Cari Network has announced a strategic initiative to develop a bank-governed tokenized deposit platform, selecting ZKsync’s advanced Prividium stack as its foundational technology. This ambitious project aims to equip US regional lenders with an innovative on-chain payments rail, designed to offer customers tokenized deposits that emulate the speed and transferability inherent in stablecoins, while meticulously preserving the robust benefits of traditional banking infrastructure and stringent compliance protocols. This development signifies a notable acceleration in the integration of distributed ledger technology (DLT) within the conventional financial sector, particularly for institutions seeking to modernize payment systems and enhance operational efficiencies without compromising regulatory adherence.

The Innovation at Hand: Tokenized Deposits

Tokenized deposits represent a critical evolution in the financial landscape, bridging the gap between traditional fiat currency and the burgeoning digital asset ecosystem. Unlike stablecoins, which are typically issued by private entities and peg their value to a fiat currency or other assets, tokenized deposits are direct liabilities of a regulated depository institution. They are essentially digital representations of customer deposits held at a commercial bank, operating on a blockchain or DLT network. This distinction is crucial for regulatory bodies, as it places tokenized deposits squarely within the existing framework of bank supervision and deposit insurance, such as that provided by the Federal Deposit Insurance Corporation (FDIC) in the United States.

The primary allure of tokenized deposits for financial institutions and their clients lies in their potential to revolutionize payment processing. By leveraging blockchain technology, these deposits can facilitate near-instantaneous settlement, 24/7 availability, and enhanced programmability, features that are largely absent in traditional interbank payment systems like ACH or even wire transfers, which often operate with limited hours and slower settlement times. For US regional banks, the adoption of such a platform could translate into significant operational cost reductions, improved liquidity management, and the ability to offer novel, digitally native services to their customers, thereby staying competitive in an increasingly digital-first economy. The promise of stablecoin-like speed and transferability, combined with the inherent trust and regulatory oversight of a bank, positions tokenized deposits as a potentially transformative financial instrument.

Cari Network’s Vision and the Regional Banking Landscape

Cari Network’s decision to focus on US regional banks is particularly insightful, given the unique challenges and opportunities faced by this segment of the financial industry. Regional banks, while vital pillars of local economies, have increasingly contended with competitive pressures from larger national and international banks, fintech disruptors, and the ever-present need to innovate without the expansive budgets of their larger counterparts. According to data from the FDIC, there are thousands of community and regional banks across the US, collectively holding trillions in assets and playing a critical role in small business lending and local community development. However, many struggle with outdated legacy technology infrastructure, which can hinder their ability to adapt to modern customer expectations for digital services.

Cari Network envisions its platform as a democratizing force, providing regional banks with access to cutting-edge blockchain technology that might otherwise be out of reach. By offering a shared, bank-governed infrastructure, Cari Network aims to mitigate the individual development costs and regulatory complexities that each bank would face if attempting to build such a system independently. The "bank-governed" aspect is paramount, suggesting a collaborative model where participating banks have a stake in the platform’s governance, ensuring that its evolution aligns with their collective interests and regulatory requirements. This approach fosters trust and collective ownership, crucial for broad adoption within a conservative industry.

For regional banks, the advantages extend beyond just faster payments. Tokenized deposits could enable new product offerings, such as instant cross-border payments for businesses, enhanced treasury management solutions, and even integration with emerging Web3 applications in a compliant manner. This could help regional banks attract and retain a younger, digitally savvy clientele, while also providing existing business customers with more efficient ways to manage their finances.

ZKsync’s Prividium Stack: A Foundation for Institutional Trust

The selection of ZKsync’s Prividium stack underscores the critical requirements for privacy, compliance, and full data control in institutional DLT adoption. ZKsync, developed by Matter Labs, is a leading Layer 2 scaling solution for Ethereum, leveraging zero-knowledge (ZK) proofs to enhance transaction throughput and reduce costs while inheriting Ethereum’s robust security guarantees. Prividium specifically tailors this technology for enterprise and institutional use cases.

