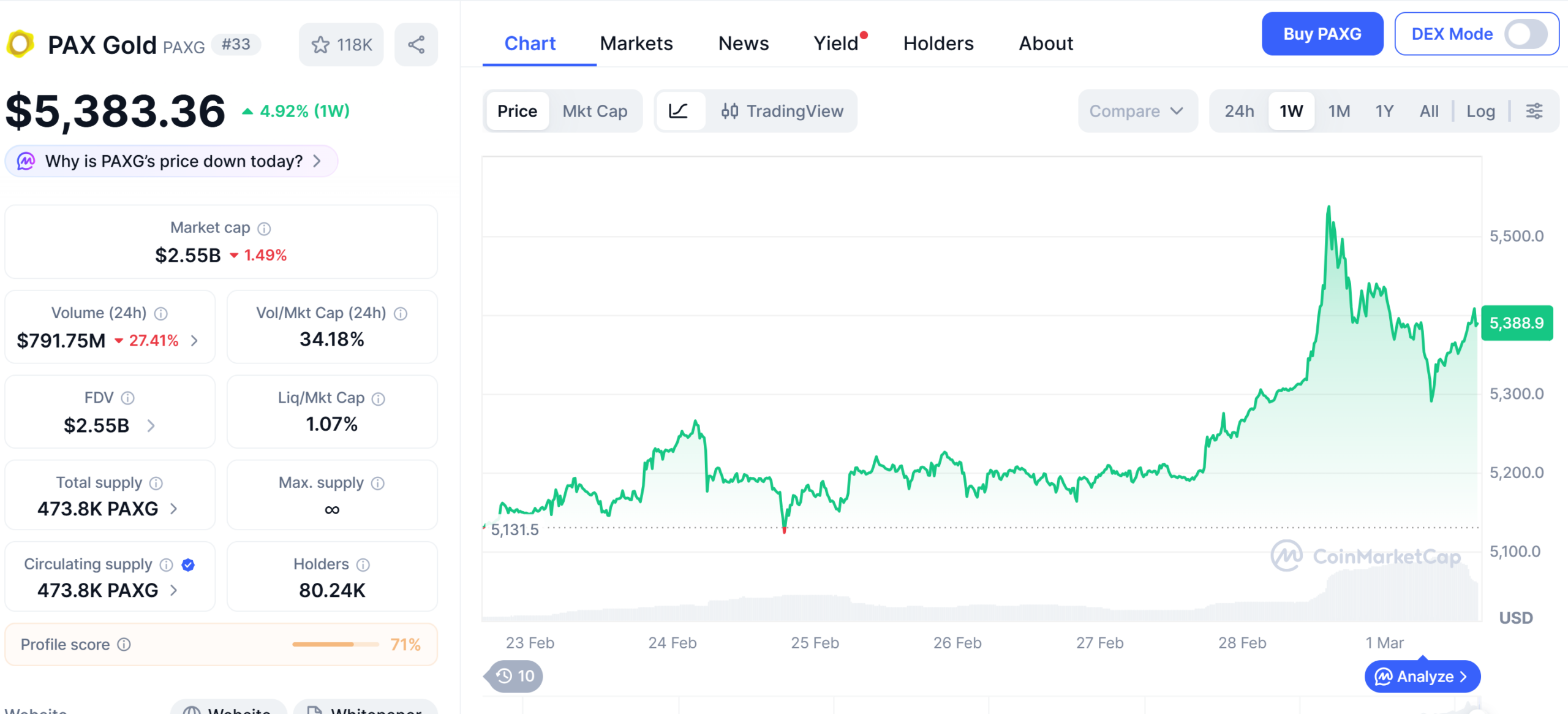

The SEC’s clarification comes at a time of increasing traction for stablecoins within the United States, despite ongoing debates about their regulatory classification and inherent risks. The stablecoin market capitalization, while experiencing a recent dip of approximately $6 billion from its December 2025 peak of over $300 billion, still boasts a robust $295 billion market cap. This figure represents steady growth since 2023, according to data from RWA.XYZ, signaling a resilient and expanding sector.

A significant legislative milestone occurred in July 2025 when then-President Donald Trump signed the GENIUS stablecoin bill into law. This landmark legislation was widely celebrated by the crypto industry as a crucial step towards establishing a comprehensive regulatory framework for stablecoins. At the time of its signing, the stablecoin market capitalization was just over $252 billion, and it subsequently surged following the bill’s passage, demonstrating the positive impact of regulatory clarity on market confidence and growth. The GENIUS bill aimed to address critical issues such as reserve requirements, redemption mechanisms, and consumer protection, laying a foundation for more secure and transparent stablecoin operations.

Despite these advancements and the evident growth in market capitalization, not all U.S. officials are convinced of stablecoins’ utility. Neel Kashkari, president of the Federal Reserve Bank of Minneapolis, remains a prominent skeptic, questioning the fundamental use cases for stablecoins and, by extension, much of the broader crypto market. In a recent statement, he remarked, "I could send any one of you $5 with Venmo, or PayPal, or Zelle, so what is it that this magical stablecoin can do?" Kashkari’s perspective reflects a segment of traditional finance and regulatory bodies that view existing payment rails as sufficient and question the added value of blockchain-based alternatives. His critique often centers on the perceived lack of unique functionality compared to established digital payment systems, overlooking potential benefits such as censorship resistance, programmability, and global accessibility that stablecoins offer, particularly for cross-border transactions and decentralized applications.

Broader Impact and Future Outlook

The SEC staff’s guidance on stablecoin haircuts is more than just a technical adjustment; it represents a subtle but significant shift in the regulatory approach to digital assets. By acknowledging stablecoins as legitimate assets that can contribute to a broker-dealer’s capital base, the SEC is signaling a willingness to adapt existing regulations to accommodate emerging technologies. This move could catalyze increased institutional adoption, not only by broker-dealers but potentially by other regulated financial entities observing this precedent.

The ability for broker-dealers to hold stablecoins efficiently opens doors for broader participation in tokenized securities markets. Tokenized securities, which are traditional assets represented on a blockchain, promise greater liquidity, fractional ownership, and more efficient settlement. Stablecoins, as the primary medium of exchange in these blockchain environments, are crucial for facilitating these transactions. Without the ability to hold stablecoins, broker-dealers would find it challenging to engage meaningfully with this nascent but rapidly growing sector. This clarification could therefore accelerate the development and adoption of tokenized assets across various financial markets, from real estate to private equity.

However, challenges remain. The current guidance is staff-level, meaning it could be subject to change or reinterpretation by future SEC administrations or through formal rulemaking. The broader regulatory landscape for crypto in the U.S. remains fragmented, with different agencies asserting jurisdiction and often providing conflicting signals. The push for comprehensive federal legislation, such as the GENIUS bill, reflects the ongoing effort to establish a unified and clear framework. Furthermore, the varying quality and transparency of stablecoin reserves continue to be a point of concern for regulators, necessitating robust audit and reporting standards to ensure their stability and investor protection.

In conclusion, the SEC staff’s decision to permit a 2% haircut for stablecoin holdings by broker-dealers is a pivotal moment for the integration of digital assets into mainstream finance. It addresses a critical regulatory ambiguity, enhances capital efficiency for regulated entities, and paves the way for greater institutional engagement with stablecoins and the broader tokenized economy. While skepticism from some officials persists, this clarification, alongside legislative efforts, underscores a growing recognition of stablecoins’ potential to modernize financial infrastructure and expand access to innovative financial products. The path ahead will likely involve further regulatory refinements, but this step unequivocally signals a more accommodating stance from a key U.S. financial regulator.