Cross-border payments, the essential mechanism enabling the movement of money between different countries, constitute a critical function for global commerce, financial markets, and remittances, collectively accounting for a global payment market estimated at approximately $1 quadrillion annually. Despite its immense value, this intricate system, traditionally reliant on a complex network of intermediaries and often characterized by batch-based settlement, has long been plagued by inefficiencies, including slow processing times, high transaction fees, and a notable lack of transparency. A new paradigm is emerging with the advent of blockchain technology, offering shared, programmable settlement layers that operate continuously, 24/7, and can finalize transactions in mere seconds. This article delves into how blockchain technology is fundamentally improving cross-border payments, highlighting the specific challenges it addresses and outlining how Chainlink’s industry-standard solutions for data, interoperability, compliance, and privacy are powering reliable, transparent, and secure cross-border and cross-chain payment infrastructures.

The Persistent Challenges in Traditional Cross-Border Payments

For decades, the global financial system has relied predominantly on the correspondent banking model, a network where banks hold accounts with each other to facilitate international transactions. This system, largely underpinned by messaging networks like SWIFT (Society for Worldwide Interbank Financial Telecommunication), while robust, was not designed for the instantaneous, high-volume demands of the modern digital economy. Its inherent architecture introduces several significant friction points.

- High Costs: Traditional cross-border payments typically involve multiple intermediary banks, each levying their own fees. These charges can include sender fees, recipient fees, and often hidden foreign exchange (FX) markups. The World Bank reported that the global average cost of sending remittances was 6.2% in Q4 2023, far above the UN Sustainable Development Goal target of 3%. For businesses, these costs accumulate rapidly, impacting profitability and increasing the expense of international trade.

- Slow Processing and Settlement Times: Transactions frequently pass through several banks in different time zones, each with its own operational hours and batch processing schedules. This multi-hop process can extend settlement times from days to even weeks, introducing significant delays for businesses managing supply chains and individuals needing urgent funds. This latency is particularly problematic in a globalized economy that demands real-time financial flows.

- Lack of Transparency: Senders and recipients often lack real-time visibility into the status of a payment or the exact breakdown of fees applied by each intermediary. This opacity leads to frustration, increased customer service inquiries, and difficulties in reconciliation for corporate treasuries. The exact arrival amount can also be uncertain due to fluctuating FX rates and unpredictable intermediary charges.

- Operational Risk and Manual Reconciliation: The involvement of numerous parties and disparate systems necessitates extensive manual reconciliation processes, which are prone to errors and create operational overhead. Furthermore, the time lag in settlement exposes parties to counterparty risk, as funds are in transit for extended periods.

- Regulatory Complexity: Navigating diverse regulatory frameworks across multiple jurisdictions, including Anti-Money Laundering (AML) and Know Your Customer (KYC) requirements, adds layers of complexity and cost. Banks must perform due diligence on all parties involved in a transaction, a process that can be cumbersome and time-consuming.

Blockchain Technology: A New Paradigm for Global Payments

At its core, a blockchain is a highly secure and reliable distributed ledger network that enables participants to record transaction activity, store data, and exchange value without the need for a central authority. For payments, this level of reliability, immutability, and decentralization enables near-instant finality, always-on operations, and automated value transfer workflows, fundamentally reimagining the architecture of cross-border transactions.

- Enhanced Speed and Near-Instant Finality: Unlike traditional systems bound by business hours and cutoff times, blockchain networks operate 24/7/365. Transactions can achieve finality, meaning they are irreversible and settled, often within seconds or minutes, regardless of geographic location or time zone. This dramatic reduction in settlement time mitigates counterparty and settlement risk, allowing for immediate value transfer and improved liquidity management.

- Significant Cost Reduction: By replacing layers of intermediaries with shared, decentralized infrastructure, blockchains streamline the payment process. On-chain transfers eliminate the need for multiple clearing entities, correspondent banks, and the associated SWIFT messaging fees. This reduction in operational complexity and reliance on third parties helps lower the all-in cost of cross-border payments for both businesses and consumers, moving closer to the goal of near-free global transfers.