Prividium’s architecture is purpose-built to address the stringent demands of regulated financial entities. Key features include:

- User-level privacy: Utilizing ZK proofs, Prividium allows for transaction verification without revealing sensitive underlying data to all network participants, a non-negotiable requirement for financial institutions dealing with confidential customer and transaction information. This cryptographic technique ensures that only necessary information is disclosed, satisfying regulatory obligations like Know Your Customer (KYC) and Anti-Money Laundering (AML) while maintaining transactional privacy.

- Compliance tools: The platform is designed with integrated tools that facilitate adherence to global financial regulations. This includes features for identity verification, transaction monitoring, reporting capabilities, and mechanisms for regulatory access to data when legally required, all within a controlled environment.

- Cross-chain connectivity: In an increasingly interconnected digital world, the ability to seamlessly interact with other blockchain networks is vital. Prividium’s design supports cross-chain interoperability, allowing tokenized deposits to potentially move across different DLTs or interact with various decentralized finance (DeFi) protocols, albeit within a permissioned and compliant framework. This future-proofs the platform against an evolving blockchain ecosystem.

- Ethereum-grade security: By building on the foundation of ZKsync, Prividium benefits from the battle-tested security and decentralization of the Ethereum mainnet. The security model ensures that transactions are immutable and tamper-proof, providing the high level of assurance required for managing monetary assets.

The integration of ZKsync’s advanced ZK proof technology is a game-changer for institutional adoption. Zero-knowledge proofs allow one party to prove to another that a statement is true, without revealing any information beyond the validity of the statement itself. In the context of financial transactions, this means that a bank could prove a transaction occurred and complied with regulations, without disclosing the identities of the parties involved or the specific amounts to unauthorized observers on the public ledger. This delicate balance of transparency and privacy is precisely what institutions like regional banks require to confidently operate in a DLT environment.

The Regulatory and Market Context for Digital Assets

The move by Cari Network and ZKsync is not an isolated event but rather indicative of a broader trend within traditional finance to explore and adopt DLT. Over the past few years, central banks, regulators, and commercial banks globally have intensified their research and pilot programs into various forms of digital money and tokenized assets.

- Central Bank Digital Currencies (CBDCs): Projects like the Federal Reserve’s Project Cedar in the US, the European Central Bank’s digital euro exploration, and the Bank for International Settlements’ initiatives (e.g., Project Dunbar) highlight a global push to understand the implications of sovereign digital currency. While tokenized deposits are distinct from CBDCs, their development contributes to the broader ecosystem of digital money and may pave the way for future interoperability.

- Regulatory Guidance: In the US, regulators have gradually provided more clarity on digital assets. The Office of the Comptroller of the Currency (OCC) has issued interpretive letters acknowledging the ability of national banks and federal savings associations to engage in certain cryptocurrency-related activities, including holding stablecoin reserves. While not directly addressing tokenized deposits, these pronouncements signal a growing regulatory acceptance of digital assets within the banking framework.

- Industry Collaboration: Initiatives like the Regulated Liability Network (RLN) in the US, a proof-of-concept involving major banks, the New York Fed, and others, also explore a common DLT platform for regulated deposits and other tokenized assets. These efforts underscore the industry-wide recognition of the need for modernized payment rails and the potential of tokenization.

