The Architecture of the Transition: Execution and Consensus

To understand the risks associated with client concentration, one must first grasp the dual-layered architecture that will define Ethereum post-Merge. Unlike the current monolithic structure where a single software client handles both transaction execution and network consensus, the upgraded Ethereum will rely on two distinct types of nodes.

The first is the Execution Layer, which maintains the Ethereum Virtual Machine (EVM). This layer is responsible for processing smart contracts, executing transactions, and maintaining the state of the blockchain. It is essentially the "business logic" of the network. The second is the Consensus Layer, often referred to as the Beacon Chain, which has been running in parallel with the mainnet since December 2020. The Consensus Layer is responsible for the PoS logic, where validators propose and attest to new blocks based on their staked ETH.

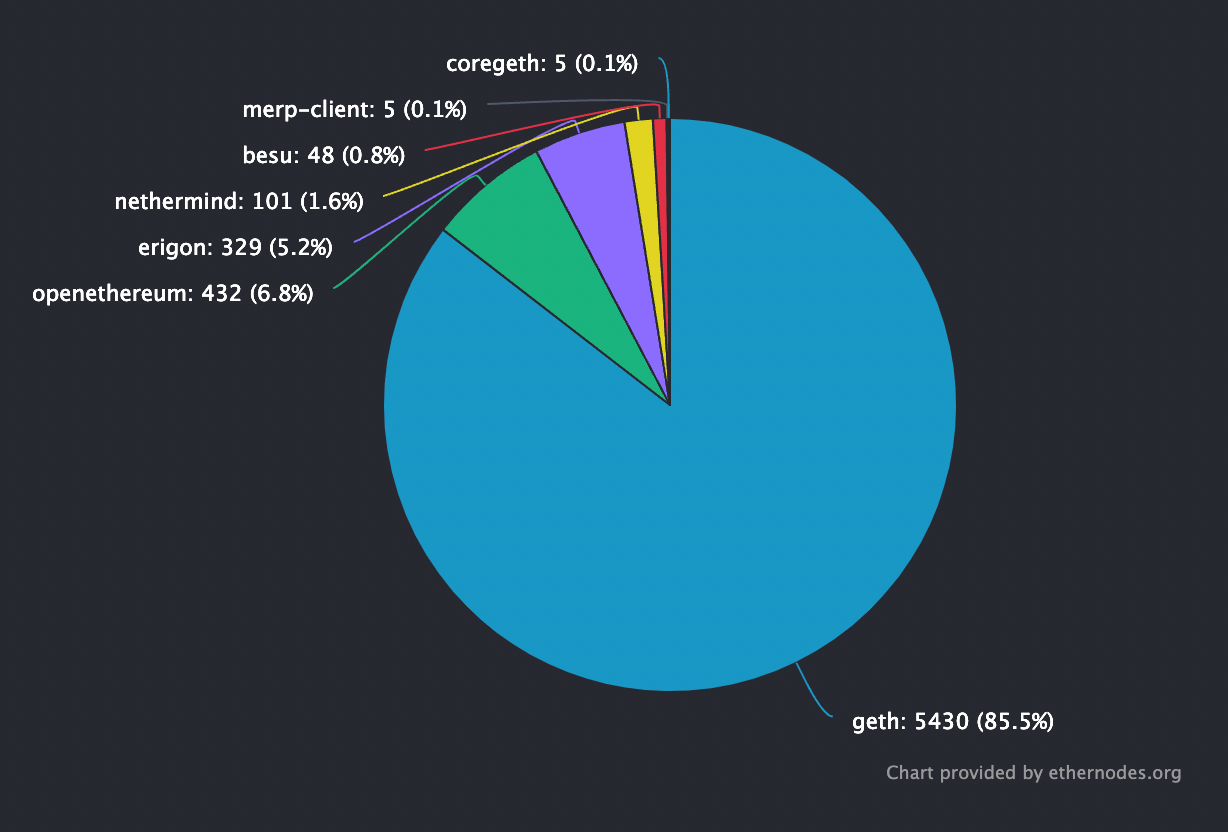

Post-Merge, these two layers will communicate via the Engine API. An execution client will bundle transactions and pass them to a consensus client, which then coordinates with the rest of the network to achieve finality. While the execution layer has historically been dominated by Geth (Go-Ethereum), which currently commands an 85% market share, the consensus layer is where the primary security concern lies. Because consensus clients are responsible for the very integrity of the ledger’s history, a bug in a majority client could lead to catastrophic network failure.

