The once-euphoric landscape of Bitcoin mining, characterized by unprecedented profitability just months ago, has dramatically shifted, leaving the industry’s foundational infrastructure facing a brutal reality check. A confluence of a steep price correction, persistently high network difficulty, and escalating energy costs has pushed Bitcoin miners into a deep capitulation phase, forcing many to re-evaluate their operational strategies and, in some cases, pivot entirely to alternative, more lucrative ventures in the artificial intelligence (AI) sector. This unprecedented shift is not merely a cyclical downturn but signals a potentially permanent reallocation of critical compute resources, raising significant questions about the long-term security model of the Bitcoin network.

The Current Crisis: A Deeper Dive into Miner Economics

The industrial backbone of the Bitcoin network, powered by vast arrays of specialized mining hardware, is currently navigating its most challenging period since the 2021 China mining ban. From its peak of over $126,000 just four months prior, Bitcoin’s price has plummeted by more than 38%, now trading near $78,000. While a significant market correction is not uncommon in the volatile cryptocurrency space, the implications for miners are far more severe due to the unique economics of proof-of-work consensus.

Bitcoin’s security mechanism relies on miners expending computational power (hashrate) to solve complex cryptographic puzzles. The first miner to solve a block receives a block subsidy (newly minted Bitcoins) and any transaction fees included in that block. This creates a direct link between Bitcoin’s price and miner profitability: higher prices translate to a more robust "security budget" for the network. Conversely, a sharp decline in price, as witnessed recently, drastically reduces the revenue generated per unit of hashrate.

Compounding this revenue compression is the stubbornly high network difficulty. Difficulty is an automatically adjusting metric that ensures new blocks are found, on average, every ten minutes, regardless of how much total hashrate is deployed. When more miners join the network, difficulty increases, making it harder to find blocks and thus reducing the probability of individual miners earning rewards. Even as some miners have capitulated and exited the network, the difficulty adjustment mechanism lags, meaning remaining miners still face an uphill battle to secure rewards. This creates a vicious cycle: falling prices reduce revenue, but high difficulty means miners must expend the same or more resources to find blocks, further squeezing margins.

Energy costs, always a critical factor for miners, have also continued to rise in many regions, driven by global energy market fluctuations and increased demand from other industries. Bitcoin mining is an energy-intensive process, and power tariffs constitute the largest operational expense for most large-scale facilities. The combination of depressed Bitcoin prices, high network difficulty, and rising energy costs has created a perfect storm, pushing a significant portion of the mining industry into unsustainable operating conditions.

Unpacking the Numbers: Financial Strain and Hashrate Decline

The financial strain on miners is evident across various industry metrics. Analytics firm CryptoQuant recently characterized miners as "extremely underpaid," given the current market conditions. Their profit-and-loss sustainability index, a measure of miner financial health, has slumped to 21 – its lowest reading since late 2024. This figure signals a widespread inability for miners to cover operational costs, let alone generate profit, at current prices and difficulty levels.

The immediate consequence of this economic pressure has been a noticeable decline in network hashrate. Bitcoin’s total hashrate has fallen by approximately 12% since last November, marking the steepest drawdown since the exodus of miners from China in 2021. This decline means the network is currently operating at its weakest computational security level since September 2025. For a network that prides itself on being the most secure computer network globally, this reduction in hashing power represents a critical stress test of its fundamental security model.

