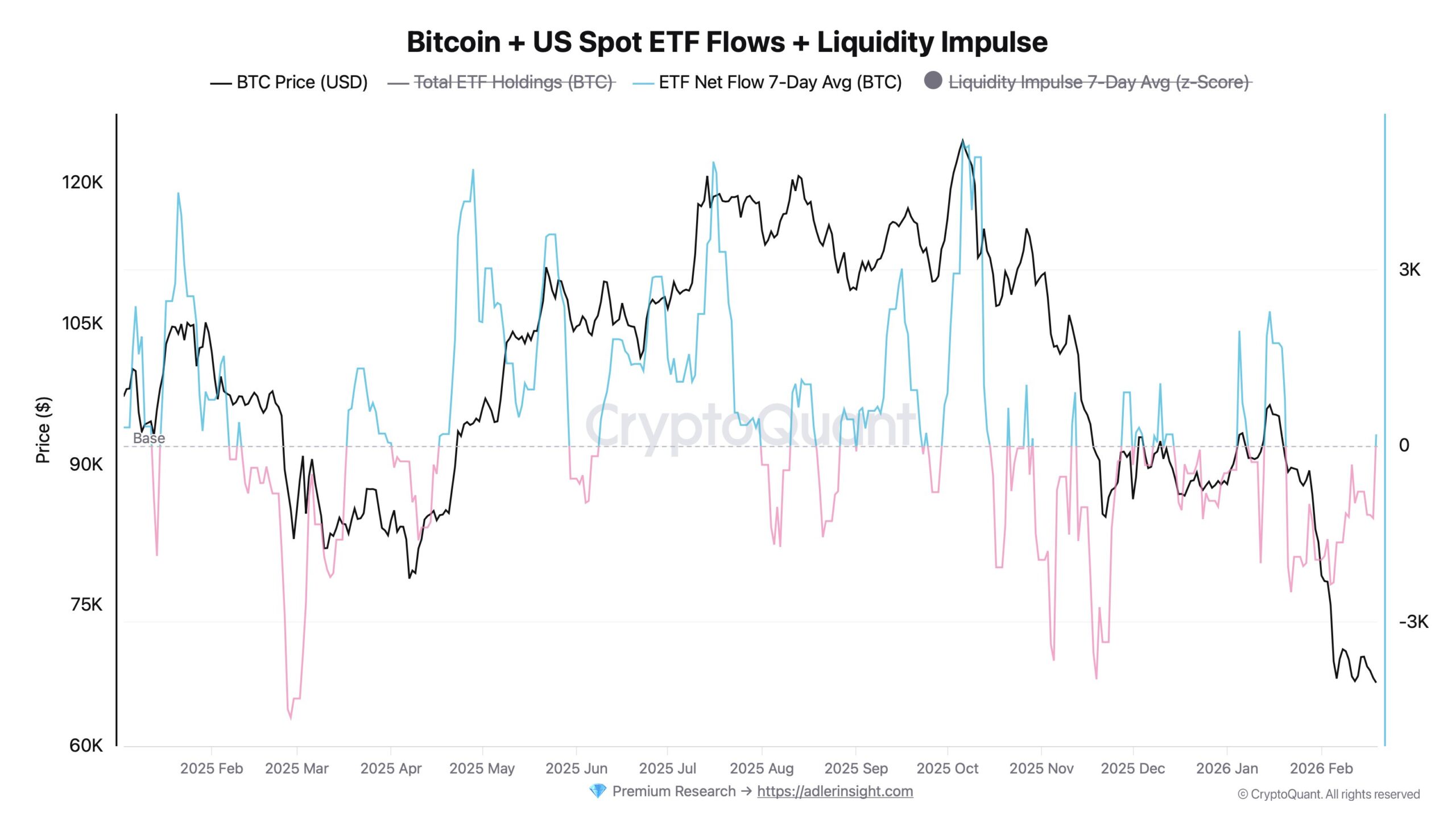

Spot Bitcoin exchange-traded funds (ETFs) are currently navigating a challenging period, marked by a fourth consecutive month of net outflows, coinciding with Bitcoin (BTC) itself approaching a fifth negative monthly close in February. This pronounced slowdown is evident across several key indicators, including shrinking fund balances and persistently bearish rolling net flow data, especially when juxtaposed with the performance of competing asset ETFs. As both Bitcoin’s price and the aggregate holdings within these institutional investment vehicles have trended downwards since October, investors across the globe are keenly seeking clarity on the potential trajectory for the premier cryptocurrency.

