A groundbreaking report from Keyrock, a prominent crypto investment firm and market maker, suggests a fundamental re-evaluation of the forces driving Bitcoin’s (BTC) price. The research indicates that newly created money does not uniformly impact risk assets, with the specific channel of liquidity injection playing a crucial role. Contrary to the widely held belief that the Federal Reserve’s balance sheet or other central bank policies are the primary determinants, Keyrock’s analysis points to US Treasury bill issuance as the dominant liquidity metric influencing Bitcoin’s valuation.

Understanding the New Thesis: Fiscal vs. Monetary Liquidity

The core of Keyrock’s findings revolves around the distinction between liquidity generated through fiscal policy (government spending financed by debt) and monetary policy (central bank actions like interest rate adjustments or quantitative easing/tightening). For years, market participants, particularly in the cryptocurrency space, have meticulously tracked the Federal Reserve’s balance sheet expansions and contractions, along with its interest rate decisions, assuming these directly correlated with the availability of capital for risk assets like Bitcoin. The narrative often posited that "money printing" by central banks inflated asset prices.

Keyrock’s researcher, Amir Hajian, challenges this conventional wisdom, asserting that "not all liquidity impacts risk asset prices equally." The report posits that when the US Treasury increases its issuance of Treasury bills (short-term debt instruments), it is essentially financing government spending. This spending directly injects fresh capital into the real economy – through salaries, infrastructure projects, welfare programs, and other expenditures. This newly circulated money, rather than merely sitting in bank reserves, eventually finds its way into various asset classes, including risk assets such as Bitcoin. The report succinctly states: "When the Treasury ramps up Treasury bill issuance, it is financing spending that flows into the real economy, and eventually into risk assets like Bitcoin. When Treasury bill issuance falls or turns negative, that fiscal tailwind fades."

This mechanism highlights a critical difference. While central bank quantitative easing (QE) involves the central bank purchasing government bonds from commercial banks, which primarily increases bank reserves, Treasury bill issuance directly funds government outlays that flow into the broader economy. This distinction suggests that fiscal policy, particularly debt-financed government spending, might have a more direct and potent impact on the "broad money supply" accessible to individual investors and corporations, which then seeks returns in various markets.