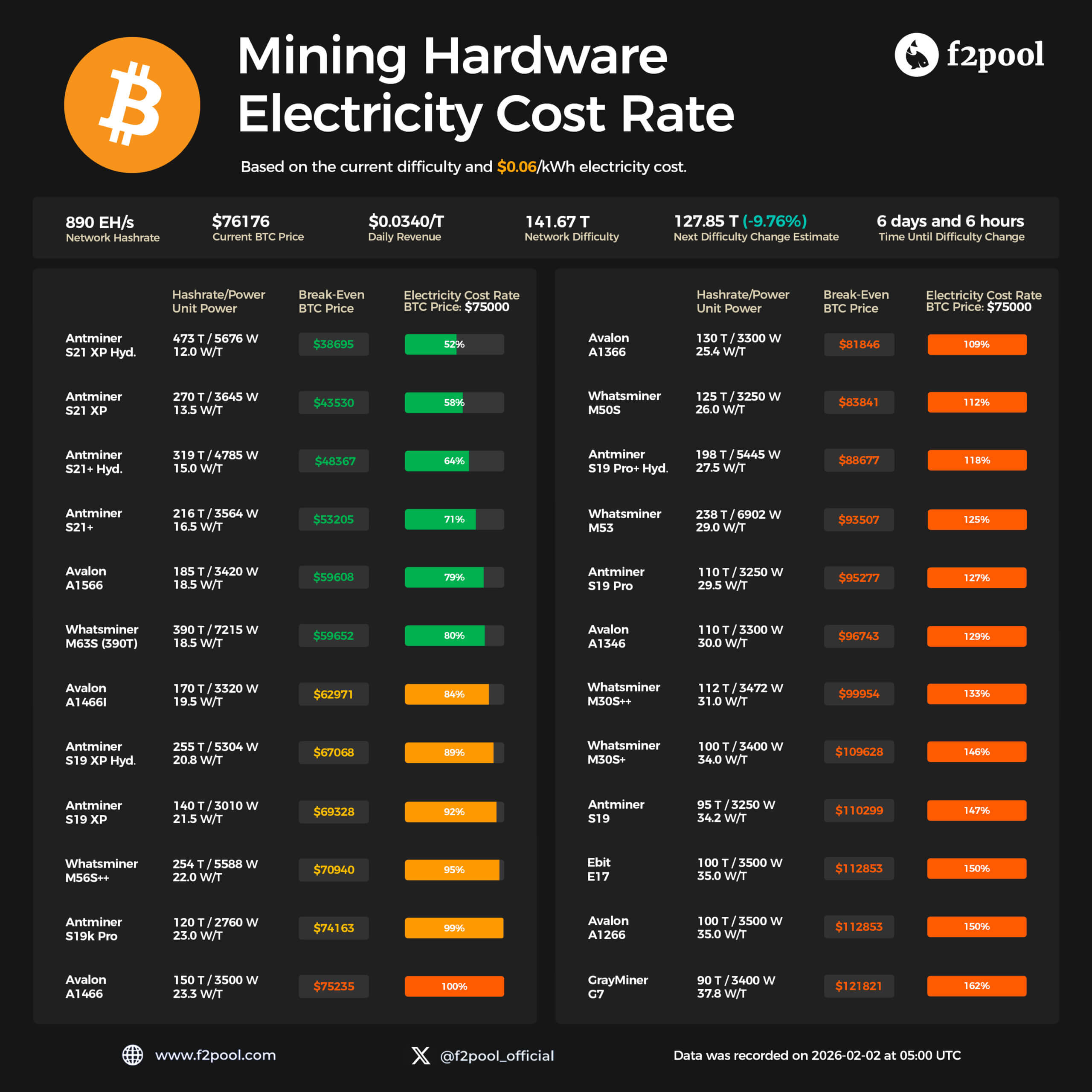

Further illustrating the severity of the revenue compression, figures from the prominent mining pool f2pool paint a stark picture. On its Feb. 2 hardware electricity cost dashboard, f2pool estimated Bitcoin’s price at approximately $76,176, with the network hashrate near 890 exahashes per second (EH/s). At these parameters, the daily revenue for miners paying $0.06 per kilowatt-hour for electricity was a meager $0.034 per terahash.

To provide historical context, Luxor Technology’s Hashrate Index, which tracks spot hashprice (the expected value of 1 TH/s of mining power per day), recorded figures near $39 per petahash per second (PH/s) per day just a few months prior. This figure was already considered lean by historical standards. The f2pool figure of $0.034 per terahash, equivalent to $34 per PH/s, confirms that miners are currently operating at or near a historical floor for profitability.

When these economics are applied to individual mining machines, the reasons for hashrate decline become abundantly clear. For example, even Bitmain’s newest Antminer S21 XP Hydro units, considered highly efficient with roughly 473 TH/s of hashpower and 5,676 watts of draw, face tight margins. At a reference Bitcoin price of $75,000 and a power cost of six cents per kWh, electricity alone accounts for about 52% of their revenue.

