The closing of the first quarter of 2026 has marked a significant turning point for the digital asset market, as Bitcoin’s performance shifted from a narrative of institutional adoption to one dominated by global instability and tightening monetary conditions. As of the market close on March 31, 2026, Bitcoin was trading at approximately $66,280, representing a 24% decline since the start of the year. This downturn was not an isolated event within the crypto-currency ecosystem but rather a reflection of a broader retreat from risk assets that saw the S&P 500 post its weakest quarterly performance since 2022.

The quarter began with high expectations among investors that the "ETF era," characterized by sustained institutional inflows and corporate treasury accumulation, would provide a permanent floor for digital asset prices. However, by the end of March, the market was grappling with a reality defined by oil prices exceeding $100 per barrel, rising Treasury yields, and a localized conflict in the Middle East that has reshaped global trade and inflation expectations. The narrative of Bitcoin as a non-correlated "digital gold" faced a rigorous test, as the asset largely behaved like a high-beta macro trade, sensitive to liquidity shifts and geopolitical shocks.

A Chronology of Market Destabilization

The first three months of 2026 followed a trajectory of increasing complexity. In early January, the market remained optimistic, buoyed by the 2025 rally and the continued integration of spot Bitcoin ETFs into traditional brokerage accounts. However, the momentum began to stall in February as geopolitical tensions escalated into active military conflict involving the United States, Israel, and Iran. This shift forced an immediate reassessment of global risk.

By mid-February, the focus of the market shifted from internal crypto-native developments to the energy sector. Brent crude oil prices breached the $100 mark, driven by fears of supply chain disruptions in the Strait of Hormuz. This energy shock reignited inflation concerns, effectively ending the market’s hope for aggressive interest rate cuts by the Federal Reserve.

In March, the pressure intensified. The 10-year Treasury yield, a benchmark for global borrowing costs, climbed toward 4.50%. As traditional safe havens like the U.S. Dollar and short-term Treasuries gained favor, liquidity was drained from speculative sectors. Bitcoin, caught in this crossfire, saw its price fluctuate between $60,000 and $72,000, failing to establish a definitive upward trend despite several attempts to reclaim higher support levels.

The Impact of Geopolitical Conflict and Energy Shocks

The conflict in the Middle East has served as the primary catalyst for the quarter’s bearish tone. Analysts note that the war-driven energy shock did more than just increase the cost of fuel; it fundamentally altered the Federal Reserve’s policy path. At the start of the year, the consensus among economists was that the FOMC would begin a series of rate cuts by mid-2026. The surge in oil prices has made inflation "sticky," leading traders to price in the possibility of further rate hikes rather than cuts.

This shift in interest rate expectations has a direct correlation with Bitcoin’s valuation. When yields on "risk-free" assets like government bonds rise, the opportunity cost of holding non-yielding assets like Bitcoin increases. Furthermore, the volatility in the energy markets has had a secondary effect on the Bitcoin mining industry, where electricity costs are a primary operational concern. The combination of falling Bitcoin prices and rising energy costs has created a "double squeeze" on the sector, contributing to the selling pressure observed throughout the quarter.

Institutional Demand and the ETF Reversal

One of the most surprising developments of Q1 2026 was the exhaustion of the institutional "shock absorber" effect. In 2025, the launch of spot ETFs was credited with providing a steady stream of buy-side pressure that mitigated volatility. That trend reversed in early 2026. Data from SoSoValue indicates that Bitcoin ETFs saw net outflows exceeding $800 million for the quarter. While March saw a modest recovery with $1 billion in inflows, it was insufficient to offset the $1.8 billion lost in January and February.

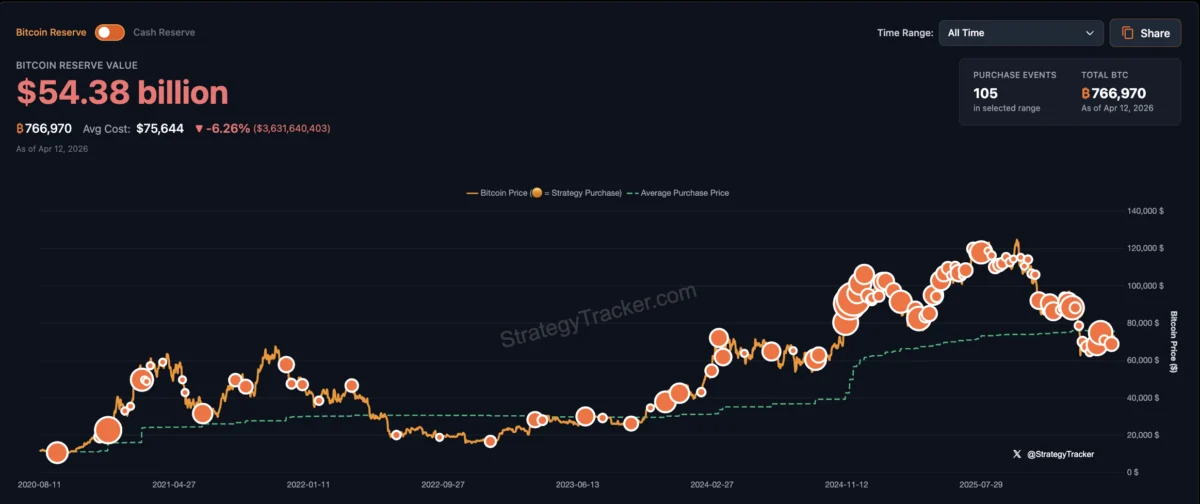

The institutional retreat extended to corporate treasuries. For much of the previous year, public companies adding Bitcoin to their balance sheets was a dominant market theme. In Q1 2026, this trend became increasingly concentrated. Strategy (formerly MicroStrategy) remained the sole aggressive buyer, acquiring 88,000 BTC during the quarter—one of its largest hauls to date. However, outside of this single entity, corporate interest appeared to wane.

