The Resurgence of On-Chain Momentum

A comprehensive analysis of on-chain metrics reveals a tightening correlation between token utility and market sentiment. The primary driver behind the current optimistic outlook is the momentum of DeFi token transfers. By utilizing the 30-day Simple Moving Average (30D-SMA) and comparing it against the 365-day Simple Moving Average (365D-SMA), analysts can distinguish between short-term market noise and sustainable long-term trends.

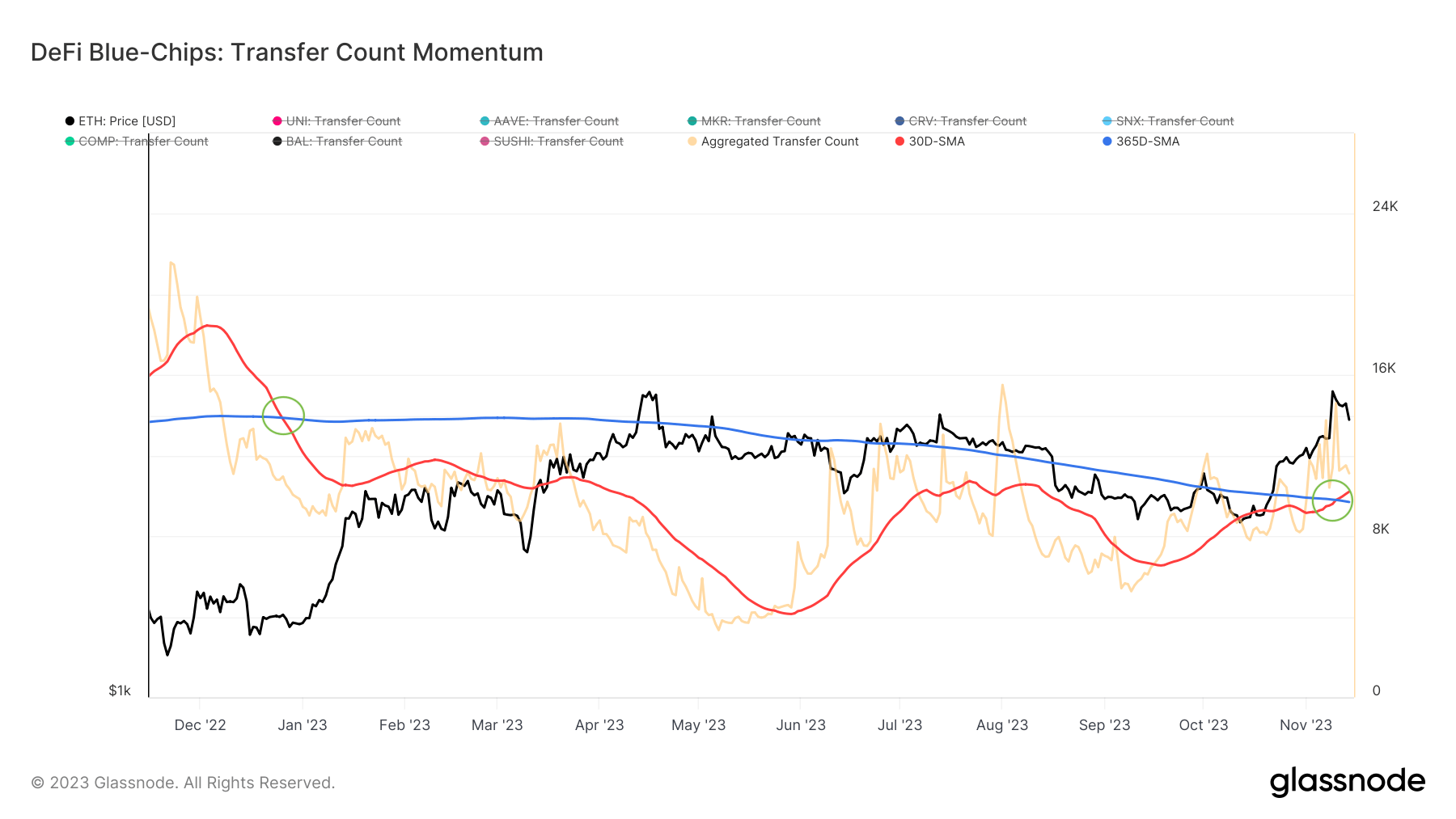

In the context of Ethereum’s DeFi ecosystem, transfer counts act as a proxy for economic throughput. When the 30D-SMA rises above the 365D-SMA, it suggests that the current frequency of transactions is outpacing the yearly average, indicating an expansion in network usage. As of November 14, 2023, the 30D-SMA for these blue-chip tokens reached 12,208, notably higher than the 365D-SMA of 9,699. This development is particularly significant because it represents the first major breakout of the monthly average over the yearly average since the market downturn began in late 2022.

The period following the collapse of major centralized entities in 2022 saw a dramatic contraction in DeFi activity. For nearly a year, the 30D-SMA trailed the 365D-SMA, reflecting a "risk-off" environment where capital remained stagnant. The recent reversal suggests that market participants are once again engaging with decentralized protocols for lending, borrowing, and liquidity provision, potentially anticipating a broader market recovery.

New User Adoption and Address Convergence

While transaction volume measures the activity of existing participants, the creation of new addresses serves as a vital metric for ecosystem growth and "new blood" entering the space. A healthy financial ecosystem requires a steady influx of new users to ensure liquidity and innovation. Data from Glassnode indicates that Ethereum’s blue-chip DeFi protocols are reaching a pivotal juncture regarding new user adoption.

On November 14, the 30D-SMA for new addresses stood at 1,155, nearly converging with the 365D-SMA of 1,165. In technical analysis, such a convergence often precedes a "cross," where the short-term average climbs above the long-term average. This trend indicates that the rate of new wallet creation is accelerating, recovering from the lows seen during the height of the crypto winter.