The Evident Correlation: Data and Lead Times

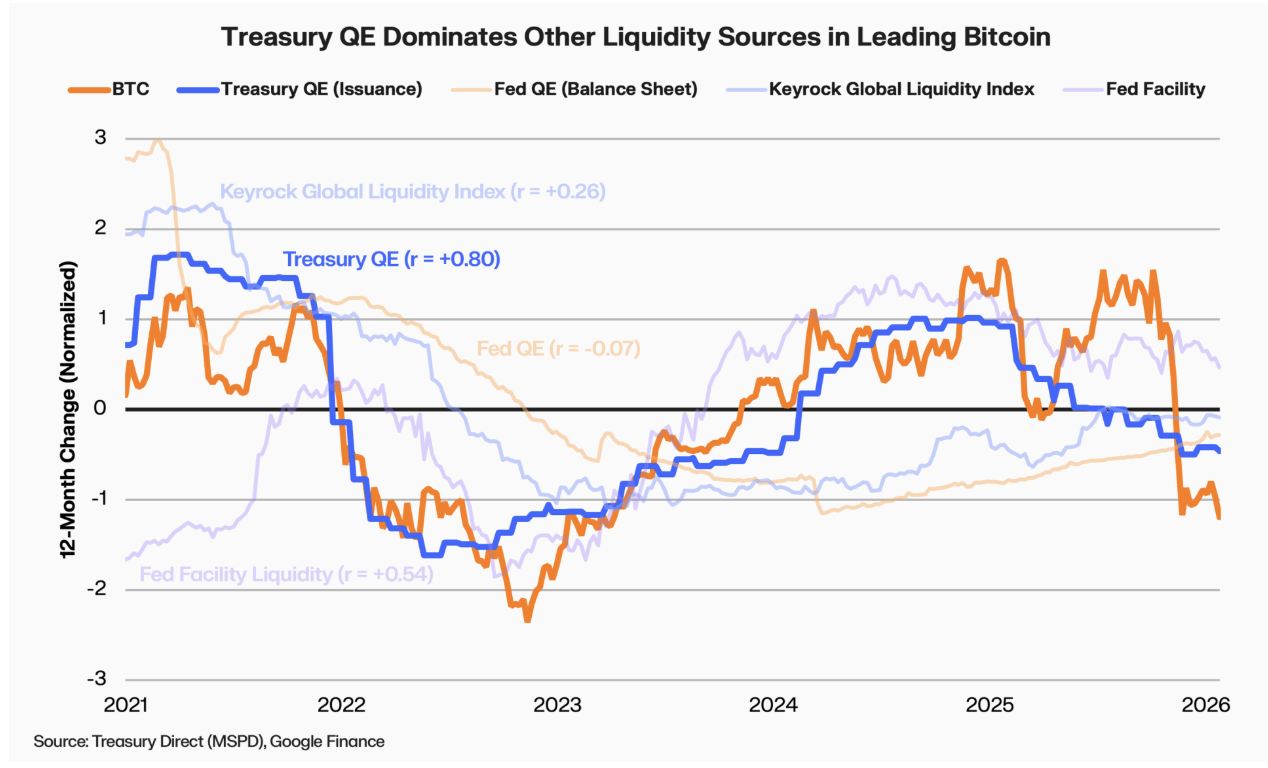

The research provides compelling statistical evidence to support its thesis. Since 2021, Treasury bill issuance has exhibited approximately an 80% correlation with Bitcoin’s price movements. This is a remarkably high correlation, especially for a market often perceived as highly volatile and susceptible to a myriad of factors. What makes this correlation even more significant is its predictive power: Treasury bill issuance leads Bitcoin prices by about eight months. This leading indicator status offers a potentially invaluable tool for investors attempting to anticipate future movements in the world’s largest cryptocurrency.

To quantify the broader impact of liquidity, Keyrock’s report details that every 1% change in global liquidity levels translates to a 7.6% impact on Bitcoin’s price in the subsequent business quarter. This sensitivity underscores Bitcoin’s role as a significant risk asset, highly responsive to the overall availability of capital in the global financial system. However, the nuance introduced by Keyrock is that where this liquidity originates matters profoundly. The accompanying charts within Keyrock’s original report visually underscore this point, illustrating the stronger statistical relationship between rising net Treasury bill issuance and Bitcoin returns compared to other methods of liquidity expansion. Historically, rising net treasury bill issuance has exhibited a leading statistical relationship with Bitcoin returns, reinforcing the firm’s central argument.

The period starting from 2021 is particularly relevant. This era followed unprecedented global fiscal and monetary stimulus in response to the COVID-19 pandemic. While central banks engaged in massive quantitative easing, governments also unleashed enormous fiscal packages, injecting trillions into economies worldwide. Keyrock’s research suggests that the fiscal component, channeled through Treasury bill issuance to fund these packages, may have been the more direct driver of asset inflation, including Bitcoin’s meteoric rise during this period.

Challenging the Prevailing Narrative: The Fed’s Role Re-evaluated

For many years, the Federal Reserve’s actions, particularly its interest rate policy and the expansion or contraction of its balance sheet, have been considered the paramount drivers of liquidity and risk asset prices. When the Fed engaged in Quantitative Easing (QE), buying vast amounts of government bonds and mortgage-backed securities, it was widely believed that this injected liquidity into the financial system, encouraging investment in riskier assets. Conversely, Quantitative Tightening (QT), where the Fed reduces its balance sheet, or interest rate hikes were seen as withdrawing liquidity and dampening speculative activity.

Keyrock’s analysis directly contradicts this widespread theory. While the Fed’s actions undeniably influence borrowing costs and financial conditions, the report implies that their direct impact on the flow of money into risk assets like Bitcoin might be secondary to the liquidity generated by the Treasury’s fiscal activities. The Fed’s influence might be more pronounced on the interbank lending market, bank profitability, and the cost of capital for corporations, rather than the immediate availability of "spendable" money that could chase higher returns in volatile markets.

This distinction is crucial for investors. If the primary driver is fiscal policy rather than monetary policy, then monitoring Treasury issuance schedules, government spending forecasts, and national debt maturities becomes more pertinent than obsessing over every Fed meeting minute or interest rate projection. While the Fed’s interest rate decisions still influence the broader economic environment and the attractiveness of different asset classes, Keyrock suggests they are not the primary direct source of the liquidity that fuels risk assets in the same way that debt-financed government spending is.

The Institutionalization Effect: Dampening Volatility

Despite the strong correlation between Treasury bill issuance and Bitcoin’s price, Keyrock’s report also highlights an interesting counter-trend: the increasing institutionalization of Bitcoin has somewhat dampened its sensitivity to liquidity conditions. The analysis suggests that the involvement of institutions and the advent of exchange-traded funds (ETFs) have reduced Bitcoin’s sensitivity to these liquidity fluctuations by approximately 23%.

The launch of spot Bitcoin ETFs in various jurisdictions, particularly in the United States in January 2024, marked a significant milestone in Bitcoin’s journey toward mainstream acceptance. These ETFs provide regulated, accessible avenues for institutional investors, wealth managers, and even retail investors to gain exposure to Bitcoin without directly holding the asset. The influx of institutional capital brings with it a different market dynamic. Institutional investors often have longer investment horizons, more sophisticated risk management strategies, and deeper pockets. Their demand is generally less reactive to short-term macroeconomic shifts compared to the more speculative, retail-driven flows that characterized earlier phases of the crypto market.