A notable example of this cooling sentiment was the behavior of Nakamoto, a firm specifically built to hold Bitcoin. In March, the company sold 284 BTC for approximately $20 million, at an average price of $70,422. This sale was particularly significant because the firm had acquired the bulk of its holdings in 2025 at a weighted average price of $118,171. Selling at a substantial loss signaled a breakdown in the financing model that had previously rewarded companies for holding Bitcoin. As equity premiums for these "proxy" stocks vanished, companies were forced to de-risk to maintain liquidity.

Miner Sales and the Pivot to Artificial Intelligence

Bitcoin miners, traditionally the backbone of the network’s supply side, also contributed to the downward price pressure. According to research from VanEck, miners sold nearly 164,000 BTC over the past year, effectively liquidating all newly issued supply. This selling was not necessarily a sign of panic but a reflection of the rising cost of production, which reached an average of $79,995 per Bitcoin in late 2025.

Major industry players took significant steps to shore up their balance sheets:

- MARA Holdings: Sold 15,133 BTC in March, generating $1.1 billion to reduce debt and repurchase convertible notes.

- Core Scientific: Liquidated 1,900 BTC in January and announced plans to sell remaining holdings through the end of the quarter.

- Riot Platforms: Sold 1,818 BTC, valued at approximately $162 million.

Beyond simple liquidation, a structural shift is occurring within the mining sector. Many firms are redirecting capital away from Bitcoin hashing and toward Artificial Intelligence (AI) and High-Performance Computing (HPC) infrastructure. CoinShares reports that over $70 billion in cumulative AI and HPC contracts have been announced across the public mining sector. Companies such as TeraWulf and Hut 8 are increasingly being revalued by the market as data center operators, a move that reduces their reliance on Bitcoin’s price but also removes them as long-term "HODLers" of the asset.

On-Chain Data: Long-Term Holders and Realized Losses

On-chain metrics provide a deeper look into the psychology of the market during this downturn. The Spent Output Profit Ratio (SOPR) for long-term holders—those who have held Bitcoin for more than 155 days—dropped below 1 during the quarter. This indicates that even the most "diamond-handed" investors were beginning to realize losses.

Market analysts interpret this as a phase of "controlled de-risking." Unlike the chaotic capitulation seen in previous bear markets, the current selling appears methodical. Glassnode noted that while realized losses remained elevated through late March, there were no signs of the mass-panic liquidations that typically define a market bottom. Instead, older coins are being spent less frequently, suggesting that while some long-term holders are exiting, a core group remains committed to the asset despite the 24% YTD decline.

Derivatives and Technical Sentiment

The derivatives market reinforced the bearish outlook throughout the quarter. Perpetual funding rates remained consistently negative, a technical signal that short-sellers were dominant and willing to pay a premium to maintain their downside bets. Futures open interest stayed muted, suggesting that the leverage necessary for a "V-shaped" recovery was absent.

In the options market, the put-call open interest ratio hit 0.77 in mid-March, its highest level in nearly five years. Investors were aggressively purchasing "puts" (downside protection), indicating a lack of confidence in a near-term rally. The high cost of these protective contracts suggests that the market is bracing for further volatility, potentially driven by upcoming Federal Open Market Committee (FOMC) meetings or further escalations in the Middle East.

Broader Impact and Market Implications

The events of the first quarter of 2026 have forced a re-evaluation of Bitcoin’s role in a diversified portfolio. The expectation that Bitcoin would serve as a hedge against geopolitical instability has been challenged by its high correlation with other risk assets during periods of liquidity stress. While the long-term thesis of Bitcoin as a finite digital asset remains intact for many, the short-term reality is that it remains deeply tethered to global macro conditions.

For the remainder of 2026, the market’s trajectory will likely depend on three factors:

- Energy Prices: If oil remains above $100, the resulting inflation will keep interest rates high, limiting the "cheap money" that often flows into crypto.

- Institutional Persistence: Whether ETF flows can return to net positive territory will determine if there is enough organic demand to absorb ongoing miner and long-term holder sales.

- The AI Pivot: As miners transition into data center operations, the "pure play" Bitcoin investment landscape will change, potentially leading to lower network hashrate growth but more financially stable infrastructure companies.

As the second quarter begins, the market remains in a state of "defensive equilibrium." The heavy selling pressure of February and March has abated, but the aggressive, conviction-led buying required for a new bull cycle has yet to materialize. Investors are left watching the headlines from Washington and the Middle East as closely as they watch the blockchain, acknowledging that for now, Bitcoin’s fate is inextricably linked to the broader global reset.