- Unprecedented Transparency and Auditability: Payments on blockchain networks are recorded on an immutable ledger, verifiable in real time by all authorized parties. This provides granular visibility into transaction status, associated fees, and the complete transaction history. Built-in cryptographic guarantees ensure data integrity, drastically reducing the risk of fraud or tampering. Additionally, on-chain records simplify audits and regulatory reporting, offering a clear and accessible trail of transaction data.

- Robust Security and Reduced Risk: The cryptographic principles underpinning blockchain technology, coupled with its distributed nature, make it highly resistant to cyberattacks and unauthorized alterations. Each transaction is encrypted and linked to the previous one, forming an unbreakable chain. This inherent security architecture reduces the risk of fraud, errors, and malicious activity, enhancing trust in the payment system.

- Programmability and Automation: Smart contracts, self-executing agreements stored on the blockchain, introduce a new level of programmability to payments. They can automate value transfer workflows, enforce complex business logic (e.g., conditional payments, escrow services), and integrate seamlessly with other systems. This automation reduces manual intervention, further cutting costs and increasing efficiency.

Key Use Cases of Blockchain in Cross-Border Payments

The advantages offered by blockchain technology are particularly impactful across several key sectors of cross-border payments:

- Remittances: For migrant workers sending money home, often to developing countries, blockchain offers a lifeline. By drastically reducing fees and speeding up transfers, it ensures more money reaches families faster. Platforms leveraging blockchain and stablecoins can facilitate remittances at a fraction of the cost and time compared to traditional money transfer operators. The World Bank estimates global remittances reached $860 billion in 2023, underscoring the massive potential impact of efficiency gains in this area.

- Interbank Settlements and Wholesale CBDCs: Central banks and commercial banks are actively exploring blockchain for interbank settlements. Wholesale Central Bank Digital Currencies (CBDCs) and tokenized deposits on distributed ledgers could enable real-time gross settlement (RTGS) between financial institutions across borders, eliminating settlement risk and improving liquidity management. Projects like the Bank for International Settlements’ (BIS) Project Mariana demonstrate the potential for multi-CBDC platforms to facilitate seamless FX transactions and cross-border payments.

- Corporate Treasury and Trade Finance: Multinational corporations can leverage blockchain to manage their international liquidity more efficiently, execute payments faster, and reduce reconciliation efforts. In trade finance, blockchain can digitize and automate aspects of supply chain financing, letters of credit, and guarantees, reducing paperwork, fraud, and the time required to settle international trade transactions.

- Retail and E-commerce: For consumers making international purchases, blockchain-based payment solutions, often utilizing stablecoins, can offer faster, cheaper, and more transparent alternatives to credit cards or traditional bank transfers. This can enhance the global reach of e-commerce businesses and improve the customer experience for international shoppers.

Chainlink’s Critical Role in Orchestrating Advanced Blockchain Payments

While blockchain networks provide the foundational ledger, they inherently operate in isolation from the vast amounts of real-world data and existing enterprise systems necessary for complex financial operations. This is where oracle networks become indispensable. Chainlink, as the industry-standard oracle platform, bridges this critical gap, providing the essential data, interoperability, compliance, and privacy standards needed to power advanced blockchain use cases like cross-border payments. Without Chainlink, the promise of blockchain for global finance would remain largely unrealized, as tokenized assets and on-chain transactions would lack the external context and connectivity required for practical application.

- Accurate Price Data with Chainlink Data Feeds: Cross-border payments frequently involve foreign exchange conversions. Chainlink Data Feeds provide tamper-resistant, highly accurate, and real-time market data for FX conversion, rate locking, and settlement logic. By aggregating data from numerous high-quality off-chain sources and delivering it on-chain via a decentralized network of oracle nodes, Chainlink ensures that payments are executed at precise, real-time prices, mitigating slippage and ensuring fair value for all parties.

