The industrial foundation of the Bitcoin network is currently navigating one of the most significant structural transformations in its fifteen-year history. As the euphoria surrounding the record-breaking price highs of late 2025 dissipates, the sector is grappling with a convergence of unfavorable economic factors: a sharp decline in asset price, persistently high network difficulty, and a predatory shift in infrastructure demand from the artificial intelligence (AI) sector. Data indicates that Bitcoin is currently trading near the $78,000 mark, representing a punishing 38% retraction from its all-time high of approximately $126,000 achieved just four months prior. This price collapse has effectively erased the profit margins of all but the most efficient mining operations, triggering a massive migration of power and hardware resources toward high-performance computing (HPC) and AI workloads.

The Economics of Mining Capitulation

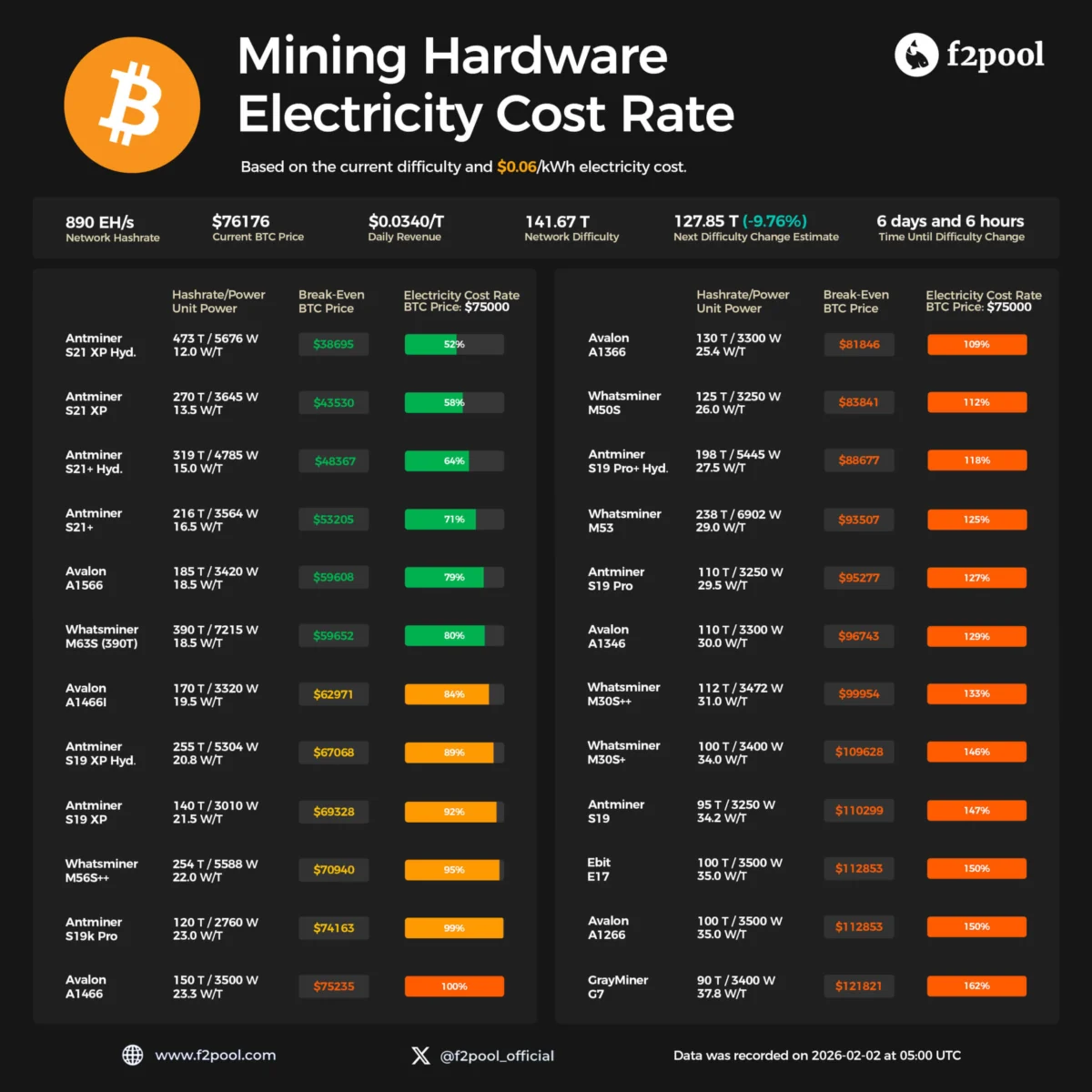

The current downturn is defined by a "hashprice" crisis—a metric that measures the expected value of 1 terahash of hashing power per day. According to data from the mining pool f2pool and Luxor Technology’s Hashrate Index, daily revenue has slumped to approximately $0.034 per terahash (TH/s) for operators paying a standard industrial electricity rate of $0.06 per kilowatt-hour (kWh). This figure represents a historical floor, lower even than the depths of the 2022 post-FTX market contagion.

The financial strain is reflected in the profit-and-loss sustainability index provided by analytics firm CryptoQuant. The index recently fell to a reading of 21, the lowest level recorded since late 2024. When this index drops below certain thresholds, it indicates that miners are "extremely underpaid" relative to the energy and capital expenditure required to secure the network. The result has been an immediate and visible contraction in network activity. Since November, Bitcoin’s total hashrate has declined by approximately 12%, marking the most significant drawdown since the Chinese government’s wholesale ban on mining in 2021. This has effectively reset the network’s computational power to levels not seen since September 2025, raising questions about the long-term trajectory of the network’s security budget.

A Chronology of the 2025-2026 Market Shift

The current crisis did not emerge in a vacuum but is the result of a specific sequence of market events over the last two quarters:

