SoFi Technologies, a prominent financial services company, has announced a pivotal partnership with global payments giant Mastercard, enabling the settlement of transactions using its dollar-backed stablecoin, SoFiUSD, across Mastercard’s extensive global payments network. This groundbreaking collaboration positions SoFiUSD as a key enabler for issuers and acquirers seeking to settle card transactions using a regulated, bank-issued digital dollar, marking a significant step towards integrating blockchain technology into mainstream financial operations.

The core of this strategic alliance lies in SoFi Bank N.A.’s intention to settle its own Mastercard credit and debit transactions directly in SoFiUSD. Beyond internal operations, SoFi’s advanced payments technology platform, Galileo, will extend this capability to its client banks and card issuers. This means a broad spectrum of financial institutions will gain the option to leverage SoFiUSD for transaction settlement across Mastercard’s vast network, streamlining processes and potentially reducing costs associated with traditional fiat currency settlements.

This initiative is particularly notable because SoFiUSD holds the distinction of being the first stablecoin issued by a U.S. nationally chartered and insured deposit bank on a public, permissionless blockchain. This unique regulatory backing, combined with the technological innovation of blockchain, promises to revolutionize settlement processes by allowing transactions to be finalized 24 hours a day, seven days a week, a stark contrast to the often restrictive operating hours of conventional banking systems. The constant availability of settlement provides unprecedented efficiency and liquidity, especially for cross-border transactions.

The Evolution of Stablecoins and SoFiUSD’s Unique Position

Stablecoins are a class of cryptocurrencies designed to minimize price volatility by pegging their value to a stable asset, most commonly the U.S. dollar. They aim to combine the speed and transparency of blockchain technology with the stability of fiat currencies, making them ideal candidates for payments and settlements. SoFiUSD, launched in December, is issued by SoFi Bank, an institution regulated by the Office of the Comptroller of the Currency (OCC) and insured by the Federal Deposit Insurance Corporation (FDIC). This regulatory oversight is a critical differentiator, instilling a higher degree of trust and confidence compared to many other stablecoins issued by non-bank entities. The stablecoin is backed 1:1 by cash reserves, ensuring its parity with the U.S. dollar, a crucial factor for its acceptance in a network as vast as Mastercard’s.

The decision to issue SoFiUSD on a public, permissionless blockchain is also a strategic one. While the specific blockchain was not disclosed in the initial announcement, using such a network enhances transparency, immutability, and accessibility, fundamental tenets of blockchain technology. This allows for open verification of transactions and balances, fostering trust among participants. Mastercard’s broader "Multi-Token Network" (MTN) is designed to be a flexible framework capable of supporting various digital assets, including fiat currencies, tokenized deposits, and other digital assets alongside stablecoins like SoFiUSD. This infrastructure prepares Mastercard for a future where diverse digital assets coexist and interoperate within its payment ecosystem.

Mastercard’s Strategic Embrace of Digital Assets

Mastercard’s partnership with SoFi is not an isolated event but rather a continuation of its deliberate and expanding strategy to integrate digital assets into its global payments infrastructure. The company has been increasingly active in the stablecoin space, recognizing their potential to enhance efficiency and reduce friction in payments.

A significant precursor to this latest development occurred in November when Mastercard partnered with Thunes, a global cross-border payments network. This collaboration aimed to expand stablecoin wallet payouts through Mastercard Move, a service designed to facilitate near real-time transfers. By enabling payouts to regulated stablecoin wallets via Thunes’ Direct Global Network, Mastercard demonstrated its commitment to bridging the gap between traditional finance and the burgeoning digital asset economy. This move highlighted Mastercard’s vision of leveraging stablecoins to make cross-border remittances faster, more affordable, and more accessible, particularly for underserved populations.

Mastercard’s broader strategy involves exploring a multitude of use cases for stablecoins beyond just settlement. The companies stated they would investigate additional applications such as cross-border remittances, which traditionally suffer from high fees and slow processing times. Business-to-business (B2B) transfers also stand to benefit significantly from stablecoin integration, offering improved liquidity management and faster payment cycles for enterprises. Programmable treasury applications, allowing for automated and conditional payments, represent another frontier for efficiency gains. Furthermore, the development of stablecoin-enabled card programs could seamlessly connect the digital asset world with everyday spending, subject, of course, to evolving regulatory requirements and Mastercard network rules. These potential applications underscore a comprehensive vision for stablecoins as foundational elements of a modernized payment system.

A Competitive Landscape: Visa’s Parallel Path to Digital Dollar Integration

Mastercard is not alone in its aggressive pursuit of stablecoin integration; its primary rival, Visa, has also been making significant strides in widening its use of digital dollars across settlement and payout services. This parallel development among the world’s two largest payment processors signals a fundamental shift in the global financial landscape, indicating that stablecoins are increasingly viewed as a viable and valuable component of future payment infrastructures.

In September, Visa embarked on its own pilot program to test stablecoin-based cross-border settlement. This initiative, part of its Visa Direct service, allowed select banks to pre-fund international transfers using Circle’s USDC (USD Coin) and EURC (Euro Coin). USDC, a widely used stablecoin, provides a robust and liquid option for these trials. This pilot demonstrated Visa’s commitment to exploring how blockchain-based digital assets could streamline international money movement. Building on this success, Visa later expanded its support to four stablecoins across four different blockchains, showcasing a versatile and interoperable approach. This expansion also included the capability for conversion into more than 25 fiat currencies, significantly enhancing the global reach and utility of stablecoin-powered transactions.

