The Triple-Layer Reality of All-In Sustaining Costs

To understand why $90,000 has become a psychological and operational flashpoint, one must first dissect the concept of All-In Sustaining Cost (AISC). In the context of Bitcoin mining, AISC is not a static figure but a dynamic threshold that determines the long-term viability of a mining firm. It moves beyond simple electricity costs to include the capital required to maintain a competitive share of the network’s total hashrate.

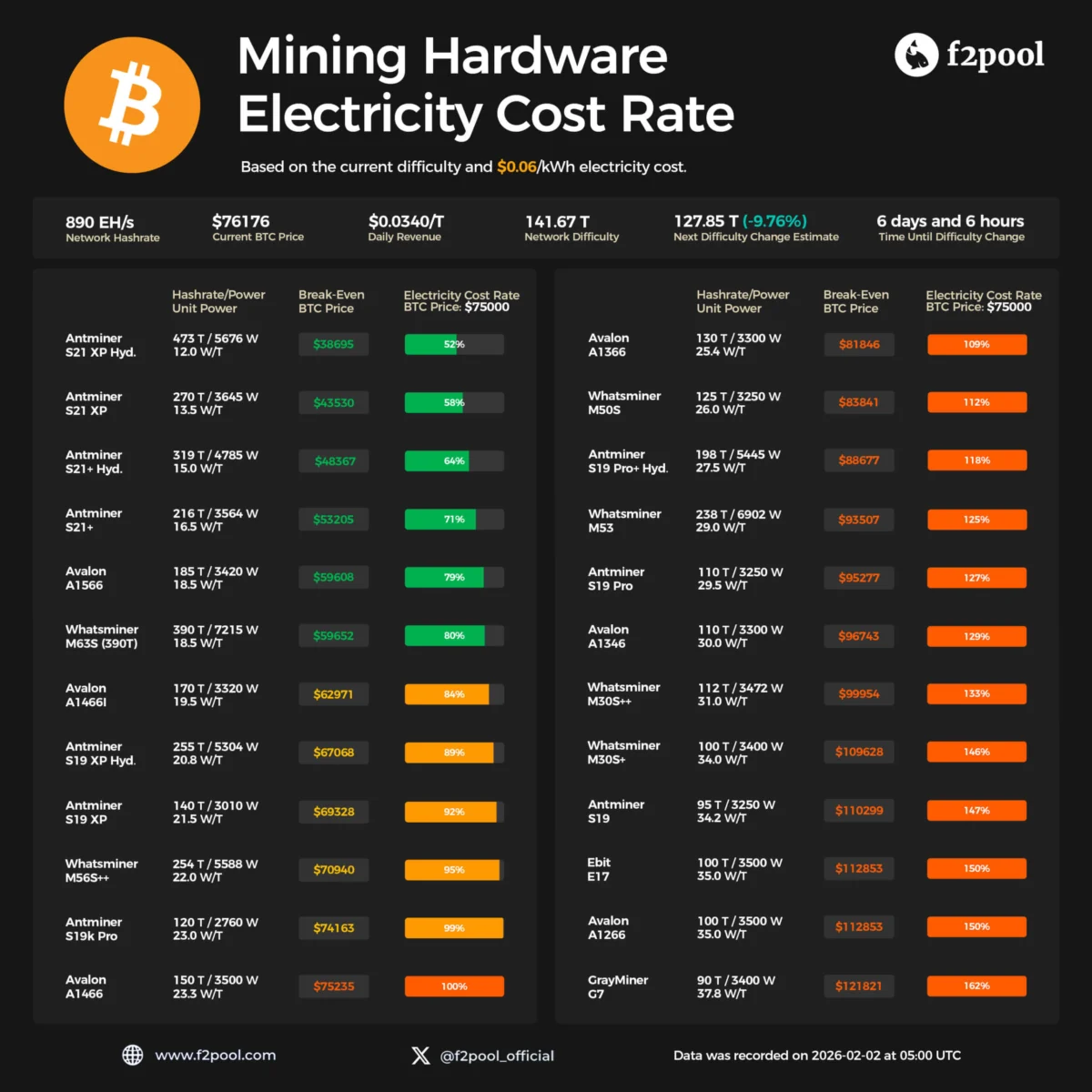

The first layer of this cost structure is direct operating cash expenditure. This is dominated by power purchase agreements (PPAs) and hosting fees. For many industrial miners, electricity is secured through long-term contracts, often ranging from $0.03 to $0.06 per kilowatt-hour. However, as the Bitcoin network difficulty increases—a self-adjusting mechanism that ensures blocks are found every ten minutes—the amount of electricity required to produce a single Bitcoin rises. At current difficulty levels, even the most efficient hardware, such as the Bitmain Antminer S21 series, sees its margins squeezed when the price hovers near $90,000, particularly for operators with less favorable power terms.

The second layer involves sustaining capital expenditure (Capex). Mining hardware is a rapidly depreciating asset. To stay relevant, miners must constantly upgrade their fleets to more efficient machines. If a miner fails to upgrade while the rest of the network does, their "hashprice"—the expected value of 1 TH/s of hashing power per day—diminishes. This creates a treadmill effect where miners must sell a portion of their earned Bitcoin simply to fund the purchase of next-generation hardware.

The third and perhaps most volatile layer is the corporate and financing cost. Since the 2021 bull run, the mining sector has matured from a fragmented collection of private entities into a sophisticated industry dominated by publicly traded giants like Marathon Digital Holdings (MARA), Riot Platforms, and CleanSpark. These companies carry significant debt loads and must manage interest payments, shareholder expectations, and liquidity buffers. When the Bitcoin price sits below the estimated average AISC of $90,000, these public entities are forced to make strategic decisions: do they sell from their "HODL" reserves, or do they dilute equity to stay afloat?