- Ensuring Asset Integrity with Chainlink Proof of Reserve (PoR): The integrity of stablecoins and other tokenized assets used in cross-border payments is paramount. Chainlink Proof of Reserve provides smart contracts with the verifiable data needed to calculate the true collateralization of any on-chain asset backed by off-chain or cross-chain reserves. This ensures that assets used for payments, especially stablecoins, are transparently and reliably backed by verifiable reserves, fostering trust and stability in the digital asset ecosystem.

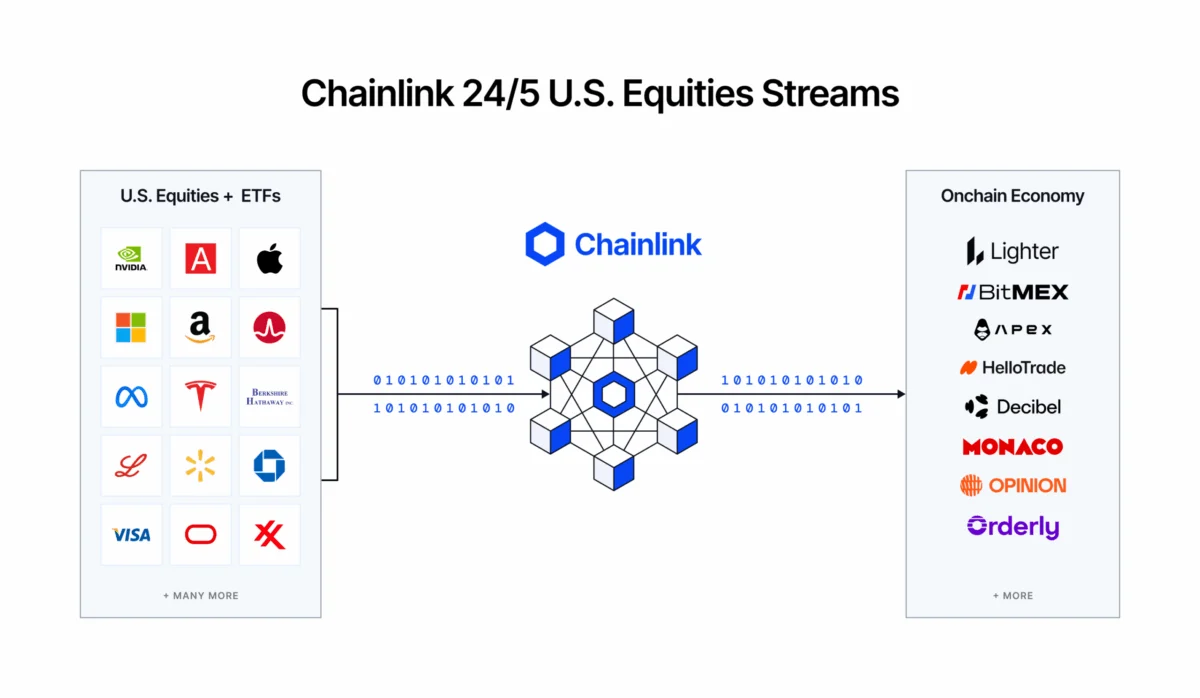

- Seamless Interoperability with Chainlink CCIP (Cross-Chain Interoperability Protocol): The blockchain landscape is fragmented, with many distinct networks. Cross-border payments often require interaction between different public and private blockchains. Chainlink CCIP is a robust, secure, and future-proof protocol that enables arbitrary cross-chain data and value transfers across any public or private blockchains. Financial applications can use CCIP to trigger token transfers or status updates to execute cross-border and cross-chain payments with the highest level of cross-chain security, effectively acting as the "internet of blockchains" for financial institutions.

- Unlocking Real-World Assets (RWAs) with Chainlink SmartData: The tokenization of real-world assets (RWAs) is a major trend in finance, and these tokenized assets are increasingly used in payments. Chainlink SmartData is a suite of on-chain data offerings designed to unlock the utility, accessibility, and reliability of tokenized RWAs. In the context of cross-border payments, SmartData enables applications to enforce settlement limits, validate collateralization, and provide accurate asset valuations across diverse jurisdictions, bridging the gap between traditional assets and on-chain finance.