Visa’s innovation extends beyond settlement to direct stablecoin payouts. In November, the company introduced a Visa Direct pilot enabling businesses to send funds directly to recipients’ stablecoin wallets. This groundbreaking service provides freelancers, gig workers, and marketplaces with the option to receive USD-backed tokens instead of traditional bank transfers. For individuals engaged in the global gig economy, this means faster access to funds, potentially lower transaction fees, and greater flexibility in managing their earnings. The expansion of this program overseas further solidified Visa’s commitment to global digital asset integration. Last month, Netherlands-based Quantoz Payments became a principal Visa member, granting it the ability to issue Visa-branded debit cards backed by its regulated e-money tokens. This move allows Quantoz to support fintechs offering stablecoin-linked products across Europe, effectively bridging the gap between digital assets and traditional card spending for European consumers and businesses.

The Broader Implications for Finance and the Global Economy

The convergence of major payment networks like Mastercard and Visa with regulated stablecoins carries profound implications for the future of finance. The most immediate benefit is the promise of enhanced efficiency and speed in financial transactions. The 24/7 settlement capability offered by stablecoins eliminates the traditional banking hours and weekend delays, which are particularly cumbersome for international transactions. This perpetual operation means businesses can manage their liquidity more effectively, reduce working capital requirements, and accelerate supply chain payments. For consumers, it translates to faster remittances and quicker access to funds.

Furthermore, the adoption of stablecoins for settlement has the potential to significantly reduce transaction costs. Traditional cross-border payments often involve multiple intermediaries, each adding fees and conversion costs. Stablecoins, leveraging blockchain technology, can bypass some of these layers, leading to more direct and cost-effective transfers. This is especially impactful for emerging markets and individuals who rely heavily on remittances, where even small percentage reductions in fees can make a substantial difference.

The exploration of additional use cases—such as programmable treasury applications, cross-border remittances, and B2B transfers—highlights the transformative potential of stablecoins. Programmable money can enable automated payroll, instant vendor payments upon delivery verification, or even smart contracts that release funds based on predefined conditions. This level of automation and precision is currently difficult to achieve with traditional fiat systems. Stablecoin-enabled card programs represent the ultimate bridge, allowing users to spend their digital dollars in the physical world wherever traditional cards are accepted, seamlessly integrating the digital and physical economies.

The regulatory environment remains a critical factor. The fact that SoFiUSD is issued by an OCC-regulated and FDIC-insured bank is a significant advantage, addressing concerns about consumer protection, financial stability, and anti-money laundering (AML) compliance that have plagued the broader cryptocurrency market. This regulatory clarity is likely to encourage wider adoption by institutions and enterprises that require robust compliance frameworks. As more regulated entities enter the stablecoin space, it builds a precedent for future legislative frameworks, potentially leading to more harmonized global regulations for digital assets.

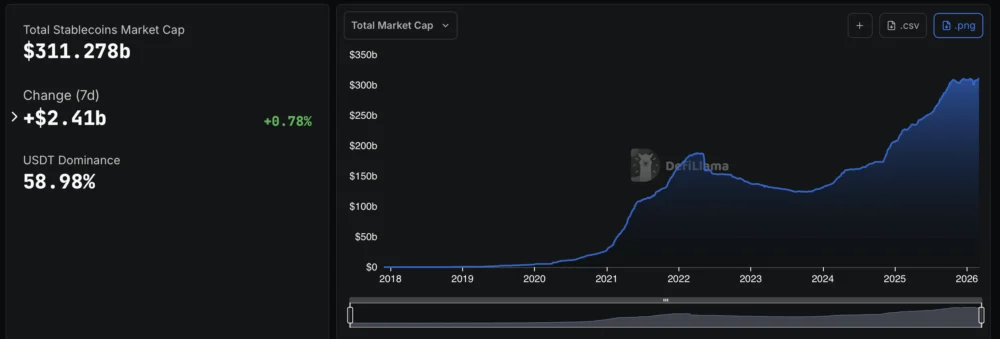

The stablecoin market itself reflects this growing momentum. At the time of writing, the total stablecoin market capitalization stood at approximately $311.28 billion, according to DefiLlama data. Transaction volumes have shown explosive growth, reaching a record $969.9 billion in August 2025, with forecasts predicting volumes nearing $1 trillion monthly by December 2026, as reported by CoinLedger in September. These figures underscore the rapidly increasing utility and adoption of stablecoins as a core component of the digital economy.

This partnership between SoFi and Mastercard, alongside Visa’s parallel efforts, marks a significant milestone in the convergence of traditional finance, fintech innovation, and blockchain technology. It signals a future where digital dollars, underpinned by robust regulatory frameworks and integrated into global payment networks, play an increasingly central role in daily commerce, cross-border trade, and financial services worldwide. The race to build the most efficient, secure, and accessible digital payment infrastructure is on, and stablecoins are undeniably at the heart of this transformation.