The Hong Kong Monetary Authority (HKMA) has taken a monumental step in solidifying its position as a leading global financial technology hub, announcing on Friday the issuance of its inaugural stablecoin issuer licenses. This landmark decision sees two financial powerhouses, HSBC and Anchorpoint Financial – a strategic joint venture comprising Standard Chartered, Animoca Brands, and Hong Kong Telecommunications (HKT) – become the first entities authorized to issue stablecoins pegged to the Hong Kong dollar (HKD). This pivotal development, stemming from a rigorous selection process that saw 36 applicants vie for the coveted licenses, marks a critical juncture for the city’s digital asset ecosystem and sets a new precedent for the integration of traditional finance with the burgeoning digital economy.

The significance of these awards cannot be overstated, particularly given the historical context. HSBC and Standard Chartered are not merely prominent commercial banks; they are two of only three institutions, alongside Bank of China (Hong Kong), entrusted with the authority to issue physical Hong Kong dollar banknotes, a privilege they have held since 1846. This deeply entrenched role in the city’s monetary system now extends into the digital realm, underscoring the HKMA’s strategic intent to bridge the chasm between conventional finance and the innovative, yet often volatile, world of digital assets. Darryl Chan, Deputy Chief Executive of the HKMA, articulated this vision, stating, "The two applicants have experience in traditional finance and risk management, which fits the mission of stablecoins that aim to bridge traditional finance and digital finance." This sentiment encapsulates the cautious yet progressive approach Hong Kong is adopting, prioritizing stability and consumer protection while fostering innovation.

A Robust Regulatory Framework: The Stablecoins Ordinance

The issuance of these licenses is underpinned by Hong Kong’s comprehensive Stablecoins Ordinance, a meticulously crafted regulatory framework that officially takes effect in August 2025. The HKMA’s proactive approach in granting licenses well in advance of the ordinance’s full implementation highlights its commitment to fostering a secure and well-regulated environment for stablecoin operations. The development of this ordinance did not occur in a vacuum; it is the culmination of years of research, public consultations, and a keen observation of global trends and challenges within the digital asset space.

Hong Kong began seriously exploring regulatory frameworks for virtual assets following an initial discussion paper released by the HKMA in January 2022, which specifically sought public feedback on the regulatory approach for stablecoins. This was part of a broader strategy to develop a holistic regulatory regime for virtual assets, recognizing their potential to transform financial services while also acknowledging inherent risks. The collapse of major crypto entities like FTX in late 2022, and the de-pegging of algorithmic stablecoins such as TerraUSD (UST), served as stark reminders of the imperative for robust regulatory oversight. These events reinforced the HKMA’s resolve to prioritize investor protection, market integrity, and financial stability.

The Stablecoins Ordinance imposes a series of stringent requirements on issuers, designed to mitigate risks and instill confidence in the digital currency. Key provisions include:

- Full Backing by High-Quality Liquid Assets: Stablecoins must be fully backed, at all times, by highly liquid assets. This means reserves must consist of cash, bank deposits, or short-term government securities, ensuring that each stablecoin can be redeemed at par value. This contrasts sharply with some earlier stablecoin models that relied on riskier or less liquid assets, or even algorithmic mechanisms, which proved susceptible to market volatility and bank runs.

- Capital Requirements: Issuers are mandated to maintain at least HK$25 million in paid-up capital. Furthermore, they must hold liquid capital equivalent to 12 months of anticipated operating expenses, providing a substantial buffer against operational disruptions and ensuring long-term viability.

- Redemption at Par: Holders must be able to redeem their stablecoins at par value (1:1) within one business day. This guarantee is fundamental to maintaining the stablecoin’s peg and ensures liquidity and trust.

- Prohibition on Interest/Yield: To prevent stablecoins from being perceived or marketed as investment products and to mitigate risks associated with lending or rehypothecation of reserves, issuers are explicitly prohibited from offering interest or yield on stablecoin holdings. This measure aims to keep stablecoins focused on their primary utility as a medium of exchange and store of value, rather than a speculative investment.

- Ban on Algorithmic Stablecoins: Learning directly from past failures, the regime explicitly bars algorithmic stablecoins, which rely on complex software and market incentives rather than tangible asset backing to maintain their peg. This ensures that only asset-backed stablecoins, proven to be more resilient, can operate under Hong Kong’s regulatory umbrella.

Financial Secretary Paul Chan had previously indicated in his February budget address that the initial batch of licenses would be limited, with regulators placing paramount importance on risk management, the quality of reserves, and robust anti-money laundering (AML) and counter-terrorist financing (CTF) controls. This measured approach underscores Hong Kong’s commitment to a safe and sustainable development of its virtual asset sector.