This institutional presence contributes to a more mature and stable market structure. While Bitcoin remains a volatile asset, the deeper liquidity provided by institutional players, the increased professionalization of trading desks, and the more robust infrastructure surrounding crypto markets can absorb some of the shocks from liquidity shifts. Instead of sharp, exaggerated movements in response to changes in available capital, institutional participation might lead to a more gradual and less dramatic price discovery process, making the asset less prone to extreme fluctuations, even as underlying liquidity drivers remain potent.

A Glimpse into the Future: Debt Maturity and Liquidity Influx

Keyrock’s report also offers a forward-looking perspective, identifying a critical "inflection point" in global liquidity dynamics. A substantial portion of the colossal $38 trillion US national debt is set to mature over the next four years. This presents a significant challenge for the US Treasury, as much of this debt was originally financed during periods of near-zero interest rates. Now, with interest rates significantly higher, the Treasury will be compelled to refinance this debt at considerably greater costs.

To manage this immense refinancing task, the US Treasury is highly likely to ramp up its issuance of Treasury bills. This necessity stems from the government’s ongoing need to fund its expenditures and roll over existing debt. Keyrock forecasts a substantial increase in T-bill issuance, projecting it to reach and sustain between $600 billion and $800 billion per year through 2028.

This projected surge in T-bill issuance has profound implications for Bitcoin’s future price trajectory. If Keyrock’s thesis holds true, this consistent and substantial injection of fiscal liquidity into the real economy, facilitated by increased Treasury bill issuance, is expected to serve as a significant tailwind for risk assets. The report specifically forecasts that this impending wave of global liquidity will impact Bitcoin prices most notably in late 2026 and early 2027. This timeline aligns with the 8-month lead time identified in the correlation data, suggesting that the increased issuance now and in the coming years will manifest in Bitcoin’s price action toward the latter half of the decade. The cyclical nature of T-bill issuance, as illustrated in Keyrock’s projections for 2021-2028, clearly shows this anticipated ramp-up, suggesting a sustained period of fiscal-driven liquidity expansion.

Broader Implications for Investors, Policymakers, and Market Structure

Keyrock’s research, if widely accepted, could instigate a significant paradigm shift in how market participants analyze and predict asset prices, particularly for volatile assets like Bitcoin.

For Bitcoin Investors: The implications are direct and actionable. Instead of solely fixating on the Federal Reserve’s rhetoric, interest rate forecasts, or balance sheet maneuvers, investors might need to broaden their analytical framework to include the US Treasury’s debt issuance schedule and government spending forecasts. This introduces a new, potentially more reliable, macro indicator for anticipating Bitcoin’s performance. It suggests a move from a purely monetary policy-centric view to one that equally weighs the impact of fiscal policy.

For Traditional Finance and Economists: The findings could spark a renewed debate on the precise mechanisms through which different forms of liquidity impact asset markets. It challenges the conventional understanding of the efficacy and reach of central bank monetary policy versus the more direct effects of government fiscal policy. It underscores the complex interplay between these two pillars of economic management and their respective influences on capital allocation. If fiscal flows are indeed more potent in driving risk assets, it could lead to a re-evaluation of financial models and macroeconomic forecasting tools.

For Policymakers: The research highlights a potential feedback loop where the exigencies of government debt management (refinancing at higher rates, leading to increased T-bill issuance) could inadvertently fuel asset price inflation, including in speculative assets. This might complicate the objectives of central banks attempting to manage inflation through monetary tightening, as fiscal liquidity could counteract some of those efforts. It emphasizes the need for coordinated fiscal and monetary policies to achieve desired economic outcomes without unintended consequences for asset markets.

For Market Structure and Algorithms: Algorithmic trading firms and institutional funds that rely on sophisticated quantitative models will likely incorporate these new liquidity metrics into their strategies. The 8-month lead time, in particular, offers a substantial window for strategic positioning, potentially influencing how large blocks of capital are allocated within digital asset portfolios. This could further entrench Bitcoin within the broader macro-economic analysis framework, solidifying its position as an asset responsive to global capital flows, albeit through a newly identified channel.

The confluence of growing national debt, higher interest rates, and the imperative for the US Treasury to refinance vast sums creates a unique environment for the coming years. Keyrock’s report suggests that this necessity will inadvertently create a significant tailwind for risk assets, including Bitcoin, primarily through the mechanism of increased Treasury bill issuance. This perspective offers a compelling alternative to traditional analyses and underscores the dynamic and evolving nature of global financial markets and the forces that shape them. As the world grapples with unprecedented levels of public debt and the complexities of managing modern economies, understanding the true drivers of liquidity and their impact on emerging asset classes like Bitcoin becomes increasingly critical for all market participants.