These "blue-chip" tokens—a group comprising Uniswap (UNI), Aave (AAVE), Maker (MKR), Curve (CRV), Synthetix (SNX), Compound (COMP), Balancer (BAL), and Sushiswap (SUSHI)—represent the foundational layer of the decentralized economy. Because these protocols facilitate the majority of decentralized trading, lending, and synthetic asset creation, their on-chain health is often viewed as a leading indicator for the broader cryptocurrency market. Recent data from Glassnode reveals a significant reversal in momentum, particularly regarding token transfer counts and new user acquisition, which historically precede broader price appreciation and ecosystem growth.

The Significance of Transfer Count Momentum

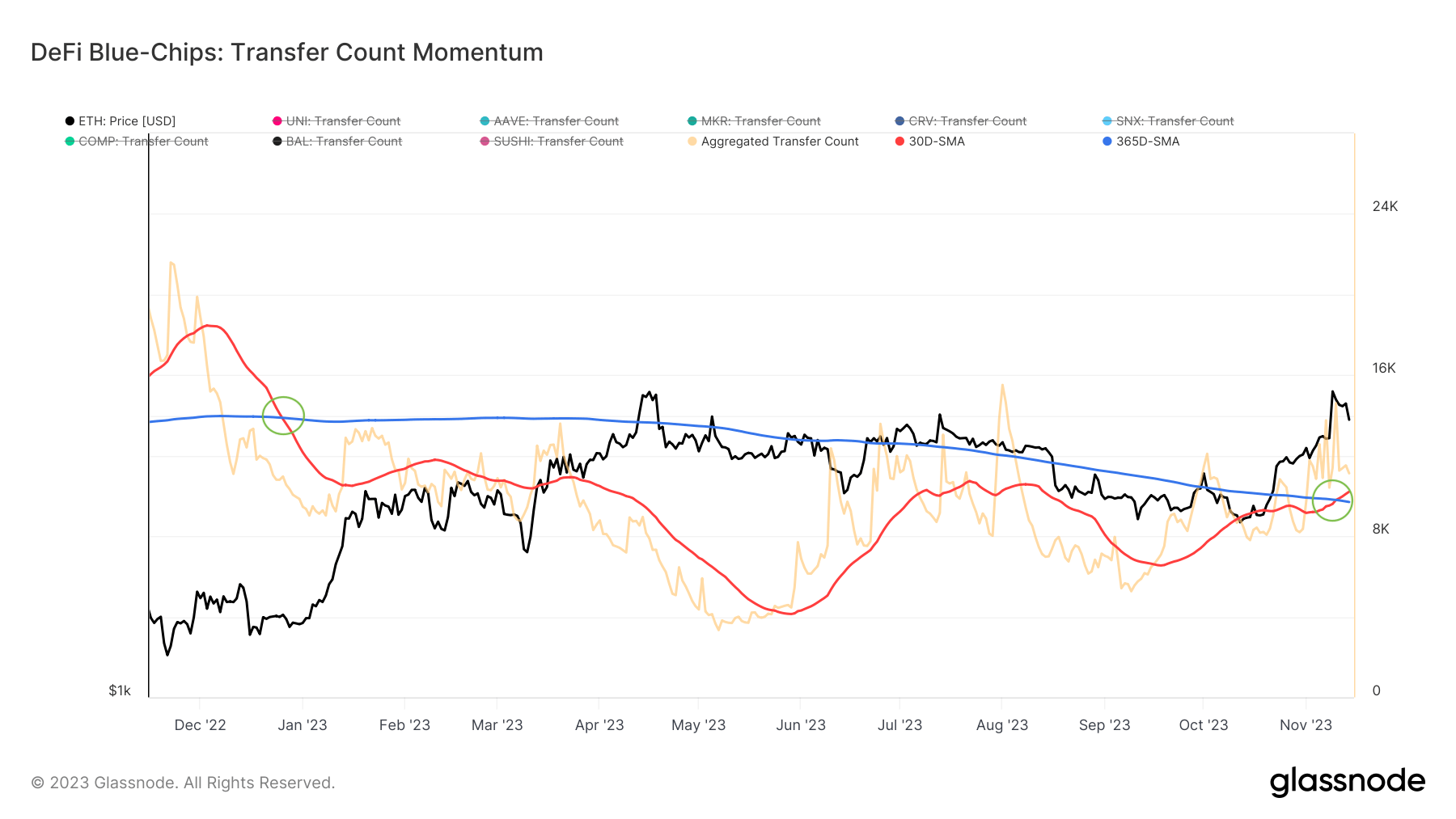

A critical metric for assessing the health of any digital asset is its transfer count momentum. This metric tracks the number of times a token is moved on-chain, serving as a proxy for both utility and investor demand. In a healthy, growing market, short-term activity should ideally outpace long-term averages, indicating that the asset is being actively used and traded rather than sitting dormant in "cold" wallets.

In the context of Ethereum’s DeFi blue chips, analysts compare the 30-day Simple Moving Average (30D-SMA) of transfer counts against the 365-day Simple Moving Average (365D-SMA). This "fast" versus "slow" comparison helps filter out daily volatility to reveal underlying structural trends. When the monthly average (30D) surpasses the yearly average (365D), it signifies an "expansion" in on-chain activity.

As of November 14, 2023, the 30D-SMA for these blue-chip tokens reached 12,208, notably higher than the 365D-SMA of 9,699. This development is particularly significant because the monthly average had remained stubbornly below the yearly average since the fourth quarter of 2022. The crossover indicates that the contraction phase, which began in the wake of the FTX collapse and the subsequent regulatory crackdown, may have finally concluded. This surge in transfers suggests that participants are once again engaging with DeFi protocols for yield generation, liquidity provision, and governance.

Chronology of the DeFi Market Cycles

To understand the weight of this current recovery, it is necessary to examine the timeline of the DeFi sector over the last three years. The "DeFi Summer" of 2020 marked the initial explosion of the sector, where protocols like Uniswap and Compound introduced the world to automated market makers (AMMs) and algorithmic lending. This period saw the 30D-SMA of activity dwarf long-term averages as capital flooded into the ecosystem.