- October 2025: Bitcoin reaches a record high of over $126,000. Mining profitability surges, leading to massive orders for next-generation ASIC (Application-Specific Integrated Circuit) hardware. Network difficulty begins a steady climb as new rigs come online.

- November 2025: The market begins a cooling phase. However, hashrate continues to rise due to the lag in hardware delivery and installation, causing a "difficulty squeeze" where more miners compete for the same fixed block rewards.

- December 2025 – January 2026: Bitcoin price breaks below the psychological support level of $100,000. Institutional miners begin to report significant "curtailment," where they shut down machines during peak energy price hours to save costs.

- February 2026: Bitcoin hits a local bottom near $76,000. Revenue per terahash hits $0.034. Large-scale operators begin announcing the permanent decommissioning of older hardware fleets (S19 and M50 series) and the conversion of site leases to AI firms.

The Hardware Profitability Red Zone

The disparity between different generations of mining hardware has never been more pronounced. At a Bitcoin price of $75,000 and electricity costs of $0.06/kWh, the "break-even" math for mining has turned hostile for the majority of the global fleet.

The Bitmain Antminer S21 XP Hydro, currently the gold standard for efficiency, remains profitable, though its margins have tightened significantly. These units, which produce roughly 473 TH/s with a 5,676-watt draw, see electricity costs consume about 52% of their total revenue. However, for mid-generation rigs like the Antminer S19 XP or the Avalon A1466i, the electricity cost rate sits between 92% and 100%. This means these machines are barely covering their power bills, leaving zero capital for debt service, staff salaries, or facility maintenance.

The situation is dire for older models. Equipment such as the Avalon A1366, Whatsminer M50S, and the venerable Antminer S19 Pro now exhibit electricity cost rates ranging from 109% to 162%. In practical terms, these machines are losing money for every second they remain plugged in. Consequently, vast quantities of this hardware are being liquidated on the secondary market or sent to scrap, contributing to the 12% drop in global hashrate.

The AI Escape Hatch: A Permanent Structural Change

Unlike previous "crypto winters," where miners simply waited for a price recovery to turn their machines back on, the 2026 downturn features a new variable: the insatiable demand for power from the AI sector. Hyperscale AI compute providers are increasingly viewing distressed Bitcoin mining sites not as competitors, but as prime real estate.