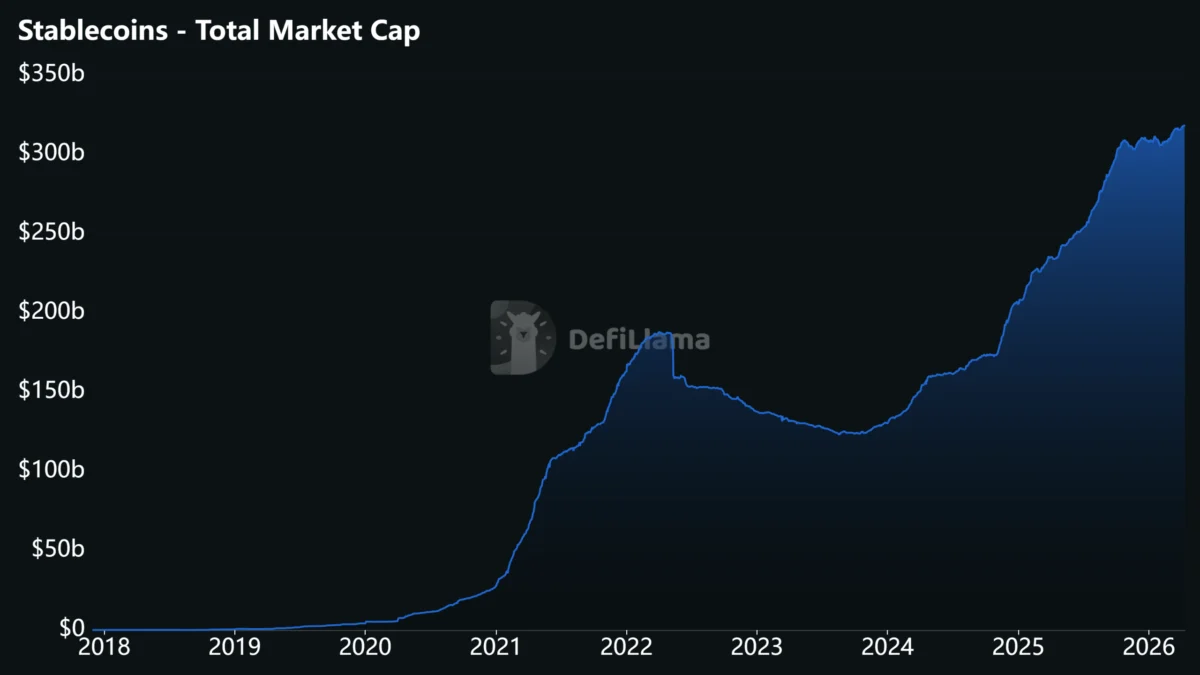

The market for stablecoins alone has grown exponentially, reaching hundreds of billions in market capitalization, demonstrating a clear demand for digital assets that maintain a stable value. This market growth serves as a powerful indicator of the potential for tokenized deposits, which offer similar transactional benefits but with the added layer of direct bank liability and regulatory oversight, potentially appealing to a wider range of institutional users and risk-averse consumers.

The Distinction: Tokenized Deposits vs. Stablecoins vs. CBDCs

It is crucial to differentiate between these three forms of digital money to fully grasp the significance of Cari Network’s platform:

- Stablecoins: Typically privately issued cryptocurrencies pegged to a stable asset (e.g., USD). They aim to maintain a stable value but carry issuer-specific risks and varying levels of regulatory oversight depending on jurisdiction and issuer. They are not direct liabilities of a regulated bank in the same way traditional deposits are. Examples include USDT and USDC.

- Tokenized Deposits: Digital representations of traditional bank deposits held at a commercial bank. They are direct liabilities of a regulated financial institution and benefit from existing deposit insurance schemes (like FDIC). They combine the security and regulatory framework of traditional banking with the efficiency and programmability of blockchain technology. This is what Cari Network is building.

- Central Bank Digital Currencies (CBDCs): Digital forms of a country’s fiat currency, issued and backed by its central bank. They would be a direct liability of the central bank, carrying no credit risk or liquidity risk. CBDCs are still largely in the research or pilot phase globally, with many jurisdictions debating their necessity and design.

Cari Network’s focus on tokenized deposits leverages the best of both worlds: the innovation of blockchain for payments and the trust and regulatory security of the existing banking system. This approach is likely to garner more immediate acceptance from regulators and traditional financial institutions compared to privately issued stablecoins or a potentially disruptive CBDC.

Statements and Perspectives from Key Stakeholders (Inferred)

While specific official statements were not provided in the original prompt, logical inferences can be drawn regarding the likely perspectives of the involved parties:

- Cari Network: Would likely emphasize its commitment to empowering regional banks with cutting-edge technology, enhancing financial inclusion, and driving efficiency within the traditional financial system. A spokesperson might state, "Our platform on ZKsync’s Prividium stack represents a monumental step towards future-proofing regional banks. We are providing a compliant, secure, and highly efficient on-chain payment rail that allows them to innovate and compete effectively in the digital age, without compromising the trust and regulatory benefits their customers expect."