The Mathematics of Consensus Risk

The security of a Proof-of-Stake network is predicated on Byzantine Fault Tolerance (BFT) principles. In Ethereum’s PoS implementation, the safety of the network is tied to specific mathematical thresholds:

- The 33% Threshold: If a client with more than one-third of the total stake goes offline or experiences a bug that prevents it from validating, the network can no longer reach "finality." While the chain continues to grow, transactions are not considered irreversible until the issue is resolved.

- The 50% Threshold: If a client used by more than half of the validators has a bug that leads to an invalid chain, that chain could potentially grow longer than the valid one, causing significant disruption and requiring manual intervention to fix.

- The 66% (Supermajority) Threshold: This is the "critical failure" zone. If a client with more than two-thirds of the stake has a consensus bug, it can finalize an incorrect or "buggy" state. In this scenario, the network’s built-in safeguards would fail to distinguish between the correct protocol and the bug. The buggy chain becomes the "official" chain in the eyes of the majority, potentially leading to a permanent chain split or the total loss of funds for those on the minority, non-buggy clients.

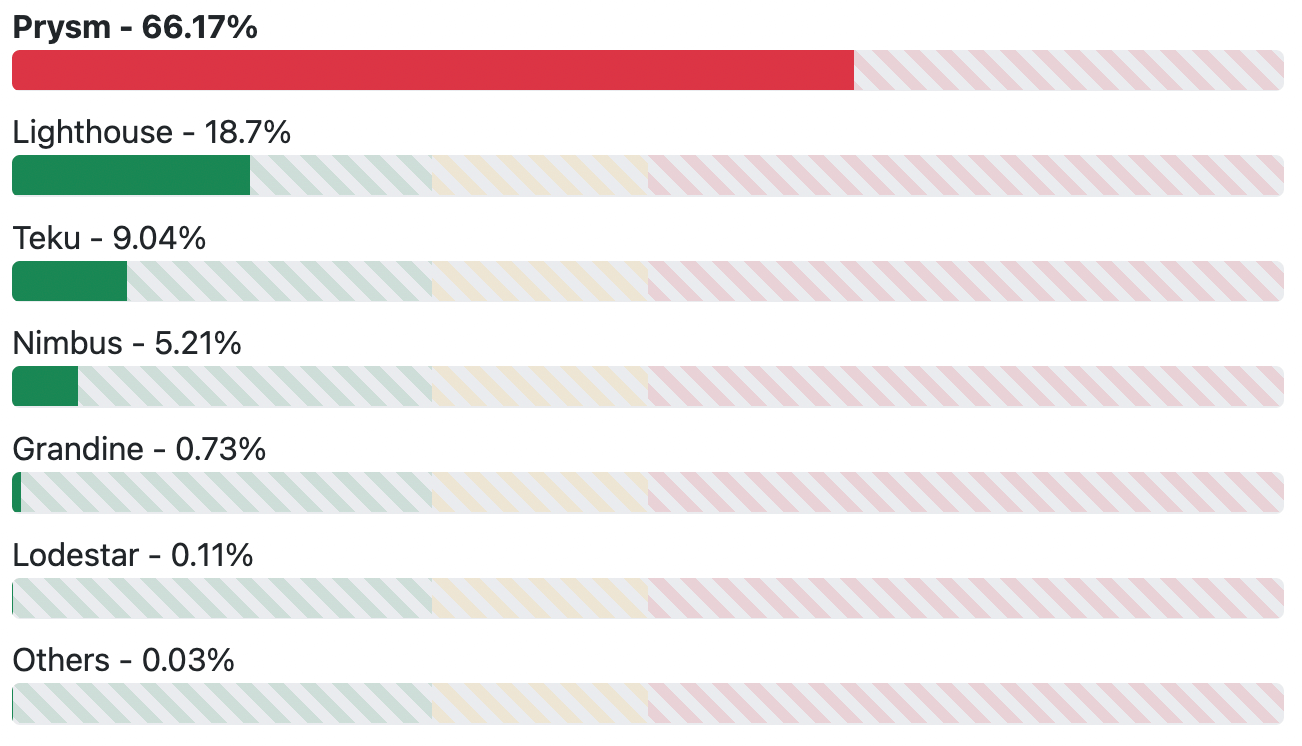

Currently, Prysmatic Labs’ Prysm client sits at or near this 66% threshold. If a consensus-breaking bug were to appear in Prysm today, the Ethereum network could finalize an invalid state, effectively forcing the community to choose between following a broken chain or performing a controversial "hard fork" to revert the damage.

A Chronology of Ethereum’s Path to The Merge

The road to the current dilemma began years ago, as Ethereum developers sought to move away from the energy-intensive PoW model used by Bitcoin.

- July 2015: Ethereum launches with a PoW consensus.

- 2018–2019: The "Casper" and "Sharding" specifications evolve into the multi-phase Ethereum 2.0 roadmap.

- December 2020: The Beacon Chain (Phase 0) launches, allowing users to stake 32 ETH to become validators. This marks the beginning of the parallel Consensus Layer.

