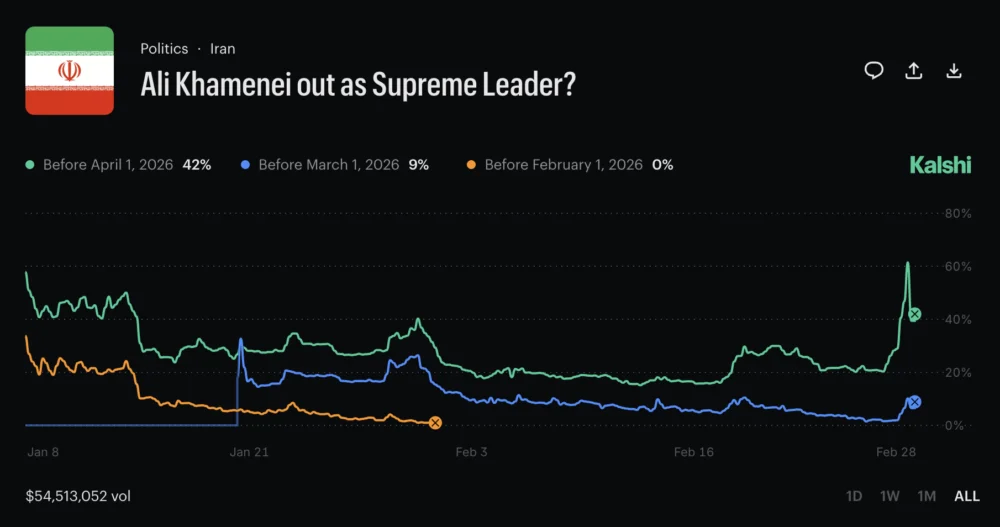

Tarek Mansour, co-founder of the U.S.-regulated prediction market Kalshi, has addressed a wave of controversy stemming from the platform’s decision to void certain positions opened after the widely reported death of Iran’s Supreme Leader, Ayatollah Ali Khamenei. The move, intended to uphold Kalshi’s long-standing policy against markets directly tied to death, has nevertheless ignited significant user backlash and reignited discussions about the ethical complexities and potential for insider trading within the burgeoning prediction market industry.

The "Ali Khamenei out as Supreme Leader" market on Kalshi had been active, allowing users to speculate on the duration of his tenure. However, following initial reports by Iranian state media early on a Sunday morning regarding Khamenei’s passing—reports that notably surfaced in the wake of unverified claims of an attack by Israel and the United States a day prior—Kalshi promptly intervened. Mansour clarified the platform’s stance in a public statement on X, emphasizing, "We don’t list markets directly tied to death. When there are markets where potential outcomes involve death, we design the rules to prevent people from profiting from death. That is what we did here." This statement aimed to articulate the underlying ethical framework guiding Kalshi’s actions, asserting a commitment to preventing exploitation of sensitive real-world events for financial gain.

Context: The "Ali Khamenei Out" Market and Prediction Market Dynamics

Prediction markets, like Kalshi, allow users to trade on the outcome of future events, ranging from economic indicators and political elections to scientific breakthroughs. Participants buy and sell contracts representing potential outcomes, with prices fluctuating based on collective belief, ultimately settling at $1 for the correct outcome and $0 for incorrect ones. Kalshi, notably, is regulated by the Commodity Futures Trading Commission (CFTC) in the United States, allowing it to offer event contracts on a variety of topics, excluding political elections and certain other sensitive areas. The "Ali Khamenei out as Supreme Leader" market was framed around the event of his departure from leadership, without explicitly mentioning death as the sole trigger, aligning with their regulatory compliance and internal policies.

Ayatollah Ali Khamenei, born in 1939, has been Iran’s Supreme Leader since 1989, succeeding Ayatollah Ruhollah Khomeini. His long tenure has seen him wield immense power, serving as the ultimate authority on major state policies and religious matters. His health has been a subject of frequent speculation over the years, making his potential departure a significant geopolitical event. Such events naturally attract the attention of prediction markets, which aim to aggregate information and provide real-time probabilities for future occurrences. The market on Kalshi provided an outlet for individuals to express their collective assessment of the likelihood of a leadership change in Iran.