- ZKsync (Matter Labs): Would highlight the robustness, privacy, and scalability of its Prividium stack, showcasing its suitability for demanding institutional applications. They might articulate, "The selection of Prividium by Cari Network validates our dedication to building a blockchain infrastructure that meets the stringent requirements of regulated financial institutions. Our zero-knowledge technology offers the unique blend of privacy, compliance, and Ethereum-grade security essential for tokenized deposits, demonstrating the real-world utility of ZKsync beyond decentralized finance."

- Regional Banks (Prospective Users): Would express enthusiasm for the potential to modernize their operations, reduce costs, and offer new services. A hypothetical regional bank executive might remark, "This initiative offers a much-needed pathway for regional banks to embrace blockchain technology in a secure and compliant manner. The ability to offer instant, tokenized deposits could be a game-changer for our business clients, improving liquidity and streamlining their operations, while also making us more competitive against larger institutions."

- Regulators: While cautious, regulators would likely view this development with interest, recognizing the potential for improved payment efficiency and risk management, provided robust compliance frameworks are in place. Their primary focus would remain on consumer protection, financial stability, and preventing illicit activities.

Broader Implications for the Financial Ecosystem

The successful deployment and adoption of Cari Network’s platform could have far-reaching implications:

- Enhanced Interoperability: A standardized, bank-governed tokenized deposit platform could foster greater interoperability between different financial institutions and potentially with broader DLT ecosystems, paving the way for a more integrated and efficient global financial system.

- Innovation in Financial Products: The programmability of tokenized deposits opens doors for entirely new financial products and services, from automated escrow accounts to instant dividend distributions and sophisticated supply chain finance solutions.

- Cost Reduction and Efficiency: Automation and near-instant settlement inherent in DLT can drastically reduce the operational costs associated with traditional payment processing, benefiting both banks and their customers.

- Validation for Blockchain Technology: Institutional adoption of DLT for core banking functions, especially by a network of regulated banks, provides significant validation for the underlying blockchain technology, moving it further into the mainstream.

- Competitive Edge for Regional Banks: This platform could level the playing field, allowing regional banks to offer services previously only accessible to larger, more technologically advanced institutions, helping them retain and attract customers.

Challenges and the Road Ahead

Despite the immense promise, the path to widespread adoption of tokenized deposits is not without its challenges.

- Regulatory Clarity: While progress has been made, comprehensive regulatory frameworks specifically for tokenized deposits are still evolving. Harmonization across different jurisdictions and clear guidance from bodies like the Federal Reserve, OCC, and FDIC will be crucial for scaling.

- Interoperability Standards: Ensuring seamless interaction between different tokenized deposit platforms, other DLTs, and legacy systems will require the development and adoption of robust technical standards.

- Cybersecurity and Risk Management: While ZKsync offers strong security, the integration of new technology always introduces new vectors for cyber threats. Banks will need to invest heavily in cybersecurity infrastructure and risk management protocols.

- Operational Integration: Integrating a new DLT-based payment rail into existing, often complex, core banking systems will require significant IT investment, training, and careful change management.

- Market Education and Adoption: Educating both financial institutions and their end customers about the benefits and mechanics of tokenized deposits will be vital for fostering trust and encouraging widespread usage.

In conclusion, Cari Network’s initiative to build a bank-governed tokenized deposit platform on ZKsync’s Prividium stack marks a significant milestone in the convergence of traditional finance and blockchain technology. By addressing the critical needs of US regional banks for speed, transferability, privacy, and compliance, this platform has the potential to redefine the future of payments and empower a vital segment of the financial industry. Its success will not only depend on technological prowess but also on collaborative efforts with regulators and a commitment to seamless integration into the existing financial ecosystem, ultimately shaping a more efficient, secure, and digitally advanced banking future.