This resurgence in address creation is not happening in a vacuum. It follows a period of intense development within these protocols. For instance, Uniswap has been progressing toward its V4 implementation, Aave has expanded its V3 deployment across multiple Layer 2 solutions, and MakerDAO has aggressively integrated Real-World Assets (RWA) into its collateral base. These fundamental improvements appear to be attracting a new wave of users who are seeking transparent, code-based financial services over their centralized counterparts.

Historical Context and the Path to Recovery

To understand the significance of the current data, one must look at the timeline of Ethereum’s DeFi evolution. The "DeFi Summer" of 2020 marked the initial explosion of the sector, where protocols like Compound and Uniswap pioneered liquidity mining and automated market making. This was followed by a period of exuberant growth in 2021, which eventually culminated in a sharp correction throughout 2022.

The 2022 "crypto winter" was characterized by a series of systemic shocks, including the de-pegging of the Terra/Luna ecosystem and the subsequent bankruptcy of FTX. These events led to a massive deleveraging event across the industry. During this time, DeFi blue chips saw their valuations and on-chain metrics crater as investors fled to the safety of stablecoins or exited the market entirely.

However, throughout 2023, the narrative began to shift. While price action remained relatively muted for the first half of the year, the underlying technology continued to mature. The Ethereum network successfully completed the "Shanghai" upgrade, allowing for the withdrawal of staked ETH, which in turn bolstered the Liquid Staking Derivatives (LSD) market—a sector closely intertwined with DeFi blue chips like Aave and Curve. The current data suggesting a "poised for growth" status is the culmination of a year-long rebuilding phase.

Protocol-Specific Contributions to Growth

The recovery is not uniform across all assets, but rather driven by specific catalysts within the blue-chip category.