- Automated Compliance with Chainlink ACE (Automated Compliance Engine): Regulatory compliance is a non-negotiable aspect of institutional finance. Chainlink’s Automated Compliance Engine (ACE) empowers users to build, manage, and execute complex financial transactions across multiple jurisdictions, counterparties, digital assets, and environments, all in a compliance-focused and privacy-preserving manner. For cross-border payments, Chainlink ACE can enforce jurisdiction-specific KYC/AML, sanctions screening, and other compliance policies directly on-chain by evaluating both identity and compliance data before a payment is executed, dramatically streamlining regulatory adherence.

- Holistic Transaction Orchestration with Chainlink Runtime Environment (CRE): To truly facilitate institutional-grade smart contracts for on-chain finance, an all-in-one orchestration layer is crucial. The Chainlink Runtime Environment (CRE) coordinates the full transaction lifecycle, including complex compliance checks, real-time FX data retrieval, settlement execution, and off-chain system reporting. In a single execution environment, CRE connects diverse chains, essential data, and enterprise systems while automating compliance and privacy, delivering fast, verifiable, and enterprise-grade cross-chain operations that are critical for institutional adoption. For example, a payment application could collect funds on one blockchain, use CCIP to send a token transfer to another chain where the payment settles in a stablecoin, with Chainlink Data Feeds providing FX rates and Proof of Reserve verifying collateral backing—all orchestrated and made compliant by CRE.

- Enhancing Privacy for Cross-Border Transactions with Confidential Compute: While transparency is a blockchain strength, institutions often require privacy for sensitive transaction details, proprietary logic, or competitive data. Chainlink enables privacy-preserving blockchain transactions through Confidential Compute, which allows sensitive logic and data to be processed off-chain in secure, verifiable environments (like Trusted Execution Environments) while only verifiable outcomes are recorded on-chain. As part of Chainlink’s broader privacy standard, this architecture facilitates private cross-border payments, selective disclosure for compliance purposes, and confidential cross-chain execution, enabling institutions to leverage public blockchains for cross-border settlement without exposing proprietary or sensitive information to the public ledger.

Regulatory Landscape and Adoption Challenges

Despite the clear benefits, the widespread adoption of blockchain in cross-border payments faces several hurdles. Regulatory uncertainty remains a significant challenge, as governments worldwide grapple with how to classify and regulate digital assets and blockchain networks. Different jurisdictions have varying licensing requirements, AML/CFT standards, and data privacy laws, creating a complex patchwork that institutions must navigate. Interoperability standards among different blockchain protocols and traditional financial systems also need further development to ensure seamless integration. Scalability of certain blockchain networks to handle global payment volumes is another concern, though ongoing technological advancements are addressing this. Finally, overcoming the inertia of deeply entrenched legacy infrastructure and cultural resistance within large financial institutions requires significant investment and a willingness to innovate.

The Future Outlook for Blockchain in Cross-Border Payments

Today’s global payment systems are slow, expensive, and opaque, often involving multiple intermediaries, high fees, and extended settlement times. Leveraging blockchains fundamentally transforms these transactions, making them faster, more transparent, and significantly more secure. As institutions, corporations, and governments increasingly seek to advance efficient, compliant, and inclusive financial infrastructure, blockchain-based cross-border payments are not merely an incremental improvement but a key driver in the next evolution of global finance.

The convergence of tokenized assets, decentralized oracle networks, and robust interoperability solutions like Chainlink’s suite of services is creating a new foundation for global financial infrastructure. This future promises a world where value moves as freely and efficiently as information, fostering greater financial inclusion, reducing costs for businesses and consumers alike, and underpinning a more resilient and integrated global economy. The journey towards this future is ongoing, marked by pilot programs, regulatory discussions, and continuous technological innovation, but the trajectory towards blockchain-powered cross-border payments is clear and irreversible.