The Pioneers: HSBC and Anchorpoint Financial

The selection of HSBC and Anchorpoint Financial as the inaugural licensees speaks volumes about the HKMA’s strategy. Both entities bring unique strengths to the table, aligning perfectly with the regulatory body’s dual goals of innovation and stability.

HSBC: A Retail-Focused Digital Leap

HSBC, one of the world’s largest banking and financial services organizations, boasts an extensive retail customer base and a strong digital banking infrastructure. The bank has declared its intention to make its HKD stablecoin accessible to retail customers through its popular PayMe app and the HSBC HK Mobile Banking platform in the second half of 2026. This move is significant as it promises direct, mainstream access to a regulated stablecoin for everyday transactions, potentially transforming how Hong Kong residents engage with digital currencies.

HSBC has been actively exploring blockchain technology for several years, participating in various distributed ledger technology (DLT) initiatives, including digital bond issuances and cross-border payment experiments. Their foray into stablecoins represents a natural progression, leveraging their existing trust, regulatory compliance expertise, and vast customer network to drive adoption. By integrating the stablecoin into widely used platforms like PayMe, HSBC aims to provide a seamless and secure digital payment experience, potentially paving the way for broader acceptance of digital HKD in the retail sector.

Anchorpoint Financial: A Collaborative Enterprise Vision

Anchorpoint Financial, the other successful applicant, is a consortium that epitomizes the bridging of traditional finance with the nascent Web3 ecosystem. The joint venture comprises:

- Standard Chartered: Another global banking giant with a strong footprint in Asia, Standard Chartered has been a proactive player in the digital asset space, having established digital asset custody services (Zodia Custody) and institutional trading platforms (Zodia Markets). Their participation brings extensive financial expertise, regulatory acumen, and a deep understanding of institutional and corporate client needs.

- Animoca Brands: A prominent Hong Kong-based blockchain gaming and metaverse company, Animoca Brands provides invaluable Web3 native expertise, understanding of digital ownership, and connections within the burgeoning decentralized ecosystem. Their involvement highlights the HKMA’s willingness to incorporate innovative, digitally native perspectives into the regulated framework, fostering a true convergence of TradFi and DeFi.

- Hong Kong Telecommunications (HKT): As Hong Kong’s premier telecommunications service provider, HKT brings an expansive network, direct access to millions of consumers and businesses, and experience in integrating digital services into daily life. Their participation suggests a vision for widespread distribution and integration of the stablecoin into various digital services and payment solutions, potentially across different sectors.

Anchorpoint Financial plans to distribute its HKD stablecoin through selected business partners, indicating an initial focus on enterprise solutions, B2B payments, and potentially facilitating transactions within specific digital ecosystems or supply chains. The diverse composition of the Anchorpoint consortium suggests a strategic intent to explore a wide array of use cases, from institutional settlements to metaverse transactions, while maintaining the highest standards of regulatory compliance.