Maker (MKR) and the RWA Revolution

MakerDAO has been a standout performer, largely due to its "Endgame" transition and its strategic move into United States Treasury bonds. By onboarding real-world assets, Maker has been able to generate significant protocol revenue even during periods of low on-chain volatility. This has increased the utility of the MKR token, as it remains central to the governance and stability of the DAI stablecoin.

Aave (AAVE) and Cross-Chain Expansion

Aave has maintained its dominance in the lending market by focusing on safety and multi-chain accessibility. The launch of its native stablecoin, GHO, and the continued success of Aave V3 on Ethereum Layer 2s like Arbitrum and Optimism have contributed to the uptick in transfer counts. As users seek yield in a rising interest rate environment, Aave’s transparent lending pools offer an attractive alternative to traditional fixed-income products.

Uniswap (UNI) and Governance Evolution

As the leading decentralized exchange by volume, Uniswap remains the primary gateway for token swaps. The anticipation surrounding Uniswap V4, which introduces "hooks" for greater customization, has kept the protocol at the forefront of investor interest. Furthermore, ongoing discussions regarding a "fee switch" that would direct protocol revenue to UNI holders continue to be a major talking point for market analysts.

Broader Market Implications and Institutional Interest

The potential growth of Ethereum’s DeFi blue chips has implications that extend beyond the decentralized finance niche. As institutional interest in Ethereum grows—evidenced by the filing of several spot Ethereum ETFs by major asset managers like BlackRock—the protocols that run on top of the network are likely to receive increased scrutiny and investment.

Institutional investors often prefer "blue chip" assets because they offer a combination of proven track records and high liquidity. If Ethereum is viewed as the "internet of value," then protocols like Uniswap and Aave are its primary financial utilities. An expansion in on-chain activity for these tokens suggests that the infrastructure is ready to handle a higher volume of institutional capital.

Furthermore, the growth in DeFi metrics provides a counter-narrative to those who argued that decentralized finance was a passing fad. The fact that transfer counts and user adoption are rebounding while regulatory pressure remains high demonstrates the inherent resilience of permissionless protocols. Unlike centralized platforms, these protocols have continued to operate without interruption, processing billions of dollars in volume through code-based execution.

Risks and Challenges to the Growth Thesis

Despite the positive data, several challenges remain that could temper the growth of DeFi blue chips. Regulatory uncertainty continues to be a significant headwind, particularly in the United States, where the SEC has scrutinized decentralized platforms and their governance tokens. The classification of these tokens remains a point of contention, and any adverse legal rulings could impact liquidity and user access.

Security also remains a perennial concern. While blue-chip protocols are among the most audited and battle-tested in the world, the DeFi space is still susceptible to smart contract vulnerabilities and economic exploits. A major hack on a top-tier protocol could quickly reverse the positive momentum observed in the current moving averages.

Finally, the competition from emerging ecosystems cannot be ignored. While Ethereum remains the gravity center for DeFi, networks like Solana and various Ethereum Layer 2s are competing for market share by offering lower transaction costs and faster execution. The "blue chips" must continue to innovate and integrate with these scaling solutions to maintain their leadership positions.

Conclusion: A Pivotal Moment for Decentralized Finance

The convergence of rising transfer counts and accelerating new address creation suggests that Ethereum’s DeFi blue chips are entering a new cycle of growth. The data from mid-November 2023 indicates that the market has moved past the "bottoming out" phase and is now seeing genuine expansion in utility and adoption.

For investors and market participants, these metrics provide a data-driven basis for optimism. The transition of the 30D-SMA above the 365D-SMA for token transfers is a classic signal of a trend reversal, while the near-convergence of new address SMAs points to a broadening user base. As the broader cryptocurrency market looks toward 2024—with potential catalysts such as the Bitcoin halving and Ethereum’s technical roadmap—the DeFi blue chips appear well-positioned to lead the next wave of on-chain financial innovation. The resilience of these protocols over the past year has solidified their status as the "blue chips" of the digital age, and their current momentum suggests that the decentralized financial revolution is far from over.