The Incident: Reported Death and Kalshi’s Immediate Response

The catalyst for Kalshi’s contentious decision was the flurry of reports on the alleged death of Ayatollah Ali Khamenei. While initial claims by Iranian state media hinted at an Israeli-U.S. attack preceding his demise—a claim that quickly met with skepticism and was not independently verified by international outlets, and later implicitly walked back by Iranian media focusing on health issues—the critical piece of information for the prediction market was the confirmation of his passing itself. The news, regardless of its immediate context or cause, triggered the pre-defined rules of the "death carveout" within the market’s terms.

Upon confirmation, Kalshi swiftly moved to implement its policy. A spokesperson for Kalshi reiterated to Cointelegraph that the platform’s policy against "death markets" is both clear and deeply entrenched in its operational guidelines. The platform publicly re-emphasized this policy on Saturday, even as Mansour highlighted that the specific stipulations for such a "death carveout" were explicitly detailed in the market’s rules from its inception. This transparency, Kalshi argues, should have preempted any surprise or dissatisfaction among traders.

Kalshi’s Policy on "Death Markets": Rationale and Enforcement

Kalshi’s proactive stance against "death markets" is rooted in a combination of ethical considerations, regulatory prudence, and a desire to maintain the integrity of its platform. The company’s philosophy dictates that profiting directly from human mortality, especially when such events can be unpredictable and carry significant human weight, crosses an ethical line. This policy aims to prevent a scenario where individuals might be incentivized, even indirectly, by tragedy.

The specific "death carveout" clause within the market rules ensures that if the outcome of a market is influenced by the death of an individual, any positions opened after the confirmation of that death are considered invalid or subject to specific adjustments. This mechanism is designed to mitigate the perception, and indeed the reality, of individuals attempting to "gamble" on death itself or to exploit real-time, sensitive information for profit. It also helps Kalshi avoid the negative public perception that could arise from being seen as facilitating such trading. For a CFTC-regulated entity, maintaining such ethical boundaries is not just good practice but also a crucial aspect of managing regulatory risk and public trust. The platform explicitly stated that this policy is "clear and long-standing," suggesting it’s not a reactive measure but a foundational principle.

User Backlash and Rebuttals: The Conflict Between Rules and Perceived Profit

Despite Kalshi’s assertions of clear rules and ethical motivations, the decision to void positions was met with considerable backlash from its user base. Online forums and social media platforms, particularly X (formerly Twitter), became arenas for disgruntled traders to express their frustration. Accusations ranged from "curtailing user profits" to a perceived lack of transparency or inconsistent application of rules. Some users argued that if the market was open, all trades made within its parameters should be honored, irrespective of the underlying event’s sensitive nature. They felt that their calculated risks, even if taken after the news broke, were legitimate and that Kalshi was retroactively altering the terms of engagement.

Tarek Mansour, in his defense, reiterated that the death carveout stipulations were "clearly stated in the rules for the market." This highlights a perennial tension in prediction markets: the balance between offering an open platform for speculation and enforcing stringent ethical and operational guidelines, especially when dealing with high-stakes geopolitical events. While Kalshi’s intention was to prevent profiting from death, some users interpreted the action as an arbitrary interference with their trading strategies, leading to a loss of potential gains. This conflict underscores the challenge of communicating complex policy nuances to a diverse user base, particularly when financial outcomes are at stake.

Financial Implications and Reimbursement Structure

To mitigate the financial impact on its users and demonstrate fairness, Kalshi outlined a specific reimbursement structure. The platform committed to reimbursing all fees associated with the "Ali Khamenei out as Supreme Leader" market, irrespective of individual trading outcomes. This measure aims to offset any transaction costs incurred by traders.

Furthermore, Kalshi differentiated between two categories of traders:

- Positions opened before Khamenei’s death: Traders who held open positions before the confirmation of his death were to be paid out according to the "last-traded price before his death." This ensures that those who made their bets based on pre-existing information and market dynamics were not penalized by the subsequent event or policy intervention. It acknowledges the validity of their initial positions.

- Positions opened after Khamenei’s death: Users who opened positions after the reported death of Khamenei were reimbursed the difference between the higher price they paid for entry and the last traded price. This nuanced approach aims to prevent profit from the sensitive event itself while also ensuring that these traders are not left entirely out of pocket. It attempts to unwind the "death-related" portion of their trade without fully confiscating their principal. This particular aspect of the reimbursement strategy directly reflects the "no profiting from death" policy.