Broader Market Implications and Hong Kong’s Global Aspirations

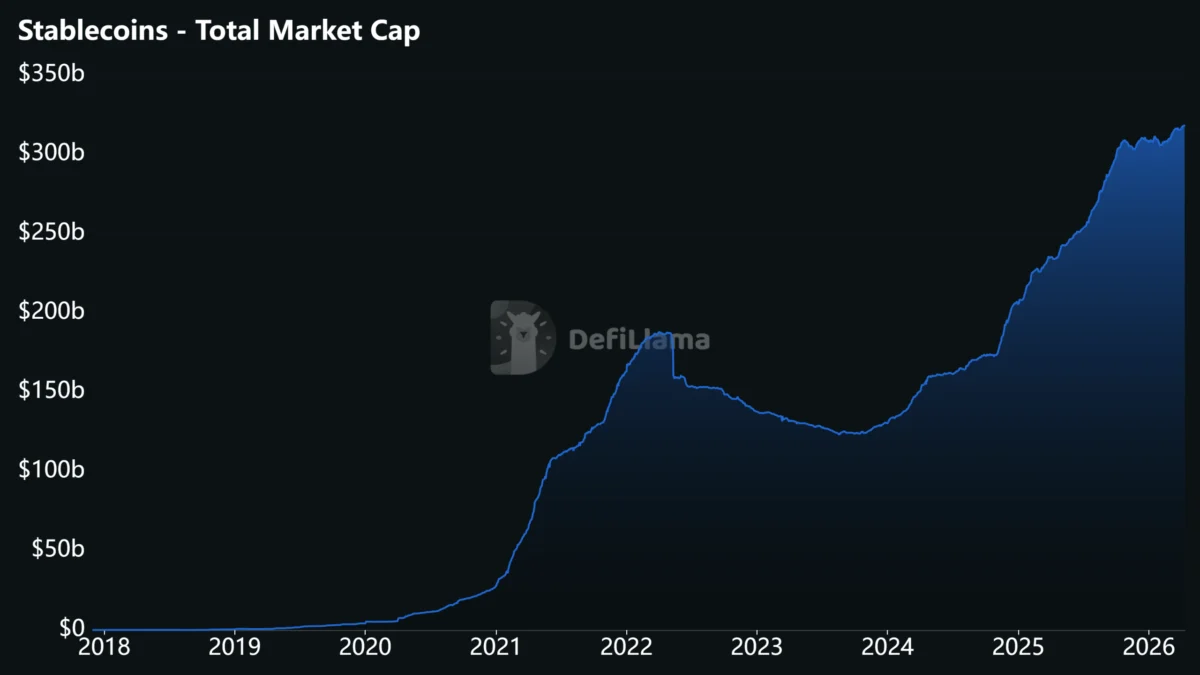

The stablecoin market globally has surged past $311 billion, though it remains overwhelmingly dominated by USD-denominated tokens such as Tether (USDT) and USD Coin (USDC). Hong Kong’s bold move to introduce regulated, bank-issued HKD stablecoins represents a calculated bet to carve out a significant niche, particularly in regional trade settlement and cross-border payments.

Facilitating Regional Trade and Payments:

Hong Kong has long served as a vital financial gateway to mainland China and a key hub for regional trade. Regulated HKD stablecoins could significantly enhance the efficiency of cross-border transactions within Asia, offering faster settlement times, lower costs, and increased transparency compared to traditional correspondent banking systems. Businesses engaged in trade across the Greater Bay Area and other Asian economies could leverage HKD stablecoins for instantaneous payments and settlements, reducing foreign exchange risks and operational overheads. This could solidify Hong Kong’s role as a nexus for digital trade finance.

Retail Adoption and Financial Inclusion:

While Hong Kong has a highly banked population, the integration of stablecoins into retail payment apps like PayMe could accelerate digital payments and potentially offer new avenues for financial inclusion in other markets where these technologies are adopted. The ease of use, instant settlement, and regulatory certainty offered by these licensed stablecoins could make them an attractive alternative or complement to existing digital payment methods.

The China Dimension: RMB Stablecoins and Internationalization:

Perhaps one of the most intriguing implications of Hong Kong’s stablecoin initiative lies in its potential role concerning mainland China. There have been reports and ongoing discussions about mainland China exploring the possibility of renminbi-backed stablecoins, potentially leveraging Hong Kong as a testing ground or a regulated channel. Furthermore, state-owned enterprises, such as the China National Petroleum Corporation (CNPC), have already initiated feasibility studies on using stablecoins for cross-border payments.

Hong Kong’s unique "One Country, Two Systems" framework positions it as an ideal sandbox and bridge for such experiments. A regulated HKD stablecoin ecosystem could provide a controlled environment for testing digital RMB initiatives, facilitating cross-border trade and investment flows between mainland China and international markets in a secure and compliant manner. This could contribute to the gradual internationalization of the RMB, albeit through a carefully managed digital pathway. The establishment of robust stablecoin regulations in Hong Kong provides a template and a trusted infrastructure that could be adapted for future digital RMB projects, allowing China to explore digital currency innovations without fully opening its capital account.

Competition and Future Outlook:

This strategic move positions Hong Kong competitively against other global financial centers like Singapore, Dubai, and London, all vying to become leaders in the digital asset space. While Singapore has also made strides in regulating digital payments and stablecoins, Hong Kong’s decision to license major incumbent banks for HKD-pegged stablecoins, coupled with its unique relationship with mainland China, provides a distinct advantage.

The HKMA’s decision is not an endpoint but rather a significant milestone in an ongoing journey. It is anticipated that more licenses may be issued in the future, as the market evolves and more use cases emerge. The focus will likely shift towards interoperability between different stablecoin networks, the development of innovative applications built on these stablecoins, and the continuous monitoring of market developments to ensure the regulatory framework remains agile and effective.

In conclusion, Hong Kong’s award of its first stablecoin issuer licenses to HSBC and Anchorpoint Financial represents a bold and meticulously planned foray into the future of digital finance. By entrusting its two most historically significant banknote issuers with the task of digitizing the HKD in a regulated environment, Hong Kong is not merely embracing innovation; it is orchestrating a profound convergence of traditional financial stability with the transformative potential of digital assets. This initiative not only strengthens Hong Kong’s standing as a global financial hub but also lays crucial groundwork for new paradigms in retail payments, cross-border trade, and potentially, the strategic internationalization of the renminbi through a secure digital corridor. The financial world will be watching closely as these pioneering stablecoins begin to circulate, charting a new course for digital currency adoption and regulation in one of Asia’s most dynamic economies.