The introduction of spot Bitcoin ETFs in various jurisdictions, particularly the United States, was heralded as a watershed moment for the cryptocurrency market. These funds were anticipated to bridge the gap between traditional finance and the nascent digital asset space, offering institutional and retail investors regulated access to Bitcoin without the complexities of direct ownership, such as self-custody or navigating cryptocurrency exchanges. The initial excitement following their approval led to a significant influx of capital, propelling net assets held in US spot Bitcoin ETFs to an impressive peak near $170 billion in October 2025. This surge underscored the pent-up demand and the optimism surrounding Bitcoin’s integration into mainstream investment portfolios. Cumulative net inflows reached an all-time high of approximately $63 billion during this period, signaling robust institutional adoption and a new era for digital asset investing.

However, the narrative has demonstrably shifted. By February 2026, net assets within these ETFs had plummeted to $84.3 billion, representing a near 50% reduction from their peak just four months prior. The cumulative net inflows have also seen a substantial retraction, falling to roughly $54 billion. More strikingly, since July 2025, cumulative net flows have totaled a mere $5 billion, a stark indicator of the dramatic deceleration in fresh capital infusions into these once-frenetic investment products. This sharp reversal from an era of unprecedented growth to one of sustained contraction has ignited considerable debate regarding the immediate future of Bitcoin and the broader implications for institutional interest in digital assets.

Detailed analysis of recent flow data provides a granular view of the challenges. Bitcoin researcher Axel Adler Jr. meticulously tracked seven sessions between February 12 and February 19, 2026, revealing a cumulative net outflow of 11,042 BTC from the spot ETFs. The period was punctuated by significant divestment, with February 12 marking the largest single-day reduction at 6,120 BTC, equivalent to approximately $416 million at prevailing market prices. This substantial one-day outflow sent ripples through the market, contributing to the broader bearish sentiment. The subsequent days of February 17 and February 18 saw back-to-back outflows of 1,520 BTC and 1,980 BTC, respectively, further cementing the trend of capital withdrawal. Amidst this torrent of negative flows, only two sessions registered positive inflows, with the February 6 session adding 5,900 BTC to the funds. Adler’s analysis underscores the severity of the situation, positing that a minimum of three consecutive positive sessions would be required to signal a genuine renewed accumulation trend within these ETFs. Until such a pattern emerges, the continuous outflows from these funds are effectively acting as a consistent source of supply for the market, contributing to downward price pressure on Bitcoin.

The macroeconomic landscape appears to be aligning with this cooling trend observed in the ETF sector. Since November 2025, the spot Bitcoin ETFs have collectively shed approximately 87,000 BTC. February 2026 alone witnessed outflows of roughly 15,000 BTC, highlighting the accelerated pace of divestment. The total Bitcoin held across all spot ETFs now hovers around 1.26 million BTC, a noticeable decline from the peak of 1.36 million BTC. This reduction in holdings is not uniformly distributed across all funds, with some experiencing more significant withdrawals than others. For instance, BlackRock’s IBIT, one of the largest and most prominent Bitcoin ETFs, saw its holdings decline to 759,000 BTC from an earlier 806,000 BTC, representing a 6% reduction. Fidelity’s FBTC experienced an even more substantial proportional decline, dropping by 12.6% from 213,000 BTC to 186,000 BTC. While these figures represent significant withdrawals, Bitcoin’s price has fallen even more sharply than the ETF balances, suggesting that the broader spot market demand has been insufficient to fully absorb the pervasive selling pressure emanating from various market participants, not solely limited to ETF redemptions.

In a broader context, the shift in investor preference is also evident when comparing Bitcoin ETFs with other established asset classes, particularly gold. Over the past two years, there has been a notable rotation of leadership between Bitcoin and gold ETFs, as measured by their 90-day rolling flows. Bitcoin’s 90-day inflows peaked impressively near $16 billion in March 2024, reflecting a period of intense speculative interest and institutional entry. These inflows subsequently cooled to a range of $3 billion to $4 billion between June and October 2024, before surging once more to $21.6 billion in December 2024, indicative of renewed bullish sentiment heading into the new year.