The situation deteriorates rapidly for less efficient hardware. Mid-generation rigs, such as an Antminer S19 XP or an Avalon A1466i, exhibit electricity cost rates ranging from approximately 92% to 100% at the same price point and power tariff. This means these machines are barely breaking even on electricity costs before accounting for other significant operational expenses like debt servicing, hosting fees, and general administrative overhead. Older or less efficient models, including the Avalon A1366, Whatsminer M50S, and S19 Pro lines, are operating at significant losses, with electricity cost rates ranging from approximately 109% to 162%. In essence, a vast proportion of the global mining fleet is currently operating at a cash loss, making continued operation financially untenable.

The AI Imperative: A New Suitor for Mining Infrastructure

What distinguishes this current revenue crash from previous crypto winters is the emergence of a new, well-funded demand source for the distressed assets of Bitcoin miners: the artificial intelligence industry. The very infrastructure that underpins Bitcoin mining—reliable power contracts, substantial grid connections, and large-scale data center facilities—is precisely what hyperscale AI compute requires. Crucially, unlike the struggling Bitcoin network, AI infrastructure providers are demonstrating a willingness to pay a premium for these resources.

The shift is epitomized by companies like CoreWeave. Originally a crypto mining operation, CoreWeave successfully pivoted to become a specialist "neocloud" provider for AI workloads. Their strategic reorientation proved highly successful, culminating in a $2 billion equity investment from Nvidia, a key player in AI hardware, to accelerate its data center expansion. In 2025, CoreWeave notably attempted to acquire the large public miner Core Scientific in a multi-billion-dollar deal, explicitly framing the target company’s mining sites and power contracts as prime real estate for powerful Graphics Processing Units (GPUs) rather than Application-Specific Integrated Circuits (ASICs) used for Bitcoin mining.

Other public Bitcoin miners have taken notice and are actively exploring or executing similar pivots towards AI. Canadian operator Hut 8, for instance, recently secured a landmark 15-year, 245-megawatt AI data center lease at its River Bend campus. This deal boasts a stated contract value of approximately $7 billion, effectively locking in long-term, stable economics that stand in stark contrast to the inherent volatility of Bitcoin mining rewards.

For shareholders of these mining companies, such pivots offer a rational and much-needed exit from the bleeding caused by the sustained price downturn. They can exchange the cyclical, highly variable revenues from Bitcoin mining for predictable, contracted cash flows from AI infrastructure, which investors currently value at a significant premium. This strategic realignment provides a lifeline for struggling companies and a pathway to sustained profitability outside the direct fortunes of Bitcoin’s price.

However, for the Bitcoin network itself, this trend presents a more complex and potentially existential question: what are the long-term implications when a fundamental component of its security infrastructure discovers a business model that offers demonstrably higher and more stable compensation?

Security Under Scrutiny: Implications for the Bitcoin Network

Jeff Feng, co-founder of Sei Labs, accurately described the current period as "the biggest Bitcoin miner capitulation since 2021," emphasizing that the reallocation of large mining operations to AI compute is amplifying the overall drawdown in hashrate. A critical distinction from prior cycles is that a portion of this hashpower isn’t merely powering down temporarily, awaiting a price recovery; it is being permanently reallocated.

Once a 245 MW site, like Hut 8’s River Bend campus, is fully re-racked for AI under a long-term lease agreement, that substantial power capacity becomes, in practical terms, unavailable for future Bitcoin hashrate expansion. These facilities, once dedicated to securing the Bitcoin network, are now committed to a different computational purpose.

It is crucial to state that Bitcoin remains incredibly secure in absolute terms. Even after recent declines, the sheer computational power required to mount a successful 51% attack on the network remains immense, costing billions of dollars and requiring significant logistical coordination. The concern, therefore, is less about an immediate collapse and more about the direction and composition of the network’s security over time. A sustained decline in hashrate effectively lowers the marginal cost of attacking the network. With less honest hashing power online, it takes fewer resources—whether through renting capacity or building it—to acquire a disruptive share of the network’s total compute.