A Chronology of Post-Halving Pressure

The current stress environment is the direct result of a sequence of events beginning with the fourth Bitcoin halving in April 2024. This event programmatically reduced the daily issuance of new Bitcoin from 900 BTC to 450 BTC. Overnight, the primary revenue source for the entire industry was cut in half, while the global hashrate—and thus the competition for those rewards—continued to climb toward all-time highs.

Following the halving, the industry entered a period of consolidation. Throughout the summer of 2024, the "hashrate ribbon"—a technical indicator that tracks the 30-day and 60-day moving averages of the network’s processing power—flipped into inversion territory. Historically, an inversion of these ribbons signals that miners are turning off older, inefficient machines because they are no longer profitable to run.

By the fourth quarter of 2024, the Bitcoin price had surged toward the $90,000 mark, providing temporary relief. However, the network difficulty adjusted upward in tandem with the price, effectively neutralizing much of the gains for the average miner. This has led to the current "bleeding" phase, where the cost of production for many legacy fleets has converged with the market price, leaving little room for error.

The Mathematics of the "Ceiling": Why a Total Collapse is Unlikely

The fear of a miner "dump" is often predicated on the idea that miners hold an infinite supply of Bitcoin that could flood the market at any moment. On-chain data from Glassnode and other analytics firms provides a more grounded perspective. Total miner-held inventories currently sit at approximately 50,000 BTC. While this is a significant sum—valued at roughly $4.5 billion at current prices—it represents a finite and manageable volume when compared to global trading liquidity.

To quantify the potential impact, market analysts utilize a "forced distribution" model. This model examines two primary sources of selling pressure: new daily issuance and existing inventory.

New issuance is the most predictable flow. With 450 BTC generated daily, the maximum "flow selling" that can occur without touching reserves is roughly 13,500 BTC per month. Even in a scenario where every single miner is forced to sell 100% of their daily production to cover costs, the market is only absorbing 450 BTC per day.

When inventory is added to the equation, the numbers remain within historical norms for market absorption. If miners were to liquidate 10% of their 50,000 BTC stockpile over a 60-day period of extreme stress, it would add only 83 BTC per day to the sell side. In a "severe stress" case, where 30% of all miner reserves are liquidated over 90 days, the total selling pressure (issuance plus inventory) would reach approximately 617 BTC per day.

To put these figures in perspective, one must compare them to the flows of Bitcoin Exchange-Traded Funds (ETFs). On a typical high-volume day, Bitcoin ETFs can see inflows or outflows exceeding $500 million. At a $90,000 price point, a $500 million move represents over 5,500 BTC. Thus, even a severe miner capitulation event—contributing roughly 600 BTC per day—represents only about 11% of the volume generated by a single active ETF trading day.

The AI Pivot: A Strategic Buffer for the Mining Industry

A critical factor that the "death spiral" narrative overlooks is the fundamental shift in the business models of major mining firms. Recognizing the volatility of Bitcoin rewards, several of the world’s largest miners have begun diversifying into High-Performance Computing (HPC) and Artificial Intelligence (AI) data centers.

Companies such as Core Scientific and Terawulf have signed multi-billion-dollar contracts to provide power and infrastructure for AI firms. By repurposing their energy-dense facilities to host Nvidia-based GPU clusters rather than Bitcoin ASICs, these companies are creating a non-correlated revenue stream. This "AI pivot" acts as a financial shock absorber; a miner with a steady stream of USD-denominated income from an AI contract is under far less pressure to liquidate their Bitcoin holdings during a market downturn.

This diversification changes the calculus of miner capitulation. In previous cycles, a miner’s only lever was to shut down machines or sell coins. Today, they can shift power allocation between Bitcoin mining and AI workloads based on which is more profitable at the margin. This flexibility effectively raises the "hard ceiling" of the death spiral, as the largest players in the network are no longer solely dependent on the Bitcoin price for survival.

Market Implications and the Role of OTC Desks

Furthermore, the method by which miners sell their Bitcoin is rarely as disruptive as the "dump" narrative suggests. Large-scale miners almost exclusively use Over-the-Counter (OTC) desks to liquidate their holdings. These trades occur outside of the public order books of major exchanges like Coinbase or Binance. While OTC sales eventually impact the market by reducing overall demand from institutional buyers, they do not cause the immediate "waterfall" price drops associated with market-order liquidations.

Professional treasury management has also become the norm. Publicly traded miners often use sophisticated hedging strategies, including collar options and forward sales, to lock in prices for their future production. These financial instruments allow miners to navigate periods where the spot price falls below their AISC without being forced into emergency liquidations.

Conclusion: A Managed Retreat, Not a Rout

The data suggests that while Bitcoin miners are indeed facing significant headwinds at the $90,000 level, the structural risks to the broader market are contained. The combination of programmatically limited issuance, finite inventory, and the diversification of mining revenue into the AI sector has created a buffer that did not exist in previous market cycles.

The "death spiral" math fails to account for the resilience of the difficulty adjustment and the institutionalization of the mining sector. If the price remains below the AISC for an extended period, the least efficient miners will go offline, the network difficulty will drop, and the remaining miners will see their costs decrease and their share of the rewards increase. This self-healing mechanism, central to Satoshi Nakamoto’s original design, ensures that the network remains operational regardless of individual miner profitability.

For investors and market participants, the takeaway is clear: while miner selling may provide a "slow grind" of resistance to upward price movement, the probability of a miner-induced systemic collapse is low. The market has grown too large, and the miners have grown too sophisticated, for the "simple story" of a capitulation dump to dictate the long-term trajectory of Bitcoin.