The trajectory for gold ETFs, however, followed a distinctly different path, often inverse to Bitcoin’s surges. Gold ETFs experienced negative flows for an extended period, which persisted until July 2024. Following this, capital began to accelerate into gold, reaching a significant $30 billion by April 2025. This period, notably March and April 2025, coincided with a downturn in Bitcoin’s 90-day flows, which slipped into negative territory at approximately $2 billion. This rotation suggests a flight to perceived safety as macroeconomic uncertainties began to mount or as investors de-risked from more volatile assets. Gold’s appeal as a traditional safe-haven asset was further underscored by its subsequent peak at $36 billion in October 2025, a period when Bitcoin inflows were notably fading into the final quarter of the year. Most recently, in January 2026, gold flows reached $29 billion before easing slightly to $21 billion by mid-February, while Bitcoin flows stubbornly remained in negative territory. The data vividly illustrates a repeated handoff between the two assets, with periods of weakening Bitcoin ETF demand consistently aligning with surges in gold inflows, particularly pronounced between March and October 2025. In relative terms, gold ETFs have effectively captured incremental capital as investors, faced with increased market volatility and economic uncertainty, have leaned towards an asset class characterized by smaller price swings and a much longer, proven track record as a store of value during risk-off phases. This dynamic highlights the evolving risk appetite of investors and their strategic allocation decisions between digital and traditional safe-haven assets.

ITC Crypto founder Benjamin Cowen has classified the first quarter of 2026 as a period of "late-cycle restrictive digestion" for both the equities and crypto markets. This analytical framework provides a crucial lens through which to understand the prevailing market conditions and the persistent outflows from Bitcoin ETFs. The US Federal Reserve’s monetary policy plays a central role in this environment. While the Fed concluded its quantitative tightening program in December 2025, thereby halting the balance sheet runoff, the overall monetary policy stance remains distinctly restrictive, especially when measured against prevailing market growth expectations. The federal funds rate continues to sit above the 2-year Treasury yield, a traditional indicator of tight monetary conditions. Furthermore, the 10-year Treasury yield trades near 4.1%, with the 10-year real yield hovering around 1.7%–1.8%. These figures indicate that investors can still earn inflation-adjusted positive returns in the fixed income markets, thereby significantly raising the opportunity cost of holding non-yielding assets such as Bitcoin. This environment naturally diverts capital from speculative or growth-oriented assets towards safer, yielding alternatives.

Cowen’s historical analysis further supports this thesis, noting that in prior tightening cycles, Bitcoin’s price has often shown signs of weakness and rolled over months before broader stress became apparent in equity markets. A salient example is 2019, when BTC price began its descent well ahead of the wider market downturn. This historical pattern suggests that Bitcoin, often viewed as a risk-on asset, is particularly sensitive to changes in liquidity and interest rate environments. Historically, durable and sustained inflows into Bitcoin ETFs have typically followed periods of falling real yields or the commencement of a clear monetary easing cycle by central banks. Critically, neither of these conditions has materialized as of February 2026. This absence of favorable macroeconomic catalysts provides a compelling explanation for the significant slowdown in demand for Bitcoin ETFs that has been observed since October 2025. The implication is clear: without a shift in monetary policy or a substantial reduction in real yields, the appeal of non-yielding assets like Bitcoin may remain subdued for institutional investors who are highly sensitive to risk-adjusted returns and opportunity costs.

The current environment represents a critical juncture for Bitcoin and the broader cryptocurrency market. The sustained outflows from spot Bitcoin ETFs challenge the optimistic narrative of continuous institutional adoption and highlight the inherent volatility and sensitivity of digital assets to macroeconomic factors. The initial exuberance surrounding the launch of these ETFs has been tempered by the realities of a restrictive monetary policy and shifting investor sentiment towards more traditional safe havens like gold. For a turnaround to occur, market participants will likely be closely monitoring several key indicators: a potential pivot in Federal Reserve policy towards easing, a consistent decline in real yields making non-yielding assets more attractive, and a sustained period of positive net inflows into the Bitcoin ETFs, signaling renewed accumulation. Until these conditions emerge, Bitcoin may continue to experience a period of "restrictive digestion," with price action and institutional interest remaining under pressure. This phase underscores the evolving maturity of the cryptocurrency market, where macroeconomics increasingly dictate sentiment and capital flows, moving beyond purely speculative drivers to a more integrated role within the global financial system.