- 2021: The "London" Hard Fork introduces EIP-1559, altering the fee market and signaling the final stages of the PoW era.

- Early 2022: Testnets like Kintsugi and Kiln successfully simulate The Merge, but data reveals a heavy reliance on the Prysm client among institutional stakers.

- Mid-2022 (Projected): The Merge is scheduled to occur, deprecating PoW mining entirely.

Throughout this timeline, the Ethereum Foundation has championed the idea of "multi-client philosophy." This is a stark contrast to Bitcoin, which relies almost exclusively on Bitcoin Core. The rationale is that Ethereum’s complexity—handling thousands of decentralized applications and billions in DeFi assets—makes it more prone to bugs than Bitcoin’s simpler value-transfer protocol. Multiple independent implementations (Prysm, Lighthouse, Teku, Nimbus, and Lodestar) were intended to ensure that a bug in one would not take down the whole system. However, the market has not naturally distributed itself across these options.

Analyzing Prysm’s Dominance: The First-Mover Advantage

The reasons for Prysm’s 66% market share are largely pragmatic rather than ideological. Speaking to industry analysts, Marius van der Wijden, a prominent Ethereum core developer, noted that Prysm benefited immensely from being the first viable prototype.

"Prysm was the first implementation that people could actually test," van der Wijden explained. This allowed the team at Prysmatic Labs to build superior documentation, a robust Web UI, and a suite of tools that made it the default choice for early adopters. Furthermore, Prysm is written in Go (Golang), the same language as Geth. For the existing pool of Ethereum developers and node operators, this made the transition to the consensus layer feel familiar and auditable.

Another critical factor was the inclusion of "remote signer" support. Large-scale institutional stakers require the ability to keep their private keys in secure, isolated environments (such as Hardware Security Modules) while the validator software runs on a separate server. Prysm offered this feature early, making it the only viable choice for major exchanges during the initial staking rollout in late 2020.