Furthermore, this trend narrows the base of stakeholders financially incentivized to defend the chain. If older, higher-cost operators are forced to exit, and only a handful of ultra-efficient miners remain profitable, control over block production could become increasingly centralized. This potential concentration of power, while not immediately threatening, introduces a fragility that can be masked by headline hashrate numbers. A smaller, more centralized group of miners could, in theory, be more susceptible to coercion or regulatory pressure, or even collude to alter network rules, though Bitcoin’s decentralized user base would ultimately resist such attempts.

CryptoQuant’s "extremely underpaid" label, therefore, serves as a crucial forward indicator. It highlights that at today’s block rewards and transaction fees, a significant portion of industrial hashrate is operating on thin or negative margins. This directly impacts the robustness of the network’s "security budget" relative to competing uses of capital and electricity, especially from the burgeoning AI sector.

Historical Precedent and Evolving Landscape

Bitcoin has weathered miner capitulations before, notably during the 2018 bear market and the 2022 crypto winter, as well as the 2021 China mining ban. Each event saw a significant drop in hashrate, followed by a recovery as less efficient miners exited and the market eventually rebound. However, the unique element of the current downturn is the direct competition for infrastructure from the AI industry. Previous capitulations were largely internal to the crypto ecosystem, driven by market cycles alone. Now, miners have a tangible, high-paying alternative for their most valuable assets: power and data center space. This changes the dynamics significantly, potentially making some of the current hashrate decline permanent rather than merely temporary.

Pathways Forward: Bitcoin’s Adaptation Strategies

From this precarious position, the miner squeeze could influence Bitcoin’s evolution in several distinct ways:

-

Quiet Consolidation: This is perhaps the most likely immediate path. As less efficient miners are forced offline, network difficulty will eventually adjust downwards. The most efficient operators, typically those with access to cheap energy, superior hardware, or advanced financial hedging strategies, will capture a larger share of block production. Hashrate might grow more slowly than in previous cycles, but it would remain substantial enough that few outside specialists would notice a critical security degradation. For investors, the primary effect would be continued volatility, as each market drawdown would compress a narrower group of miners, potentially increasing their selling and hedging behavior to manage risk.

-

Accelerated Transition to Fee-Driven Security: Bitcoin’s block subsidy halves approximately every four years, reducing the primary incentive for miners. The long-term vision for Bitcoin’s security is a transition to a model primarily driven by transaction fees. If block subsidies remain insufficient relative to the attractive returns offered by AI, the ecosystem may be forced to accelerate this transition. This could involve greater focus on high-value settlement at the base layer, encouraging more activity on second-layer solutions like the Lightning Network to offload smaller transactions, and a wider acceptance that block space is a scarce resource that should command a higher premium. Higher transaction fees would directly bolster the security budget, making mining more competitive with AI.

-

Explicit External Backstops: A more speculative, yet increasingly discussed, path involves external institutions providing deliberate support for Bitcoin’s security budget. The same institutions that have normalized spot Bitcoin ETFs might eventually view the network’s security budget in a similar light to bank capital ratios – as something that requires strategic attention and, if necessary, direct support. This could manifest in various forms: higher fees for specific transaction classes deemed critical, industry-funded incentives or grants for miners to maintain hashrate in key regions, or even increased scrutiny of AI conversions that materially dent hashrate in strategically important locations. Such measures would represent a more proactive approach to safeguarding network security beyond the implicit incentives of the market.

Crucially, none of these potential outcomes would necessitate a fundamental break with Bitcoin’s core design principles. Instead, they all involve the broader industry, operating within an increasingly crowded and competitive energy market, deciding how much it is prepared to pay to keep computational power dedicated to the Bitcoin network rather than allowing it to migrate to GPU clusters serving the AI boom.

At present, the f2pool dashboard serves as a real-time snapshot of this negotiation. A system with approximately 890 exahashes per second of compute, supported by a Bitcoin price of roughly $76,000, is effectively paying about 3.5 cents per terahash per day for its security. The ultimate trajectory of the Bitcoin mining market, and by extension, the long-term robustness of its security, will hinge on whether future energy investments and computational power allocations are willing to accept this rate or if they will demand something closer to the more lucrative economics currently offered by the insatiable demands of artificial intelligence. The current capitulation is not just a market correction; it is a profound re-evaluation of value and utility for the foundational infrastructure of the decentralized financial world.