Broader Implications: Ethical Debates in Prediction Markets

The Kalshi incident is not an isolated event but rather a symptom of the ongoing ethical and operational challenges faced by prediction market platforms. The ability to trade on outcomes of real-world events, particularly those with significant human impact or geopolitical sensitivity, inevitably raises profound ethical questions. Is it appropriate to monetize tragedy? Where do platforms draw the line between legitimate speculation and unethical opportunism?

The core debate revolves around the moral hazard associated with such markets. While proponents argue that prediction markets can aggregate valuable information and even serve as an early warning system for certain events, critics contend that they risk commodifying human suffering and incentivizing actions that might otherwise be considered morally reprehensible. Kalshi’s explicit "no death markets" policy is a direct attempt to navigate this ethical minefield, but as the user backlash demonstrates, even well-intentioned policies can generate controversy when they intersect with financial expectations. The incident serves as a stark reminder that as prediction markets grow in popularity and influence, their ethical frameworks will come under increasing scrutiny.

The Shadow of Insider Trading: Past Incidents and Ongoing Concerns

Adding another layer of complexity to the discussion surrounding prediction markets is the persistent shadow of insider trading. The Kalshi incident, while primarily about the "death market" policy, occurs within a broader context where suspicions of insider trading activity on rival platforms have repeatedly surfaced amid geopolitical tensions.

A notable incident occurred in February when six traders on the rival prediction market Polymarket reportedly netted approximately $1 million by betting on a U.S. strike on Iran before the end of the month. According to Bloomberg reports, all six wallets involved were newly created in February, predominantly focused on markets related to a potential strike on Iran, with some positions being filled mere hours before the first explosions were heard over the Iranian capital of Tehran. These highly correlated and timely trades raised significant red flags among on-chain investigators and analysts, fueling suspicions of insider trading or privileged information being exploited.

Another compelling case emerged in January when then-U.S. President Donald Trump announced the arrest of an individual who had leaked information tied to the raid and capture of former Venezuelan President Nicolás Maduro. This revelation quickly fueled speculation from on-chain analysis platforms like Lookonchain, suggesting a potential link between the arrested leaker and winning bets placed on Polymarket shortly before the U.S. raid in Caracas. The precise timing of these bets, preceding a highly sensitive and confidential operation, strongly hinted at the misuse of non-public information for financial gain.

These instances, occurring on different platforms but within the same ecosystem of event-based speculation, highlight a critical vulnerability for prediction markets. While these platforms often champion transparency through public ledger technology (in the case of decentralized markets) and robust rule sets (for regulated ones like Kalshi), the potential for individuals with privileged access to sensitive information to exploit these markets remains a significant concern. Insider trading not only undermines the fairness and integrity of the markets but also poses serious legal and reputational risks to the platforms themselves. It underscores the difficulty of completely insulating these markets from external information advantages, particularly in areas of national security and high-stakes geopolitics.

Regulatory Landscape and Future of Prediction Markets

The ongoing controversies surrounding ethical boundaries and insider trading on prediction markets like Kalshi and Polymarket inevitably draw attention to the regulatory landscape. Kalshi, as a CFTC-regulated entity, operates under specific guidelines that mandate transparency, market integrity, and consumer protection. Their "no death markets" policy can be seen as a proactive measure to stay within regulatory comfort zones and uphold ethical standards. However, the incidents on unregulated or less-regulated platforms like Polymarket highlight a broader challenge.

The future of prediction markets will likely be shaped by how effectively platforms can address these concerns. This includes:

- Enhanced Policy Clarity: While Kalshi states its policies are clear, the backlash suggests a need for even more prominent communication and user education regarding sensitive "carveouts."

- Robust Surveillance and Enforcement: Proactive monitoring for suspicious trading patterns, similar to traditional financial markets, is crucial to combat insider trading.

- Ethical Framework Development: A more comprehensive industry-wide discussion on what constitutes ethical trading in prediction markets, especially concerning human life and geopolitical stability, may be necessary.

- Regulatory Evolution: As these markets mature, regulators may impose stricter rules, potentially affecting the types of events that can be traded and the methods of operation. The line between harmless speculation and problematic activity is continuously being drawn, and these incidents actively contribute to that evolving definition.

The Kalshi incident, therefore, is more than just a dispute over voided trades; it is a microcosm of the larger challenges facing the prediction market industry. It forces a critical examination of how these platforms can balance the desire for open, efficient markets with the imperative to operate ethically, prevent exploitation, and maintain public trust in an increasingly interconnected and information-driven world. The balancing act is delicate, and the consequences of missteps can be significant for both the platforms and their users.