The Role of Centralized Exchanges and Staking Providers

Data suggests that the client diversity issue is not driven by individual "home stakers" but by massive, centralized entities. According to recent network scans, a handful of providers contribute the bulk of the Prysm dominance:

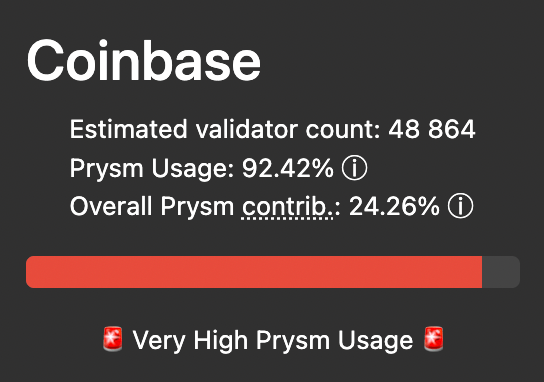

- Coinbase: With nearly 49,000 validators (approx. 17.5% of the network), Coinbase runs over 92% of its infrastructure on Prysm.

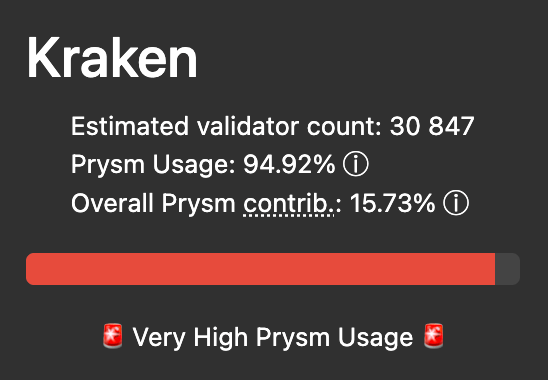

- Kraken: Operating roughly 11% of the network’s validators, Kraken maintains a 94.9% reliance on Prysm.

- Binance: Holding nearly 9% of the validator share, Binance utilizes Prysm for roughly 76.6% of its operations.

- Lido Finance: As a decentralized liquid staking protocol, Lido is slightly better but still utilizes Prysm for 42.8% of its validators.

When questioned about this concentration, Coinbase Cloud pointed to the security features that were unique to Prysm at launch. "Remote signers allow validators to generate and store keys in isolated environments… which greatly increases the security," the company stated in a recent technical update. While they have since begun integrating the Lighthouse client, the inertia of existing infrastructure makes a rapid shift difficult.

Kraken’s Senior Product Manager, Brian Hoffman, echoed this sentiment, stating that while Prysm was chosen for its "maturity and stability," the exchange is now working with the Ethereum Foundation to migrate some validators to Teku to mitigate systemic risk.

Broader Implications and the "No Bailout" Policy

The Ethereum developer community has taken a hardline stance on this issue to incentivize change. Core developers have repeatedly warned that if a supermajority client experiences a consensus bug that leads to financial loss, there will be no protocol-level "bailout" for those validators.

If a majority client forks away from the correct chain, the network’s "Inactivity Leak" mechanism would begin to strip ETH from those validators until their collective stake drops below the 33% threshold, allowing the remaining minority clients to finalize the correct chain. This means that running the most popular client is actually the riskiest financial move for a staker, as they face the highest potential for "slashing" and penalties in the event of a bug.

Despite these risks, the consensus among core developers like Marius van der Wijden remains that The Merge is safe to pursue. "The chances of a consensus failure happening are very small," he noted, citing the rigorous "fuzzing" and testing infrastructure that constantly checks for discrepancies between different clients.

Conclusion: The Path Forward

The Ethereum Merge represents a landmark event in the history of distributed systems. While the dominance of the Prysm client presents a non-zero risk of a "game over" scenario, the ongoing efforts by exchanges to diversify their stacks and the emergence of decentralized alternatives like Rocket Pool (which uses only 10% Prysm) suggest the trend is moving toward a safer equilibrium.

As the transition approaches, the responsibility for Ethereum’s resilience rests not just with the protocol developers, but with the institutional entities that command the network’s staking power. The coming months will determine whether the community can proactively solve the diversity crisis or if the network will have to rely on its mathematical safeguards to weather a potential storm. For now, the "engine replacement" continues, with the hope that the multiple redundant systems designed by the Ethereum Foundation will be enough to keep the plane in the air.