By 2021, the market reached a fever pitch, with Total Value Locked (TVL) across Ethereum-based protocols surpassing $100 billion. However, the onset of the 2022 "crypto winter" brought a series of systemic shocks. The collapse of the Terra-LUNA ecosystem in May 2022, followed by the insolvency of Celsius and Three Arrows Capital, led to a massive deleveraging event. By the time FTX collapsed in November 2022, the 30D-SMA of transfer counts for blue-chip tokens fell sharply below the 365D-SMA, where it remained for nearly a year.

The period from late 2022 through mid-2023 was characterized by a "wait-and-see" approach from investors. While the underlying technology of protocols like Aave and MakerDAO remained robust—proving their resilience by functioning perfectly during the market crashes—the lack of new capital and user interest resulted in a stagnant on-chain environment. The November 2023 data suggests that this period of hibernation has ended, as the "golden cross" of moving averages reflects a return of active participation.

New User Adoption and Address Momentum

While transfer counts measure the activity of existing participants, the creation of new addresses serves as a barometer for market expansion and the onboarding of new capital. The momentum of new DeFi addresses is calculated similarly to transfer counts, comparing the monthly average of new address creation against the yearly average.

Data from mid-November 2023 shows a pivotal moment in this metric. The 30D-SMA of new addresses for Ethereum’s blue-chip protocols reached 1,155, nearly converging with the 365D-SMA of 1,165. While the monthly average has not yet decisively broken above the yearly average, the narrowing gap indicates a resurgence in new user interest.

In the world of blockchain analytics, convergence often precedes a breakout. The fact that new address creation is accelerating after a long period of decline suggests that the "bottom" for user adoption has likely been formed. This trend is bolstered by the increasing integration of DeFi with traditional financial concepts, such as Real World Assets (RWAs).

Profiling the Blue-Chip Ecosystem

The protocols driving this momentum are not speculative "meme" coins but are instead revenue-generating entities with established product-market fit.

- Uniswap (UNI): As the dominant decentralized exchange, Uniswap continues to lead in volume. The anticipation surrounding Uniswap v4, which promises "hooks" for greater customization, has kept developer interest high.

- Aave (AAVE): The leading lending protocol has successfully launched its native stablecoin, GHO, and has expanded its V3 deployment across multiple Layer 2 networks, increasing its accessibility and capital efficiency.