Bitcoin mining infrastructure is uniquely suited for AI conversion. Both require high-voltage power interconnections, sophisticated cooling systems, and massive industrial footprints. However, the economic profiles are vastly different. While Bitcoin mining is a volatile, commodity-based business, AI data centers typically operate on long-term, fixed-revenue contracts with tech giants or well-funded startups.

CoreWeave, a former crypto mining firm that pivoted to AI, has become the blueprint for this transition. After securing a $2 billion equity investment from Nvidia, CoreWeave sought to acquire one of the world’s largest miners, Core Scientific, in a multibillion-dollar deal. The objective was clear: to repurpose the miner’s power contracts and physical sites for GPU-based AI workloads.

Similarly, Hut 8, a major Canadian operator, recently finalized a 15-year lease for a 245-megawatt AI data center at its River Bend campus. The deal is valued at approximately $7 billion. For Hut 8 and its shareholders, this represents a shift from the "boom and bust" cycle of Bitcoin rewards to a steady, predictable cash flow. However, for the Bitcoin network, every megawatt of power locked into a 15-year AI contract is a megawatt that will likely never return to hashing. This suggests that the recent decline in hashrate may not be a temporary dip, but a permanent removal of capacity.

Implications for Network Security and Centralization

The exodus of hashrate to the AI sector has profound implications for Bitcoin’s security model. The network’s primary defense against a 51% attack is the sheer cost and scarcity of the hardware and electricity required to overwhelm the honest participants. As the "security budget"—the total value of block rewards and fees—shrinks, the marginal cost of attacking the network also decreases.

Jeff Feng, co-founder of Sei Labs, has characterized this period as the most significant miner capitulation since the 2021 China ban. He notes that the pivot to AI is "amplifying the drawdown" by providing an exit ramp that didn’t exist in previous cycles. If a significant portion of the global hashrate is permanently reallocated to AI, the remaining Bitcoin mining pool becomes smaller and potentially more concentrated.

Centralization is a growing concern among network purists. If only ultra-efficient, multi-billion-dollar corporations can afford to mine at $0.034 per TH/s, the democratic and decentralized nature of block production is at risk. A smaller number of players controlling a larger percentage of the hashrate makes the network more susceptible to regulatory pressure, censorship at the pool level, or coordinated disruptions.

Future Outlook: The Transition to Fee-Based Security

The current crisis may accelerate Bitcoin’s inevitable transition from a subsidy-based security model to a fee-based one. Every four years, the Bitcoin halving reduces the block reward, eventually leaving transaction fees as the sole incentive for miners. The current revenue crash, exacerbated by the AI pivot, is forcing the ecosystem to confront this reality sooner than expected.

Industry analysts suggest three potential paths forward:

- Industrial Consolidation: A period of "quiet consolidation" where the most efficient operators buy out distressed competitors. In this scenario, hashrate grows more slowly, but the network remains stable as difficulty adjusts downward to keep the remaining miners profitable.

- Layer-2 Expansion: To sustain a high security budget without a $150,000 Bitcoin price, the network must generate more transaction fees. This could drive a surge in development for Layer-2 solutions like the Lightning Network or BitVM, which increase the utility and transaction volume of the base layer.

- Institutional Backstops: As Bitcoin becomes a core component of institutional portfolios through ETFs, the entities holding billions of dollars in the asset may eventually need to play a role in ensuring the network’s underlying security. This could involve institutional support for mining infrastructure or a wider acceptance of higher base-layer fees as a necessary "security tax."

At present, the f2pool dashboard serves as a stark reminder of the current state of play. A network with 890 exahashes per second of compute is currently being secured at a rate of roughly 3.5 cents per terahash per day. Whether the market deems this sufficient, or whether the remaining infrastructure continues to bleed into the AI sector, will define the next era of Bitcoin’s existence. For now, the "industrial backbone" of the digital currency is being rewired, and the results will permanently alter the landscape of decentralized finance.