- Maker (MKR): Perhaps the most successful "pivot" in the sector, MakerDAO has aggressively integrated US Treasuries and other RWAs into its collateral base. This has allowed the protocol to capture high interest rates from the traditional financial world, driving significant revenue back to MKR holders through buybacks.

- Curve (CRV) and Balancer (BAL): These protocols remain the backbone of liquidity for stablecoins and complex asset pools. Despite a high-profile exploit earlier in the year, Curve has demonstrated resilience, with its crvUSD stablecoin gaining traction.

- Synthetix (SNX): By providing the liquidity layer for perpetual futures and synthetic assets, Synthetix has become a core component of the "DeFi composability" stack, benefiting from the rise of decentralized derivatives trading.

Supporting Data and Technical Analysis

The recovery in DeFi metrics coincides with a broader stabilizing of the Ethereum network. Since the "Merge" to Proof of Stake and the subsequent "Shapella" upgrade, Ethereum has become a yield-bearing asset, which in turn makes DeFi protocols more attractive.

Furthermore, the growth of Layer 2 (L2) scaling solutions such as Arbitrum, Optimism, and Base has significantly reduced the cost of interacting with these blue-chip protocols. While the Glassnode data focuses on Ethereum mainnet activity, the "wealth effect" from L2s often flows back into the mainnet governance tokens of these protocols.

Market analysts point out that the current 30D-SMA of 12,208 transfers is still far below the peaks of 2021, where counts frequently exceeded 40,000. However, the importance lies in the rate of change rather than the absolute number. A 25% increase in the monthly average relative to the yearly average is a statistically significant deviation that typically indicates a shift in market regime from "bearish/neutral" to "early-stage bullish."

Industry Reactions and Analyst Perspectives

While official statements from protocol foundations are typically focused on technical development rather than token price or transfer metrics, the broader sentiment among DeFi researchers is one of cautious optimism. Analysts at several on-chain research firms have noted that the "quality" of current activity appears higher than in previous cycles.

During the 2021 boom, much of the transfer volume was driven by "yield farming" and circular logic that lacked long-term sustainability. In contrast, the current uptick is occurring in an environment where "lazy capital" has been flushed out. The users remaining—and the new ones entering—are engaging with protocols that have survived multiple "black swan" events.

Inferred reactions from institutional observers suggest that the focus on MakerDAO’s RWA integration and Aave’s institutional-grade lending pools (Aave Arc) is beginning to pay dividends. As one analyst noted, "We are seeing a transition from DeFi as a ‘crypto-native playground’ to DeFi as ‘global financial infrastructure.’ The transfer counts are finally starting to reflect that reality."

Broader Impact and Future Implications

The potential growth of Ethereum’s blue-chip DeFi tokens has implications that extend beyond the immediate price of UNI or AAVE. As these protocols regain momentum, they provide the necessary liquidity and infrastructure for the next generation of decentralized applications (dApps).

A robust DeFi sector acts as a "sink" for Ethereum, as users lock ETH into smart contracts to mint stablecoins or provide liquidity. This reduces the circulating supply of ETH, potentially creating upward price pressure on the network’s native asset. Furthermore, a thriving DeFi ecosystem attracts developers who build increasingly complex financial products, such as decentralized insurance and undercollateralized lending.

However, the path forward is not without risks. Regulatory scrutiny remains a primary concern, as authorities in the United States and Europe continue to debate how to categorize and regulate decentralized protocols. The outcome of ongoing legal battles involving the SEC and various crypto entities will undoubtedly impact the speed of DeFi adoption.

Additionally, the sustainability of the growth in new addresses will be the key factor to monitor in 2024. For a full-scale market recovery to occur, the 30D-SMA for new addresses must not only converge with the 365D-SMA but must break above it and stay there. This would signal that DeFi has moved beyond its current user base and is successfully capturing the interest of a wider demographic.

In conclusion, the data from November 2023 serves as a compelling piece of evidence that the DeFi sector is at a crossroads. The surge in transfer momentum and the stabilization of new user adoption suggest that the foundational protocols of the Ethereum network are poised for a new chapter of growth. While the "irrational exuberance" of previous years has faded, it has been replaced by a more mature, data-driven expansion that could redefine the future of decentralized finance.